484K sidelined for 1,617 jobs — Wales startup alarm flashes amid £2.6B SME gap and innovation collapse

TL;DR

- Wales Startup Alarm Snoozes: 484K Adults Idle, Innovation Crashes to 27.7%, £2.6B SME Gap Squeezes Founders. Is your Welsh startup caught in the £2.6B SME funding squeeze?

- Three Deployed Music SaaS Apps, Zero Marketing: UK Solo Developer Builds Full Concert Stack But Hits Invisible Growth—Sweat Equity Test Against Capital-Flooded Giants. Can a solo UK developer scale three music SaaS apps on sweat equity alone before July ends?

- $50,000 India Tray Startup: Founder Bets Home Décor Can Outpace AI Capital Wave. Is there still room for a $50K tray startup when AI funding hits nine figures?

🔥 Wales Hit the Snooze Button on Its Startup Alarm

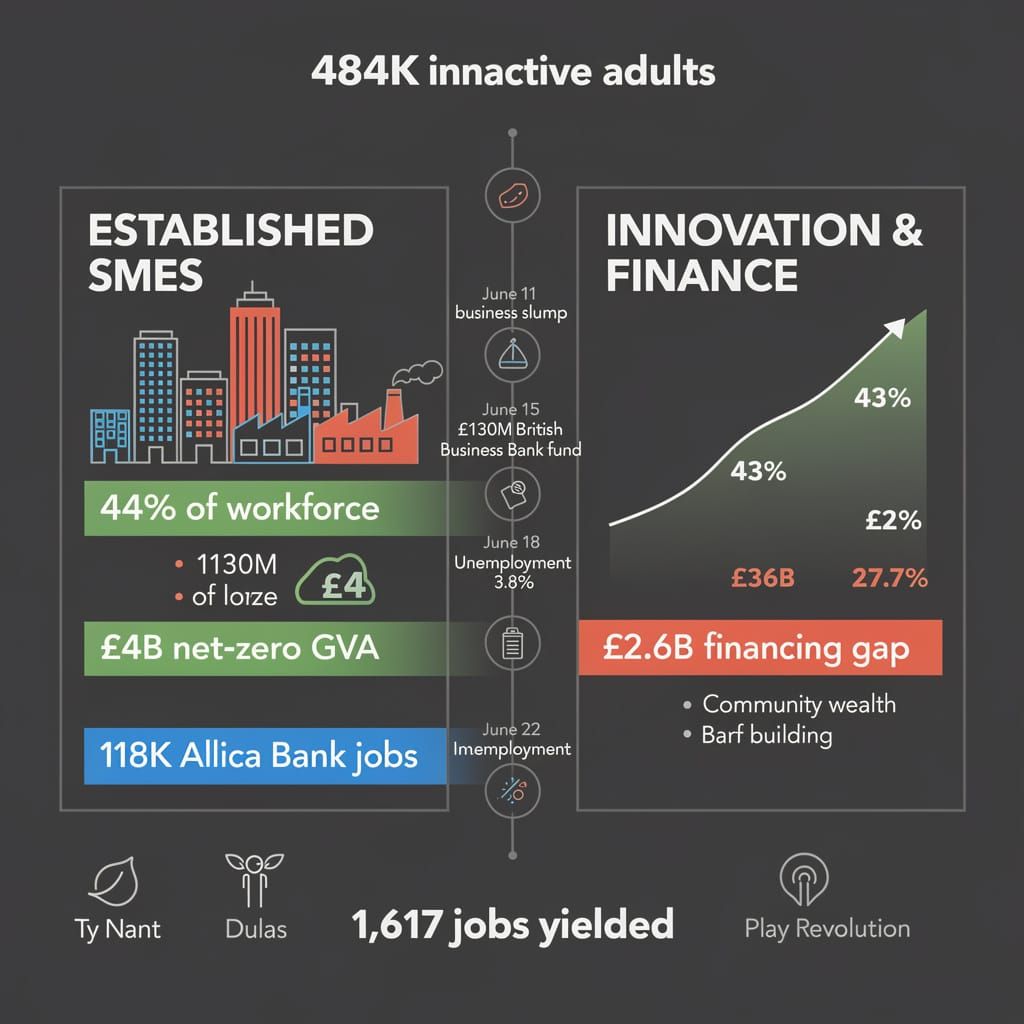

484K Welsh adults ride the bench while new projects yielded a measly 1,617 jobs. 🔥 That's ~300 sidelined workers per role. Innovation nosedived from 43% to 27.7%, and a £2.6B SME gap has founders on hold. Wales keeps old paychecks alive but can't birth new startups. — Is your venture stuck in that funding traffic jam?

Wales is running a strange split-screen economy. On June 11, business activity slumped while inflation stayed stubborn, and by June 18 unemployment had crept up to 3.8%—the opposite direction to the UK’s 4.9% fall. That left 484,000 working-age adults economically inactive. Yet on June 19, Oxford Economics showed established SMEs still employ 44% of the private-sector workforce, keeping the labor market from sliding further. Toss in the June 5 Sunday Times 100 ranking of fast-growing Welsh firms like Ty Nant and de Novo Solutions, plus Dulas bagging the 2024 SME Exporter of the Year award for solar vaccine refrigerators, and the picture gets weird: Wales is preserving yesterday’s jobs while struggling to birth tomorrow’s companies.

Why Is the Next Generation Stuck in Neutral?

Two barriers keep the alarm ringing. First, capital is patchy. Oxford Economics puts the SME financing gap at £2.6 billion. Allica Bank has already backed 118,000 jobs, but that stream has not reached every corner. Second, innovation is corroding: Wales dropped from 43% innovation-active firms in 2018–20 to just 27.7% in 2022–24, the widest lag of any UK region. With UK GDP crawling at roughly 1% and productivity limping along at 0.4% year-on-year, the founder pipeline is not just narrow—it is leaking.

New money is arriving, but unevenly. On June 15, Foresight Group reported strong deal flow from the British Business Bank’s £130 million Investment Fund for Wales, backing firms like Play Revolution and Advantiv. Inward investment projects also climbed to 75 in June 2026—the only UK increase—but they promise only 1,617 jobs, down from 2,470 the year before. Capital is flowing, yet job yields are shrinking.

Policy is stirring, though the wallet is tight. Adam Price wants to halve Wales’ productivity gap with the UK inside ten years, and the new Welsh Innovation and Development Agency is meant to deliver the wiring. Meanwhile, Finance Minister Elin Jones has already flagged "extremely difficult decisions" around roughly £1 billion in pre-election pledges, suggesting the fiscal cupboard is closer to bare than advertised. Net zero industries already pump £4 billion GVA and support 41,000 roles, and on June 22 Cwmpas CEO Bethan Webber pushed community wealth building through cooperatives like Dulas as a way to keep talent and profits local. These bright spots indicate Wales knows where the future lives; the trick is paying the fare to get there.

- 2026: Tight credit, hesitant hiring, and a congested fiscal runway keep short-term stimulus parked. Unemployment at 3.8% and 484,000 inactive adults signal labor-market friction.

- Mid-term: Adam Price’s ten-year productivity target and the £130 million Investment Fund aim to unlock scaling. If the Welsh Innovation and Development Agency converts rising deal flow into real jobs—and community wealth models keep ownership Welsh—business formation might claw back toward the UK average.

- Long-term: Digital transition and clean-tech scale remain the gatekeepers. Without them, manufacturing exposure climbs and innovation stays stuck in the slow lane despite the CSconnected and net-zero momentum.

🎤 The Quietest Launch Party in Music Tech

3 music SaaS apps, $0 marketing: a UK solo dev built an entire concert stack and hit total silence 🎤 While SpaceX courts a $75B IPO and Google drops fresh apps,Playlistr is stuck fighting for forum clicks. One builder, three products, zero budget—can sweat equity cut through the noise before July?

On June 26, 2026, a solo developer in the United Kingdom flipped the switch on not one, not two, but three interlinked music SaaS products—Playlistr LIVE, Playlistr Connect, and Playlistr FanCam—and then discovered that shipping code does not automatically ship attention.

The trio covers the full concert stack. LIVE handles real-time audience chat, Connect manages artist ticketing, and FanCam triggers auto-photo capture at shows. Each module runs on its own URL, fully deployed and autonomous. The marketing budget sits at exactly zero dollars. The growth strategy, so far, consists of posts to niche tech forums.

That is exactly the bottleneck. Product readiness never pulls traction on its own, and without sales channels the apps stay invisible to venues and musicians who could actually use them.

Visibility: Confined to tech forums while live-event demand is consolidating elsewhere—on June 3 YouTube secured Academy Awards broadcast rights and partnership deals with the NFL and ESPN, signaling that streaming and live content are commanding massive platform investment. Growth: Zero marketing spend plus zero sales functions equals zero discoverability, even though a precedent exists: in March 2014 the startup Play My Inbox launched to streamline music delivery via email threads, proving that a lean music tool can find users when it targets a clear workflow gap. Capital: Cash reserves are absent, so the founder barters profit participation—sweat equity—for introductions and grassroots venue deals.

Can Sweat Equity Turn Up the Volume?

The entire future rides on whether industry contacts join fast enough to close the gap. The developer needs partners who can translate forum silence into stage-side pilots.

There is precedent, but there is also unprecedented noise. Play My Inbox showed a solo builder could carve out a music-tech niche in 2014; yet the current feed is dominated by capital-dense launches. SpaceX announced a $75 billion IPO on June 4, Google dropped its Dreambeans storytelling app the same day, and on June 17 the anonymous infrastructure startup Z.AI generated instant hype simply by deploying its first public cloud server. When giants flood the zone, a forum post competes against algorithmic engagement machines.

- End of July 2026: If brand partners onboard within weeks, monthly active users could exceed 500. Without that intervention, the suite stays locked in obscurity.

Three deployed apps, one solo builder, and a classic startup truth: deployment day is not the finish line. It is the moment you notice nobody can find the door—especially while the rest of the concert world is already flooding through another one.

🛋️💸 The $50,000 Tray: Why This Founder Thinks Your Coffee Table is Underserved

$50K tray startup vs $234M AI rounds. An India founder just bet your coffee table is underserved—launching into Prime Day chaos, no less 🛋️💸 While capital rushes to compute giants, boutique physical goods compete for attention. Can a sharper tray still win in a market chasing chips? Who's backing design over data centers?

On June 26, 2026, an India-based founder unloaded a luxury serving tray and home décor line into the retail wild. The pitch? Your living room, hotel lobby, and wedding registry deserve better hardware. The ask? A cool $50,000 to cover inventory, branding, and enough digital marketing to cut through the noise—or a co-founder with serious sales and e-commerce chops who can move acrylic and custom décor into hospitality and gifting channels.

Before the debut, the founder had already hammered out supplier relationships and mapped a corridor between gifting culture and wholesale hospitality. The line targets buyers hunting for bedroom accents, event décor, and premium serviceware, sliding into a gap where mass-market clutter meets boutique pricing. Existing manufacturing networks keep upfront costs in check, but scaling demands either capital or a partner who speaks fluent revenue.

What Happened and When

- Pre-June 26: Founder locked in suppliers and developed the tray and décor product set.

- June 26, 2026: Brand went live with a wholesale, wedding, and hospitality focus; founder opened a dual hunt for $50,000 in capital or a co-founder with sales, marketing, and operations expertise.

Where the Chips Fall

- Retail: The line nudges into gifting, bedroom accessories, wedding décor, and hotel supplies with minimal risk of bumping into incumbent brands—because incumbents rarely bother with custom-batch acrylic.

- E-commerce: Marketing spend aims to pull niche décor traffic online rather than wrestle Amazon in a price brawl, which is especially smart given Prime Day stretched June 23–26 and drew retaliatory discount fire from Target, Walmart, and Best Buy, leaving slim room for boutique launches to breathe.

What’s Next?

- Immediate: The next few months hinge on closing that $50,000 check or landing a co-founder who can turn stocked trays into purchase orders.

- Mid-term: Repeat wholesale placements in hospitality and wedding channels will decide if the niche is lucrative or just crowded.

- Long-term: No serial roadmap teased; survival depends on early margins and supplier reliability, plus proving physical home goods can still pull checks while capital floods toward AI infrastructure like Sarvam’s $234 million sovereign AI round backed by HCLTech and Hydra Host’s $100 million compute play. The broader personalization economy—laser engravers, embroidery rigs, and vending side-hustles—already shows low-entry hardware can print margins when the niche is tight enough.

This is physical-product minimalism with a straight face. The founder is not disrupting atoms or tokenizing furniture. They are simply wagering that a sharper tray at the right price still moves units. For $50,000 and an open co-founder seat, the thesis is as sturdy as the product needs to be: design earns margin, margin earns runway, and runway earns the right to design the next piece.

Comments ()