$5.05 Trillion Valuation: India's Equity Market Risks Collapse Amid Sanctions Dependency

TL;DR

- $5.05 Trillion Valuation: India's Equity Market Risks Collapse Amid Global Policy Shifts. Is India's $5.05 trillion market cap a sign of genuine growth or a fragile mirage dependent on global oil luck?

- 3% Green Energy Slide: India's ESG Bubble Faces Profitability Reality Check. Is India's green energy rally a sustainable shift or just an overvalued ESG bubble about to burst?

- $310.5M SSMR IPO: Niche TSXV Debut Fails to Move Needle Amid S&P 500 Surge. Is SSMR's $310 million TSXV debut a genuine mining catalyst or merely a liquidity mirage?

📉 The Fragile High: India's Equity Mirage

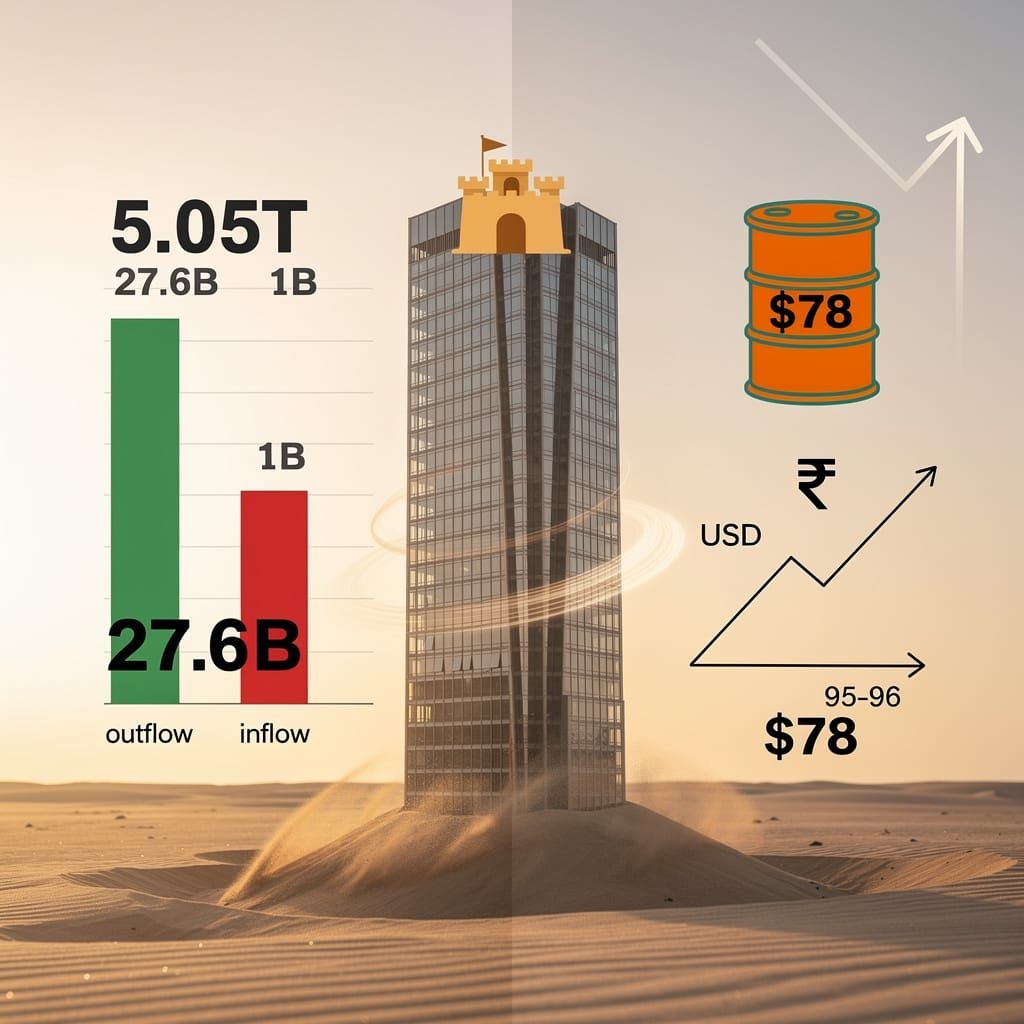

$5.05 Trillion valuation—a staggering mirage. 📉 That's like building a skyscraper on sand. This 'recovery' is just a byproduct of a temporary US sanctions waiver, not actual growth. FIIs dumped $27.6B before a tiny $1B trickled back. Sustainable? Hardly. Indian investors—is this growth or just a lucky break?

The Indian equity market is currently riding a wave of optimism that relies more on external luck than internal strength. While headlines suggest a recovery, the reality is a systemic dependency on global volatility. By June 2026, the narrative of a $5.05 trillion valuation serves as a convenient veil for deeper structural fractures.

Why the Optimism?

The current surge is not a product of productivity, but a causal chain of geopolitical concessions. The resolution of tensions in the Strait of Hormuz—triggered by a US-six month US sanctions waiver and a preliminary agreement on June 23—depressed Brent crude to ~$77.64/bbl. This easing of the energy chokehold reduced fiscal stress for an import-dependent economy, creating a superficial window for growth.

However, this "recovery" is a reaction to the absence of a crisis. The market's fragility is demonstrated by the ease with which capital vanishes when the wind shifts.

Market Drivers:

- Oil Prices: Brent crude's slide toward $78.58/bbl following the US-Iran interim agreement reduces the import burden and trims inflation headwinds.

- Monetary Policy: Stability is an illusion; while the RBI maintains a policy rate of 5.25%, global markets remain twitchy as the Fed weighs persistent inflation and a potential mid-to-late 2026 tightening cycle.

- Currency: The Rupee's stability is purely coincidental. It recently slumped to 95–96 per USD, driven by the same US-Iran volatility that now temporarily fuels the rally.

Current State vs. Reality:

- Valuations: A $5.05 trillion market cap indicates a shift toward commodity-driven narratives, not sustainable growth.

- Liquidity: The touted $1 billion FII inflow in June is a drop in the bucket compared to the $27.6 billion foreign investors dumped from Indian shares in previous weeks.

- Performance: While June saw a momentary bump (Sensex +3.8%, Nifty +2.8%), these gains follow a brutal 9.3% decline in recent weeks as AI hype shifted focus toward peers like the KOSPI.

The Outlook:

- Q3 2026: Continued volatility as the market digests revised downward earnings forecasts from firms like Nomura.

- Mid-2026: High risk of capital flight if the US-Iran interim agreement fails or if Fed rate hikes accelerate.

📉 The Green Mirage: India's Divergent Energy Rally

3% plunges in green heavyweights reveal a grim reality: the ESG dream is fading 📉. This is a massive disconnect between hype and actual profit. Institutional investors are finally dumping the "green premium" for real value. Is your portfolio holding a mirage or a business? India investors — are you still buying promises?

On July 3, 2026, the S&P BSE SENSEX and NIFTY 50 climbed by 0.34% and 0.38% respectively, providing a thin veneer of stability. Beneath these headline figures, the green energy sector exhibited a fractured performance. While Websol Energy edged up 0.99%, heavyweights like JSW Energy (-2.71%) and Olectra Greentech (-3.06%) closed sharply down. This divergence indicates that institutional investors are no longer buying the "ESG dream" on faith; they are rotating capital based on actual profitability rather than thematic hype.

Is the Valuation Bubble Bursting?

Market breadth fails to support current green energy valuations. Despite the launch of the North Star platform by BII and CIP, and a clean-energy partnership with the Netherlands in May 2026, the internal churn reveals a strategic exit. The May-June period demonstrates a causal chain where US-Iran geopolitical tensions and rupee depreciation triggered a sector rotation toward value plays. This volatility met inflated P/E ratios, resulting in a cautious repositioning where institutions treat ESG stocks as liquid assets to be trimmed.

Sectoral Friction

- Valuations: Disconnect between high multiples → increased vulnerability to profit-booking.

- Institutional Flow: Shift from thematic ESG → value plays and revenue-based metrics.

- Market Breadth: Narrow gains → reliance on outliers to sustain index levels.

The Path Toward Correction

The current trajectory demonstrates that the "green premium" is eroding. Investors now demand tangible margins over promises of carbon neutrality. While the sector sees opportunistic wins—such as the NTPC Green Energy and Ctrls Data Centers joint venture—systemic failures persist. The abrupt termination of PPL's commissioning on April 29, 2026, due to non-compliant battery storage strategies, underscores the gap between announced capacity and operational reality. Government incentives provide a floor, but they cannot sustain speculative multiples against a backdrop of widening corporate bond spreads.

- Q3 2026: Increased volatility as quarterly results test the validity of green energy premiums.

- Q4 2026: Potential 5–10% correction in overvalued ESG stocks if profit-booking accelerates.

- 2027: Market equilibrium reached only after valuations align with actual dividend yields and free cash flow.

🙄 The $310 Million Mirage: SSMR's TSXV Debut

$310.5M total—a rounding error compared to the S&P 500's $8.74T gain 🙄. SSMR's TSXV debut claims "engagement," but institutional capital is chasing AI, not niche mining. With Fed rate hikes looming, is this a strategic move or just a desperate liquidity grab? Local investors—buying the hype?

On June 5, 2026, SSMR attempted to capture market attention by offering 23 million shares at $13.50 each on the TSXV. While the company frames this move as a strategic expansion, the math reveals a modest play in a niche sector, resulting in a total offering value of $310.5 million.

Does this signal a mining renaissance?

The company claims the IPO enabled "enhanced shareholder engagement," a corporate euphemism for the fact that a few local investors are now curious. However, this curiosity is a rounding error compared to the broader sector. While SSMR was filing paperwork, the real action occurred in the energy and commodity space; on June 1, analysts pivoted toward undervalued commodity stocks as the Strait of Hormuz closure pushed WTI and Brent crude above $90 per barrel. SSMR's launch is a localized event, not a catalyst, demonstrating a wide gap between internal optimism and actual market weight.

- June 5, 2026: SSMR initiates IPO of 23M shares at $13.50.

- June 8, 2026: Alliance Resource Partners executes a $206.2M mineral interest purchase, dwarfing the scale of individual IPO activity.

- June 16, 2026: Integrated Minerals Management Inc. launches a C$300,000 exploration program, illustrating the modest, fragmented nature of current junior mining spends.

- Q3 2026 projection: Stagnation likely as capital flows into AI infrastructure, exemplified by IREN’s $1.6B deal with Dell.

Market Influence: Low volume → negligible impact during the May 29 sell-off where US markets dropped 9.3% from all-time highs. Investor Interest: Local curiosity → failure to attract institutional capital currently chasing AI-driven equities and semiconductor giants. Capital Scale: $310.5M total → insufficient to shift regional pricing compared to the $8.74 trillion net gain in the S&P 500 since April.

Despite the registration formalities, the causal chain from this IPO to sector growth is nonexistent. The event indicates a desire for liquidity by SSMR rather than a shift in mining viability. While the company celebrates "engagement," the broader equity market remains indifferent to a mid-sized listing on a secondary exchange, especially as the Federal Reserve signals an 85% probability of rate hikes, further pressuring high-risk, low-liquidity assets.

Comments ()