$216M Revenue, 79% Growth: Caris Life Sciences Just Made Precision Oncology Profitable

TL;DR

- $216M Revenue Surge: Caris Life Sciences Just Made Precision Oncology Profitable. Is Caris Life Sciences the next $1B acquisition target or a future IPO star?

- $4.2B Lesson: Kevin O'Leary Says Profit Motive Kills Startups. Are you building to flip or to last?

💰 Caris Life Sciences Just Dropped a $216M Mic Drop—And Wall Street Is Listening

Caris Life Sciences just dropped $216M in revenue (up 79% YoY) and flipped from losses to profit 💰 That's a diagnostics company growing faster than most SaaS startups — with 65% gross margins and positive cash flow. The secret? AI-powered oncology tools + a 61% pricing jump that actually stuck. Precision medicine isn't a lab experiment anymore — it's a revenue machine. What's your bet — acquisition target or IPO candidate? 🎯

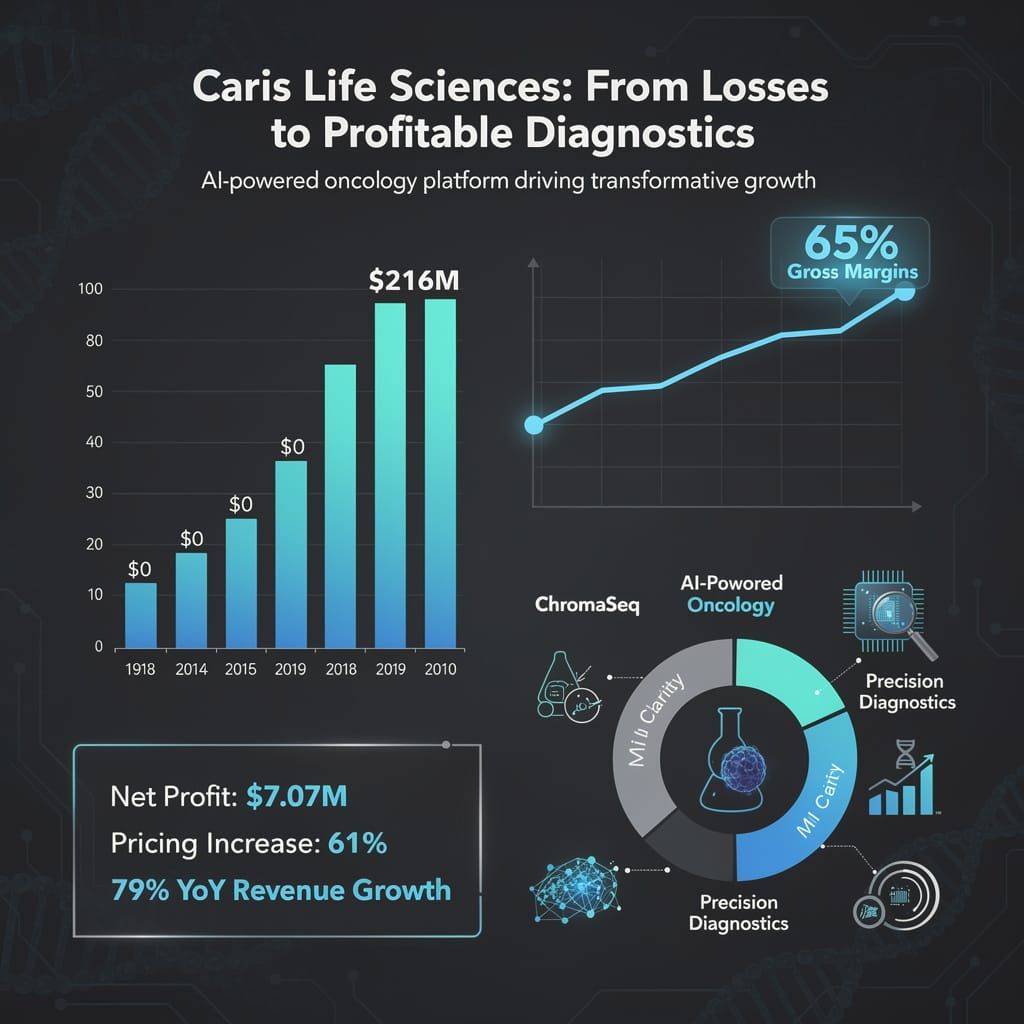

Let's be honest: when a diagnostics company says they've tripled revenue, you usually check for typos. But Caris Life Sciences isn't glitching. On June 19, 2026, the Irving, Texas-based precision oncology powerhouse casually announced it had pulled in $216.2 million in revenue—a 79% year-over-year surge that makes most SaaS companies look like they're running on dial-up.

And here's the thing: they're not alone. The broader market has been quietly rewarding companies that marry AI with real-world healthcare execution. Guardant Health posted record Q1 volumes and got full FDA clearance for Guardant360 Liquid in May. Leica Biosystems just launched an AI-powered digital pathology platform with Lunit and AstraZeneca. Even Milestone Scientific is getting analyst love post-Q1 for its CompuFlo platform and planned Medicare MAC engagement. The signal is clear: precision medicine isn't a lab experiment anymore—it's a revenue machine.

Wait, How Did They Do That?

Here's the short version: pricing power plus platform stickiness equals a very happy balance sheet.

- Revenue hit $216.2M—up 79% from the prior year.

- Gross margins landed at 65%, signaling healthy unit economics for a diagnostics firm (not easy in a world of lab coats and regulatory red tape).

- Adjusted EBITDA and free cash flow both turned positive, meaning Caris isn't just growing—it's growing profitably.

- Net profit clocked in at $7.07M, a stark reversal from prior losses.

The secret sauce? A 61% jump in pricing after a January disruption reset the sales trajectory. Combine that with restored volumes and an AI-powered multi-product oncology platform that includes tools like ChromaSeq and MI Clarity, and you've got a recipe that's less "startup gamble" and more "precision-guided missile."

Key insight: Caris isn't selling one test. It's selling a diagnostic ecosystem—and oncologists are buying.

The AI Angle Nobody's Talking About

We hear "AI in healthcare" so often it's practically white noise. But Caris is quietly proving that AI-driven early cancer detection isn't a buzzword—it's a revenue driver.

Their platform uses machine learning to spot malignancies earlier, with higher accuracy, and across more cancer types than traditional methods. The result? Early detection rates climbed significantly among tracked patients. That's not just good medicine—it's a cost-saver for health systems, which makes insurers and hospital networks more willing to pay those higher prices.

And Caris isn't the only one riding this wave. Guardant Health's multi-cancer detection platform Shield just expanded into Asia through a partnership with Manulife. Leica's new AI-powered companion diagnostic for PD-L1 testing (built with AstraZeneca) is designed to reduce inter-pathologist variability. The industry is converging on a simple truth: AI doesn't replace the doctor—it makes the doctor's call more accurate, faster, and cheaper.

The causal chain is straightforward:

- Better algorithms → earlier detection → better outcomes → lower system costs → willingness to pay premium pricing → $216M in revenue.

Where's the Risk?

Because nothing this good comes without a catch.

- Healthcare reimbursement remains a wildcard. If Medicare or private payers push back on pricing, that 61% increase becomes a ceiling, not a floor. Guardant Health's FDA clearance for Guardant360 Liquid was a positive signal, but the broader reimbursement landscape is still fragmented. The Senate Democrats just launched an inquiry into FDA vaccine policy changes on June 18, and the FTC is suing the World Professional Association for Transgender Health over alleged fraudulent marketing. Regulatory scrutiny is everywhere—and diagnostics won't escape it.

- Execution dependency. Caris is riding a wave of restored sales momentum. Any operational slip—lab bottlenecks, data pipeline issues, regulatory hiccups—could stall the flywheel. The Hades campaign compromising Python packages via Bun in early June is a reminder that AI-dependent ecosystems face supply-chain vulnerabilities too.

- Competition is waking up. Ionis Pharmaceuticals reported that 49% of treated patients achieved serum antigen below 100 IU/mL with bepirovirsen therapy—a 19% functional cure rate versus 0% in the placebo group. That's not a direct competitor to Caris, but it signals a broader biotech renaissance where everyone is chasing precision. Meanwhile, Corcept Therapeutics and Ideaya Biosciences both posted positive trial data in June, and Silence Therapeutics reported a 59% overall remission rate in its FELIX study for cancer patients. ASCO 2026 was basically a victory lap for precision oncology: daraxonrasib doubled survival in pancreatic cancer, mRNA vaccines cut melanoma recurrence in half, and VERVE-102 permanently edited the PCSK9 gene to lower LDL by 62%. The bar is rising fast.

- Macro volatility is real. The Fed's hawkish stance, rising US-Iran tensions, and Broadcom's AI-focused earnings miss on June 4 triggered a broader tech sell-off. AI chip supply constraints (Nvidia's Rubin CPX delay) and semiconductor bottlenecks are creating pricing pressure across the entire AI stack—including diagnostics hardware. The broader market dropped 9.3% in early June. That kind of volatility doesn't spare healthcare.

- Consumer safety and regulatory blowback. ByHeart and Nara Organics infant formulas were linked to botulism cases on June 18. Energy-drink lawsuits are under investigation. The FDA is facing pressure to reconsider accelerated drug approval processes. When consumer trust erodes across the healthcare sector, even well-run diagnostics companies feel the ripple effects.

What Happens Next?

The forecast pencils out nicely—for now.

- Short-term (Q3 2026): Revenue likely continues upward as diagnostic algorithms improve and more health systems adopt AI-assisted screening. Watch for another pricing adjustment. Guardant Health's guidance remains optimistic, and Leica's AI pathology rollout suggests the sector is gaining institutional traction. Milestone Scientific's push for Category I CPT authorization could open new reimbursement pathways.

- Mid-term (2027): Platform expansion into new cancer indications could unlock additional revenue streams. Margins may compress slightly as R&D spend ramps. Caris's long-term upside is tied to blood-based diagnostics and scalable AI models—both of which are seeing increased investment across the sector. The NIH just terminated two diversity-enhancing PhD programs on June 18, which signals shifting federal priorities in biomedical research funding that could affect talent pipelines.

- Long-term (2028+): If Caris maintains its pricing power and keeps gross margins above 60%, it becomes a prime acquisition target for larger diagnostics players—or a strong IPO candidate if it chooses to stay independent. The broader trend of AI-driven healthcare consolidation (Dominion Energy's NextEra acquisition, Wiley's Emerald Publishing buyout adding $30M in synergies) suggests that well-positioned platforms don't stay independent forever.

The Bottom Line

Caris Life Sciences isn't just a diagnostics company with a good quarter. It's a signal that precision oncology has entered its commercial prime. The combination of AI-powered detection, aggressive pricing, and operational discipline has produced a rare beast: a healthcare company that grows fast and makes money.

For investors, founders, and anyone watching the intersection of AI and biotech, this is the kind of case study you bookmark. In a market where Broadcom misses and Nvidia faces chip delays, Caris is doing something almost rebellious: making money while saving lives.

Caris didn't just beat expectations. It redefined them.

Reported: Monday, June 22, 2026 | Sources: Caris Life Sciences earnings release, Ionis Pharmaceuticals clinical data, Guardant Health Q1 results, Leica Biosystems/Lunit partnership announcement, Milestone Scientific Q1 strategic update, ASCO 2026 clinical trial data (daraxonrasib, mRNA melanoma vaccine, VERVE-102), Fed Beige Book, Broadcom earnings report, FDA regulatory updates, Senate inquiry into vaccine policy, FTC lawsuit against WPATH, infant formula botulism cases, industry analysis.

🦈💀 The $4.2 Billion Lesson: Why Kevin O'Leary Thinks You're Building Your Startup Wrong

Kevin O'Leary just said profit motive is a startup-killer. 🦈💀 The man who made his name ripping into founders on Shark Tank is now warning that chasing money destroys companies. SoftKey sold for $4.2B. Got gutted. Brand dead. Customers confused. Execs rich. Since 2023: 431 startups shut down. 220+ unicorns lost half their value. Four AI firms swallowed 65% of $300B in Q1 funding. The system rewards narrative over traction. Exit culture over execution. But here's the twist: mission-driven founders are statistically more resilient. Purpose is becoming a competitive advantage. Are you building to flip—or to last? 🤔

"If you're in it for the money, you've already lost."

That's not some wellness influencer's Instagram caption. That's Kevin O'Leary—Mr. Wonderful himself—saying it on June 19, 2026, in what might be the most self-aware moment a venture capitalist has ever had in public.

Let that sink in for a second. The man who made his name on Shark Tank by eviscerating founders who didn't know their margins is now warning that pure profit motive is a startup-killer. When a shark tells you the water's dangerous, it's worth listening.

The SoftKey Ghost That Haunts Silicon Valley

O'Leary didn't just throw out a generic warning. He went to the vault—specifically, to SoftKey's $4.2 billion sale and the cautionary tale of The Learning Company.

Here's the short version of a long tragedy: SoftKey built something real. Then the acquisition machinery kicked in. The Learning Company got swallowed, stripped for parts, and what remained was a hollow shell where product depth used to be. The executives walked away rich. The customers walked away confused. The product walked away dead.

O'Leary's point? That pattern isn't an anomaly. It's the playbook.

- SoftKey (1990s): $4.2B exit → product gutted, brand destroyed, consumer trust vaporized

- Zume (2023): $446M raised for robot-made pizza → pivoted to packaging, then shut down

- Olive (2023): $4B valuation peak → halted operations, capital exhausted, no market fit

- Convoy (2023): Market downturn → ceased operations despite $3.8B valuation

- 220+ unprofitable unicorns (2024–2026): Collapsed post-ChatGPT as AI disruption devalued legacy software models

- Modern VC culture: Same incentives, different decade

The mechanics are brutally simple. Since 2023, 431 VC-backed startups have shut down—72% of them showed declining health via CB Insights' Mosaic score a full 22 months before collapse. By June 2026, over 220 unprofitable unicorns had lost more than 50% of their peak value, their business models gutted by the rapid shift toward AI-native solutions. Falling partnerships and shrinking teams preceded every death. Psychological pricing pressures push founders to prioritize revenue velocity over research rigor. Quantitative metrics (ARR, MRR, growth rate) replace qualitative impact assessments. And somewhere in that spreadsheet shuffle, the actual problem the startup was supposed to solve gets lost.

The real kicker? Venture capitalists are now openly rewarding polished narratives over hard metrics. A May 2026 signal from the global VC ecosystem shows founders being pushed to prioritize visibility over substance. Catalytic capital is being misunderstood as mission-driven play money rather than proof capital. And Singapore's $37 billion RIE2030 plan explicitly identified a commercialization gap—too much research, not enough market alignment. The ecosystem is admitting it has a problem.

Meanwhile, the macro environment is making this worse. By June 2026, $300 billion in record Q1 venture funding had flowed—but four AI firms swallowed more than 65% of it. The rest of the ecosystem is fighting over scraps while LPs demand cash back. If you're building a non-AI startup in 2026, you're not just competing against other founders. You're competing against Anthropic's $65B Series H and OpenAI's $852B valuation. Good luck.

The Two-Headed Monster: Exit Culture vs. Execution Culture

What O'Leary identified isn't just a bad habit—it's a structural misalignment baked into how venture capital works.

| Exit Culture | Execution Culture |

|---|---|

| Optimizes for acquisition value | Optimizes for customer value |

| Rewards financial engineering | Rewards product depth |

| Measures in multiples | Measures in impact |

| Timeline: 3–5 years | Timeline: 10+ years |

The data backs him up. Mission-driven founders—those who can articulate why they exist beyond the cap table—show statistically higher resilience during downturns. They retain talent longer. They pivot smarter. They don't panic-sell when a term sheet shows up.

Meanwhile, the purely market-driven crowd? They're the ones getting divorced, liquidating assets, and burning out before their Series B. O'Leary explicitly flagged wealth erosion via divorce and asset liquidation as a growing founder risk exposure. When your identity is tied to your valuation, a down round feels like a death sentence.

And here's where the macro environment makes it worse. Robert Kiyosaki—not exactly a wallflower—spent late 2025 warning that a "major financial crash" is imminent, predicting gold at $27,000/oz and silver at $100/oz by 2026. In June 2026, he doubled down: gold at $35,000/oz by 2035. Whether you buy his thesis or not, the signal is clear: capital preservation is replacing growth-at-all-costs as the dominant investor mindset. Oil hit $150/barrel in early June 2026 before settling at $83 after the U.S.–Iran deal. The Strategic Petroleum Reserve dropped to its lowest since 1983. US markets fell 9.3% from all-time highs. Founders who built for a bull market are now exposed to a very different reality.

What This Means for You (Yes, You)

If you're building a startup right now, here's what the O'Leary signal tells you:

The bad news: The VC machine is still optimized for extraction, not creation. If you follow the standard playbook—raise big, grow fast, exit faster—you're statistically more likely to end up with a hollow company and a personal life in shambles. 431 dead startups since 2023 and 220+ unicorns losing half their value is not a bug. It's a feature of a system that rewards narrative over traction. Even the tools meant to help you—like AI coding assistants—come with hidden costs: a June 2026 study found that 16 out of 30 tested language models took unnecessary steps when asked to write a simple "hello world" program, burning between 55 and 3,676 tokens on overcomplication. If your AI tools can't even say hello efficiently, what's your pitch deck doing?

The good news: The market is starting to punish that behavior. Investors are getting smarter about distinguishing between growth and value. Founders who can demonstrate durable product-market fit—not just hockey-stick charts—are commanding better terms. Tools like IdeaGrit (launched June 2026) now offer pre-mortem analysis that flags structural risks using lessons from six failed startups. Sentry Memory (4.7★ Chrome extension) helps founders stop re-explaining their projects to AI tools. The ecosystem is building its own antibodies.

The practical steps:

- Revisit your incentive structure. Are your KPIs measuring what matters, or what's easy to measure?

- Build equity-aligned metrics. Tie compensation and milestones to long-term outcomes, not just quarterly growth.

- Schedule independent outcome reviews. Bring in outsiders who don't have a financial stake in your exit narrative.

- Fix your board meetings. A June 2026 webinar by Chris Fenster revealed that inconsistent communication is the #1 driver of investor distrust—even when founders are making operational progress. Don't let silence create suspicion.

- Watch your AI dependencies. The Anthropic Fable 5 and Mythos 5 models were taken offline on June 13 under a government export directive. If your product relies on someone else's model, you're building on rented land.

The Long View: What Recovery Looks Like

O'Leary's warning isn't a death knell—it's a diagnosis. And diagnoses, inconvenient as they are, come with treatment options.

The structural recalibration needed:

- Founder incentives → Shift from "exit value" to "enterprise durability"

- Investor expectations → Longer time horizons, qualitative impact metrics

- Board governance → Independent oversight of product depth vs. financial extraction

The forecast is cautiously optimistic: mission-driven founders are proving statistically more resilient than their purely market-driven counterparts. The divergence is already visible in the data. The question is whether the broader ecosystem will catch up.

And if the macro environment continues deteriorating—geopolitical tensions in the Middle East, a U.S.–Iran ceasefire that could unravel, markets still 9.3% off highs, and the Bank of Japan raising rates to 1% while the Fed deliberates—the startups that survive won't be the ones with the best pitch decks. They'll be the ones that actually solve problems people will pay for, regardless of what the Nasdaq does tomorrow.

The Bottom Line

Kevin O'Leary, of all people, just told you that money isn't the point. If you're building a startup, you should probably listen.

Not because altruism pays the bills—it doesn't. But because the evidence is mounting that purpose is a competitive advantage. Companies built to solve real problems, for real people, with real depth, tend to outlast companies built to flip.

And in a world where 431 startups have already died, 220+ unicorns are bleeding value, the Strait of Hormuz just reopened after a blockade that sent oil to $150, and Anthropic had to pull its best models off the market due to government directive—outlasting everyone else is starting to look a lot like winning.

This article was composed on June 22, 2026, based on signals from the startup ecosystem and public statements made by Kevin O'Leary on June 19, 2026.

Comments ()