$200B GDP Target: Canada's AI Strategy vs. US Tech Giants

TL;DR

- $200B GDP Target: Canada Launches AI Strategy Amid US Capital War. Can Canada's $1.2B AI fund actually stop the brain drain to Silicon Valley?

- $1.8B Valuation: IQM Quantum Computing Hits NASDAQ to Challenge US Dominance. Is listing on the NASDAQ the only way for European quantum startups to survive US subsidies?

- $1.4 Trillion at Stake: UK CMA Challenges App Store Monopolies to Open NFC Payments. Will the UK's move to bypass App Store fees boost FinTech innovation or compromise mobile security?

🇨🇦 Maple Leaf Intelligence: Canada’s $2B AI Gamble

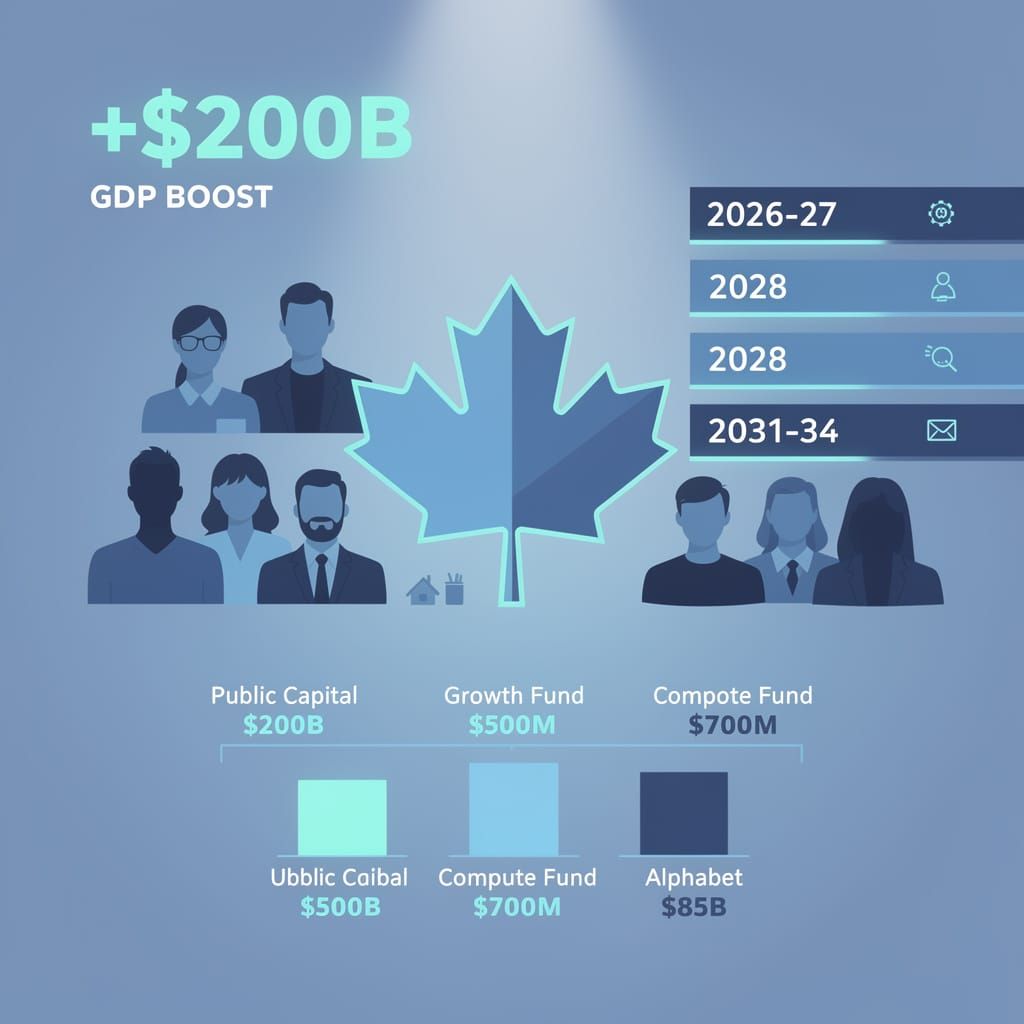

$200B GDP boost: Canada's AI gamble is massive, roughly the size of its entire current tech output 🇨🇦. Ottawa's dumping $1.2B into growth and compute to stop the brain drain. But can state grants beat an $85B Alphabet war chest? Local founders — is this real support or just 'zombie' funding?

Canada is done being the world's AI nursery—the place where geniuses are trained only to be poached by Silicon Valley. On June 4, 2026, Prime Minister Mark Carney unveiled the "AI for All" strategy, a pivot from passive support to aggressive market engineering. The goal? A $200B GDP boost and 250,000 new jobs by 2031.

Can State Capital Stop the Brain Drain?

Canadian startups usually nail the research but choke on commercialization. Ottawa is attempting to break this cycle with a $500M Tech Growth Fund for local startups and a $700M Compute Access Fund.

But the strategy is fighting a brutal global tide. While Canada pushes for "AI sovereignty" via the ~$20B Cohere-Aleph Alpha merger, the US titans are simply outspending the room. Alphabet just announced an $85B equity raise to fuel AI expansion, and OpenAI has officially filed for its IPO, signaling a capital war that makes national grants look like pocket change.

The Causal Chain: Public Capital → Reduced Early-Stage Risk → Private VC Inflows (e.g., Beacon's $225M raise) → Domestic Scaling → Export Growth.

The Roadmap:

- 2026–2027: Deployment of $500M Growth Fund to fuel mid-stage Series B/C rounds.

- 2028: Integration of workforce pipelines to mitigate displacement (as AI-driven layoffs hit Meta, Nvidia, and Oracle for 97,006 jobs).

- 2031–2034: Target of 60% AI adoption across sectors and a $200B GDP increase.

The Reality Check

It's not all maple syrup and unicorns. Canada is trying to build an industry while the tools of that industry are eating the workforce. The "AI for All" job targets clash with a global trend of aggressive automation; the very efficiency Canada is funding is what led Nvidia to cite AI as the primary driver for its own mass layoffs.

Furthermore, geopolitical instability is complicating the math. With Iran threatening to close the Strait of Hormuz and oil-driven inflation hitting 4.2%, the cost of powering the massive data centers required for this gamble is skyrocketing.

Strengths: Strong academic base; new $6.6B Defence Industrial Strategy; sports-tech wins (World Cup 2026). Weaknesses: High compute costs; history of "exit-to-USA"; energy security risks. Opportunity: Leading "Ethical AI" via the Safe Social Media Act. Risk: Creating "zombie startups" dependent on grants rather than market viability.

By coupling sovereign investment with an export-first mindset, Canada is betting it can transform from a talent incubator into a powerhouse. Whether it can outrun the bureaucracy—and the job-killing efficiency of the AI it's funding—remains to be seen.

🚀 The Quantum Heist: IQM Hits NASDAQ

$1.8 Billion valuation! 🚀 IQM just raided the NASDAQ to fight the US quantum wall, securing a war chest equivalent to 12% of IBM's recent foundry push. 💻 Finland's powerhouse is going public to avoid becoming a mere 'cloud client.' Risking SEC oversight for survival? Nordic founders — is the US exchange the only way to scale now?

European quantum computing just stopped playing catch-up. IQM Quantum Computing officially landed on the NASDAQ under the ticker IQMX, executing a calculated raid on US capital to fuel a Finnish powerhouse. This isn't just a vanity play; it is a strategic maneuver to survive a global arms race where the US is currently spending billions to build a "quantum wall."

How did the plumbing work?

IQM didn't just walk onto the exchange; they merged with Real Asset Acquisition Corp (RASAC) to transform from a private gem into a public American asset. The move was backed by a pre-money valuation of ~$1.8 billion and a €146 million PIPE financing boost from ILMARINEN. With 23 quantum computers already sold and €31 million in audited revenue, IQM has the receipts to justify the hype.

- June 5, 2026: Registration statement becomes effective for the business combination.

- June 23, 2026: Hardware deployment milestone achieved at Oak Ridge National Laboratory.

- July 1, 2026: Deal closes; IQM completes the $233.5 million ADS-listed buyout with a matching $233.5 million PIPE to scale operations.

Why the sudden rush?

Because the US is playing aggressive. The Department of Commerce recently pumped $2 billion in CHIPS Act incentives into quantum R&D, including a massive $1 billion for IBM to build the Anderon quantum foundry—the first 300mm quantum wafer facility in the States. Between IBM’s $10 billion R&D roadmap and Quantinuum’s $12.7 billion valuation IPO, Europe is fighting for "digital sovereignty" or risk becoming a mere client of US clouds.

By listing on the NASDAQ while keeping its hub in Finland, IQM creates a causal chain: government-backed research triggers hardware sales, which enable high-valuation listings, which then fund non-cloud-dependent hardware.

Strategic Gains:

- Capital: $233.5 million injection for aggressive R&D scaling.

- Liquidity: Dual-listing plans (Nasdaq and Helsinki SE) enhance growth capacity.

- Validation: Public revenue figures provide a competitive edge over lab-bound startups.

Structural Risks:

- Regulation: ADS security structures invite heavy SEC oversight.

- Competition: US incumbents (IBM, Quantinuum) enjoy massive domestic subsidies.

- Security: Rapid scaling increases the urgent need for quantum-resistant encryption.

What happens next?

Quantum is now a financial instrument. With Europe deploying 35 new NVIDIA AI supercomputers (800 exaFLOPS) to integrate classical-quantum workflows via CUDA-Q, the industrial ecosystem is finally catching up to the financial ambition.

- Q3 2026: Rollout of Q-beta systems across European research hubs.

- Q4 2026: Launch of nuclear-fusion prototypes, merging CleanTech and Quantum funding.

- 2027: Projected wave of Nordic quantum IPOs following the RASAC blueprint.

💸 The Great App Store Jailbreak

30% fees? That's the dream. The UK is targeting a 30% commission tax on a $1.4T revenue machine 💸. It's like giving developers their own keys to the kingdom. But is opening the NFC chip a security nightmare in the AI era? FinTechs win, but users might risk it all. UK devs, are you ready to ditch the walled garden?

Apple and Google have long held the keys to the mobile kingdom, skimming a chunky 30% cut from digital transactions. But on June 30, 2026, the UK Competition and Markets Authority (CMA) decided to kick in the door. The regulator proposed a plan to lift restrictions on "app steering," enabling developers to direct users toward non-platform payment methods—including NFC-enabled cards—effectively bypassing standard commission fees.

Why now?

The move targets a market where reliance on dual-platform dominance is roughly 90%. While the "walled garden" approach stifled competition, the stakes have skyrocketed. In 2025, Apple's App Store generated a record $1.4 trillion in developer revenue, a 3x increase since 2019. By breaking the monopoly on payment routing, the CMA aims to inject competition into a global economy where digital goods are now a significant share of global GDP. For UK FinTechs, this is liberation; for the tech giants, it is a direct hit to high-margin revenue.

The Security Trade-off

Apple isn't taking the news lightly, warning that opening the NFC chip creates a security vacuum. This isn't just corporate whining; the risk is tangible. New AI-driven phishing kits and the rise of autonomous coding agents for bug-hunting demonstrate how quickly vulnerabilities are exploited. Furthermore, as Apple pushes visionOS 27 and iOS 27 with on-device AI, the attack surface is expanding. Opening payment gateways during a period of heightened cybersecurity risk—including recent AI-driven cyber-campaigns—could leave users exposed.

Risk Analysis

- Security: Loss of encrypted silos → heightened fraud risk via unvetted steering links.

- Financial: Diversified payment options → erosion of the 30% commission on $1.4T+ revenue streams.

- Innovation: NFC openness → faster development of independent FinTech solutions.

The Valuation Crunch

While developers cheer, investors are sweating. Andrew Cheng, formerly of Campbell Global Investors, indicates that antitrust-driven volatility threatens valuation targets, specifically those eyeing the €2bn mark. When monetization shifts from predictable platform fees to a fragmented open market, the revenue streams VCs love tend to wobble.

What follows?

- Q3 2026: Initial rollout of steering mechanisms; anticipated 5-10% shift in payment volume for top-tier apps.

- Q4 2026: Potential platform fee restructuring to prevent mass exodus of high-value developers.

- 2027: Full third-party NFC integration, potentially reducing consumer transaction costs by 15-30% across the UK.

Comments ()