£9.8B Gilt Sell-Off: UK Fiscal Instability Risks Systemic Collapse

TL;DR

- £9.8 Billion Gilt Sell-Off: UK Fiscal Instability Hits 5% Yield Threshold Amid Leadership Vacuum. Is the UK's fiscal instability making US Treasuries the only safe haven for wealth managers?

- 4.3% GDP Growth: China's Export Surge Masks Domestic Stagnation and Job Losses. Is China's 4.3% GDP growth a real recovery or just a tech-export mirage masking a domestic collapse?

- 50.3 PMI: China's Export Surge Masks Domestic Retail Collapse and Tariff Panic. Is China's marginal PMI recovery a sign of strength or a desperate scramble to beat US tariffs?

📉 The Gilt Gap: Britain's Fiscal Mirage

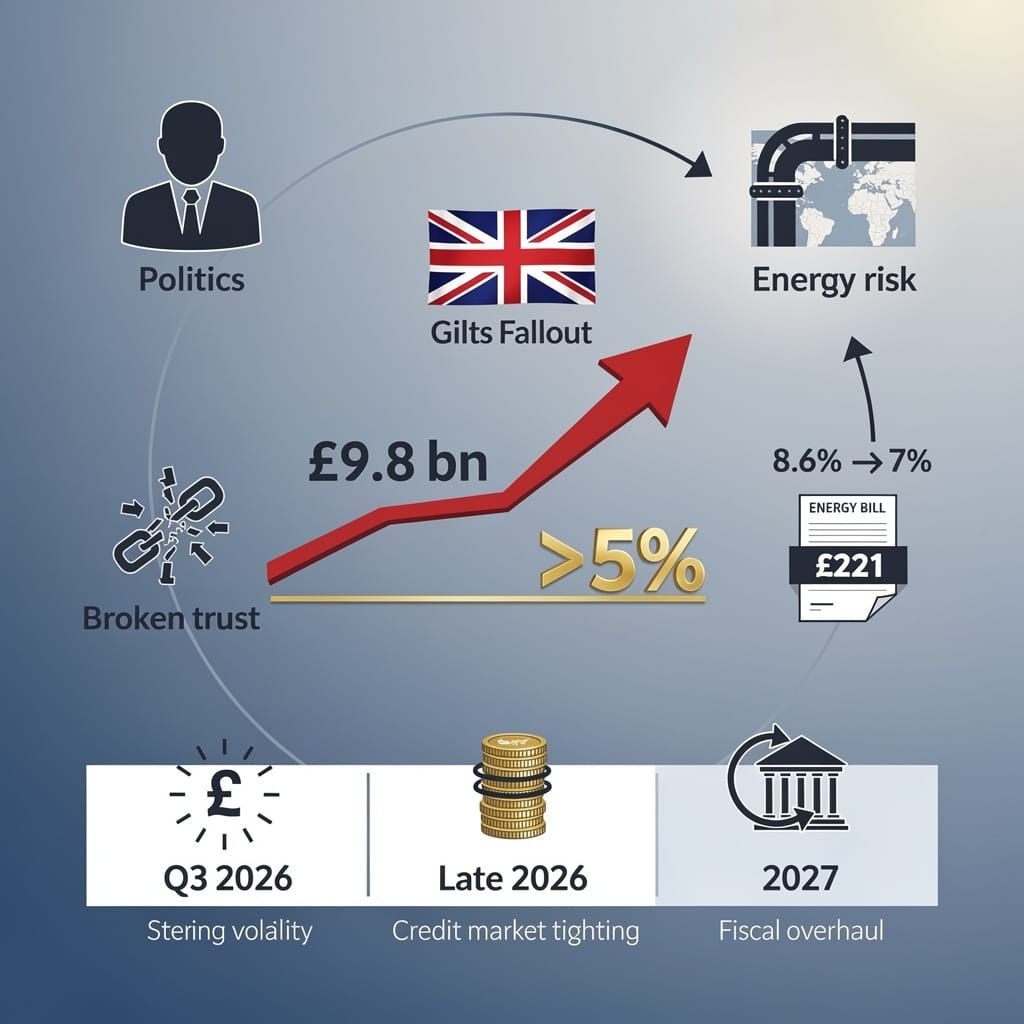

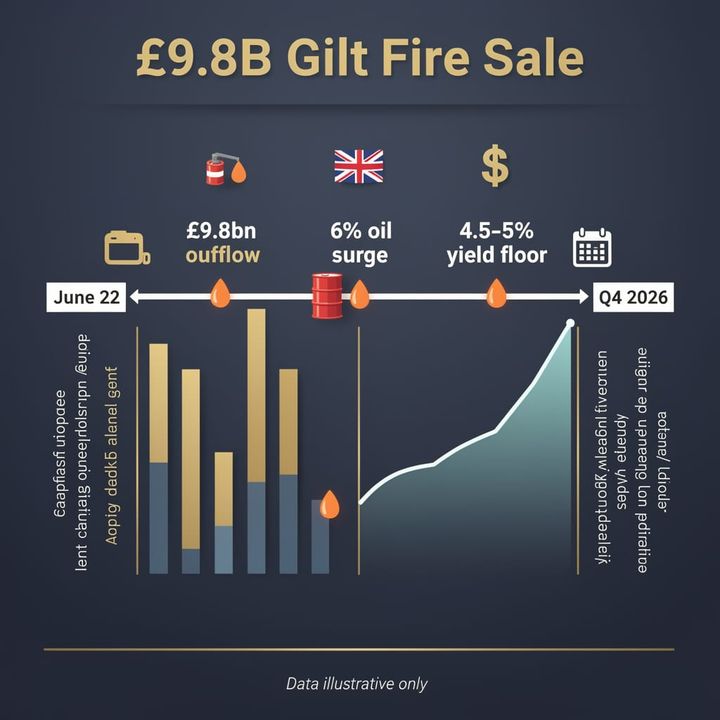

£9.8 billion dumped. A staggering exodus of Gilt holdings—equivalent to the entire annual budget of several mid-sized cities—in a single flash 📉. Political vacuums and oil shocks are shredding confidence. Treasury 'reassurance' or just more noise? UK investors: are you fleeing to US Treasuries too?

On July 14, 2026, the UK financial market demonstrated institutional fragility as city wealth managers dumped £9.8 billion in UK Gilts. This sell-off, triggered by fears of fiscal irresponsibility ahead of Andy Burnham’s appointment, pushed yields above the 5% threshold. This movement indicates a sharp decoupling between government fiscal promises and investor confidence, resulting in a rapid reallocation of capital away from UK sovereign debt.

Why is the Market Panicking?

The volatility stems from a causal chain of political and geopolitical instability. The resignation of Sir Keir Starmer on June 21, effective June 22, created a leadership vacuum that intensified market skepticism. This instability coincides with a macro risk cascade: renewed attacks along the Strait of Hormuz on July 14 surged oil prices by over 6%, fueling fears of tighter monetary policy and higher borrowing costs.

While the government attempts to manage the fallout, structural deficits persist. Since Q1 2026, the UK has borrowed a record £4.79 billion, while households face annual energy bill increases of £221. This fiscal trajectory enables a feedback loop: as yields rise to combat inflation and instability, the cost of servicing liabilities increases, further straining a budget already under scrutiny.

Systemic Failures:

- Fiscal Trust: Wealth managers (including Rathbones and Aberdeen Investments) exiting gilts → yields hitting new highs since May.

- Capital Attraction: Foreign investment share dropped from 8.6% to 7% → diminished global competitiveness.

- Energy Exposure: Supply chain shocks in the Strait of Hormuz → increased inflationary pressure and consumer debt risk.

What Follows the Spike?

The current trajectory projects a period of forced regulatory recalibration. The reliance on Bank of England interventions—which are hampered by global trends and a 40% probability of US Fed rate hikes—demonstrates that the UK's financial guardrails offer minimal protection against systemic shocks.

- Q3 2026: Persistent volatility in Sterling as markets test the 5.5% yield floor.

- Late 2026: Tightening of domestic credit markets, potentially reducing corporate investment.

- 2027: Mandatory overhaul of fiscal rules to restore minimum investor trust.

Institutional Response

- Treasury: Attempting reassurance → results in increased skepticism due to policy instability.

- Bank of England: Monitoring yield curves → enables limited intervention amid global tightening.

- Investors: Shifting to US Treasuries → accelerates the devaluation of UK-based portfolios.

📉 The Export Mirage: China's Unbalanced Growth

4.3% GDP growth—a hollowed-out record. That is roughly the speed of a slow walk while the internal economy collapses 📉. Tech exports surge 27% but citizens stay paralyzed by a dying property market. A recovery for robots, not people? China — is your local economy actually feeling this growth?

China reported a 4.3% annual GDP expansion as of July 15, 2026—the lowest rate since Q4 2022. This figure misses forecasts and masks a deepening systemic fracture. The growth relies almost exclusively on a narrow corridor of high-tech exports, while the internal engine of the economy stalls.

Is Export Growth a Sustainable Shield?

External demand props up headline numbers, enabling the IMF to raise its growth forecast to 4.6%. However, this creates a causal chain where industrial success exists in isolation from the average citizen. While a reported 27% month-on-month surge in exports—driven by AI and EV demand—bolstered a record trade surplus of $99 billion, the domestic consumer remains paralyzed by a collapsing property market.

The Consumption Gap:

- Retail Sales: A 1.0% marginal rise on July 15 followed a 0.6% dip in May, demonstrating a fragile rebound that fails to offset broader stagnation.

- Property Investment: The sector continues to weaken amid job concerns; luxury transaction volumes in connected hubs like Hong Kong declined 30% QoQ, while mainland buyers struggle as equity erases.

- Labor Market: Manufacturing PMI hit 50.3 on June 30, yet this AI-driven efficiency accelerates displacement. A 20% increase in industrial robot installations since 2018 correlates with a 9.5% drop in secondary-sector employment.

This divergence indicates a hollowed-out recovery. The economy demonstrates a two-tier system: a booming tech-export sector and a stagnant domestic core. The result is an imbalance where growth is exported rather than experienced internally.

Timeline of Projections:

- July 24, 2026: Politburo meeting determines the depth of targeted stimulus to address labor market resilience.

- Q3 2026: GDP projects to inch toward 4.4%, contingent on whether compensatory stimulus materializes.

- Year-End 2026: Central bank forecasts 4.6% growth, though structural adjustment risks persist as domestic spending lags.

Structural Stress Points:

- Tech Focus: 27% export spike → increased dependence on U.S. order intake and geopolitical shipping stability.

- Housing: Property sector weakness → drained household savings → muted discretionary expenditure.

- Labor: AI-powered automation → systemic job displacement → stagnant local wages.

The current trajectory demonstrates that while the state can manufacture growth via exports, it cannot mandate consumer confidence. Relying on the world to buy AI hardware while the secondary sector loses nearly 10% of its workforce is not a recovery; it is a precarious redistribution of risk.

📉 The Export Illusion: China's PMI "Recovery"

50.3 PMI: a pathetic flicker of growth. This marginal gain is just a panic pivot—factories dumping chips into the US to beat tariffs before the door slams shut 📉. Domestic retail is actually tanking. China — Is your portfolio betting on this fragile facade?

China’s manufacturing data presents a fragile facade of stability. By June 1, 2026, the Manufacturing PMI hit a flat 50.0, signaling total stagnation. While it clawed back to 50.3 by June 30, these figures barely scrape the contraction threshold. This marginal "growth" relies on an export order sub-index of 50.1—a number suggesting a rebound only if one ignores the desperation driving the volume.

Is this growth or a panic pivot?

The surge in AI and semiconductor exports is not a sign of organic strength, but a tactical scramble. Factories are aggressively pushing components into the U.S. market to front-run escalating tariffs, supported by falling unit costs and holiday pre-orders from U.S. retailers. This defensive posture is reflected in record semiconductor export volumes, though this relies on external AI investment rather than internal health.

While the state highlights these spikes, the domestic reality is a collapse. May retail sales fell 0.6% YoY—the first monthly drop since December 2022—driven specifically by a slump in auto and appliance purchases. This erosion of household wealth, compounded by sliding fixed-asset investment (-4.1%), directly suppresses local demand.

This causal chain—where domestic failure forces an over-reliance on foreign demand—results in a precarious economic structure. Even with the IMF raising growth forecasts to 4.6%, the reliance on an "export-first" strategy to circumvent sanctions demonstrates that external shipments are merely masking internal stagnation.

Market Realities

- Domestic Consumption: Retail sales drop 0.6% → reduced auto/appliance spend → failure to absorb industrial overcapacity.

- Trade Strategy: Tariff pressure → AI/chip export surge → temporary PMI inflation to 50.3.

- Systemic Risk: Export dependence → vulnerability to U.S. policy shifts → fragile recovery limited by property downturn.

Forecasted Trajectory

- Q3 2026: GDP projects toward 4.6%, supported by AI hardware demand but capped by weak household sentiment.

- Q4 2026: Potential correction in export volumes as tariff-avoidance windows close, threatening to drag PMI below 50.0.

- 2027 Outlook: Critical necessity to pivot toward domestic consumption or face continued reliance on volatile foreign markets.

Sectoral Comparison AI/Chips: High export volume → short-term revenue spikes, extreme long-term tariff exposure. Real Estate: Fixed-asset investment contracted 4.1% → systemic drag on non-manufacturing sentiment. Retail: Weak consumer confidence → 0.6% YoY decline in May sales.

Comments ()