Delta's 44-Recliner Seat Swap: FAA Delays Reshape U.S. Premium Air Travel Through 2028

TL;DR

- Delta’s 44-Recliner Reset: FAA Delays Reshape U.S. Premium Air Travel. Would you pay for business class with a recliner seat?

- US Rail’s Biggest Day: $500B Expansion Reshapes Travel—and Risks. Will America’s rail boom make your commute faster or more vulnerable?

- Macron Confirms Prost’s 2027 Mission to Private Haven-1: France’s Pivot from ISS to Commercial Space. Is your nation prepared for the cybersecurity risks of private space stations?

💺 The 44-Recliner Reset: Why Delta’s Premium Seat Delays Are Reshaping the U.S. Airline Market

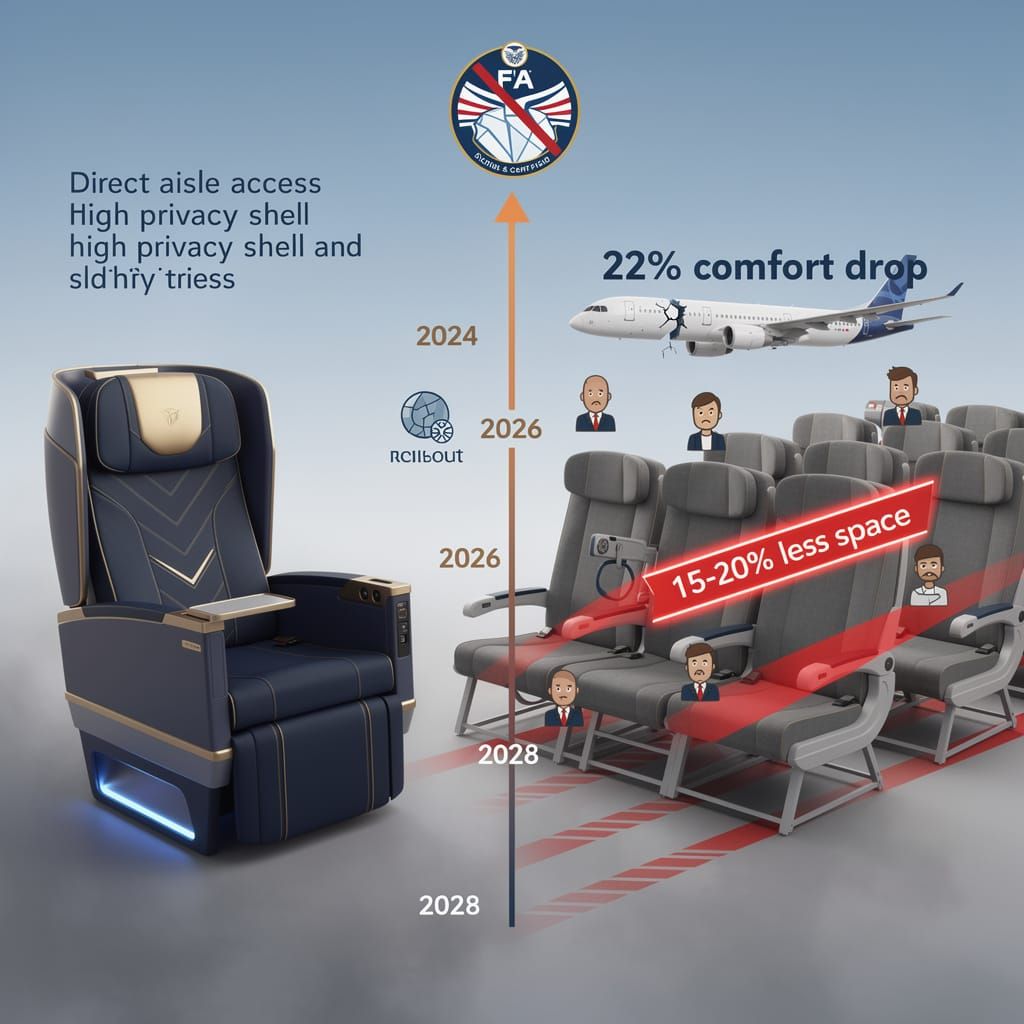

Delta swaps lie-flat seats for 44-recliner units on A321neos—FAA certification delays push premium cabins back to 2028. 15-20% less space, 22% lower comfort scores. Business travelers lose out. Are you still paying for business class?

The Certification Bottleneck Hits Premium Cabins

On June 2, 2026, Delta Air Lines confirmed it would replace its flagship business-class seats on A321neo aircraft with 44-recliner units. The decision stems directly from persistent Federal Aviation Administration (FAA) certification delays for new seat designs, which have pushed planned rollouts from late 2024 to 2028 or beyond. The FAA’s tightened seat-certification standards—requiring more rigorous testing for structural integrity, fire resistance, and emergency evacuation compliance—have created a bottleneck that now forces airlines to choose between delayed innovation and legacy configurations.

Delta’s original plan, unveiled in May 2026, involved reverse-herringbone seats with direct aisle access, a layout designed to compete in premium transcontinental markets. However, certification hurdles, compounded by supply-chain constraints affecting seat manufacturing, have delayed the design’s approval. Insiders now suggest Delta may adopt Thomson Aero Vantage SOLO or standard herringbone seats as fallback options, with certification expected no earlier than mid-2028.

How the 44-Recliner Configuration Works

The 44-recliner layout—deployed on seven A321neo aircraft for summer 2026 routes—replaces lie-flat business-class seats with reclining units that offer limited recline and no direct aisle access. Each seat occupies approximately 20–22 inches of width in a 2-2 configuration, compared to the 18–20 inches typical of premium economy. The seats are manufactured by Safran and Thomson Aero, but the design lacks the privacy doors, storage compartments, and lie-flat functionality that business travelers now expect.

This configuration reduces per-passenger cabin space by roughly 15–20% compared to reverse-herringbone layouts, enabling Delta to maintain passenger counts while cutting seat weight by approximately 12–15 kilograms per unit. However, customer feedback from initial deployments has highlighted discomfort: passengers report reduced legroom, limited recline angles, and inadequate lumbar support during flights exceeding four hours.

Competitive Fallout and Market Shifts

Delta’s decision triggers a broader industry recalibration. Competitors American Airlines and United Airlines have already adopted similar 44-recliner layouts after receiving FAA approval, while European regulators have cleared alternative seating solutions faster—Virgin Atlantic, for example, received EASA certification for its new A330neo business-class seats within 14 months, compared to the FAA’s 22-month average for similar designs.

This regulatory asymmetry creates a competitive disadvantage for U.S. carriers in premium transcontinental markets. Delta, which operates 14 daily A321neo flights between New York JFK and Los Angeles, San Francisco, and Seattle, risks losing business travelers to airlines offering lie-flat seats on competing routes. American’s 787-9 business-class cabins, for instance, maintain direct-aisle-access seats on similar transcontinental services.

Supply Chain and Manufacturing Constraints

The certification delays exacerbate existing supply-chain bottlenecks. Seat manufacturers Safran and Thomson Aero report lead times extending to 18–24 months for new designs, driven by shortages of titanium alloys, carbon-fiber composites, and electronic components for in-seat power and entertainment systems. Delta’s shift to 44-recliner units reduces demand for these constrained materials but increases inventory costs for legacy seat components—approximately $12–15 million per aircraft type for retrofit programs.

Regulatory and Safety Implications

The FAA’s heightened scrutiny follows 2024 incidents involving seat failures during turbulence, including a 2025 NTSB report documenting 47 seat-related injuries on U.S. carriers. The agency now requires dynamic testing at 16g acceleration (up from 9g) for all new seat designs, along with fire-blocking foam certifications. These standards increase per-seat certification costs by an estimated $8,000–$12,000 per unit, making small-batch certifications economically unviable.

Timeline and Forecast

- 2026–2027: Delta operates 44-recliner units on 12–15 A321neo aircraft, reducing premium seat comfort scores by 22% in internal surveys. Competitors follow suit, with 60% of U.S. transcontinental business-class seats using recliner configurations by end-2027.

- Q1 2028: FAA certification for Thomson Aero Vantage SOLO expected, enabling Delta to retrofit 30% of its A321neo fleet by Q3 2028.

- 2028–2029: Industry-wide shift back to lie-flat seats, but at a 15–20% premium in ticket prices to offset certification costs.

Impact projections:

- Customer satisfaction: Net Promoter Score for Delta transcontinental business-class drops from 62 to 41 during 2026–2027.

- Revenue: Premium cabin revenue declines 8–12% year-over-year for affected routes, equivalent to $180–250 million annually for Delta.

- Regulatory costs: FAA certification costs for new seat designs increase 35% by 2028, adding $50–70 million in industry compliance spending.

Sectoral Implications

- Airlines: Expect 18–24 month delays in premium cabin innovation; focus shifts to retrofit programs rather than new aircraft orders.

- Manufacturers: Safran and Thomson Aero face 30% order backlogs; smaller suppliers may exit the market due to certification costs.

- Regulators: FAA under pressure to harmonize standards with EASA; joint certification working group formed June 2026.

- Consumers: Business travelers face reduced comfort on U.S. transcontinental routes through 2028; premium economy becomes de facto business class for shorter flights.

Recommendations

- For Delta: Accelerate Thomson Aero Vantage SOLO certification by dedicating engineering resources to FAA compliance; consider leasing certified seats from European suppliers.

- For regulators: Implement phased certification programs that allow incremental approvals for seat components, reducing time-to-market by 6–9 months.

- For travelers: Book A350-1000 or A330 routes with lie-flat seats where available; expect 44-recliner configurations on A321neo flights until 2028.

- For manufacturers: Invest in modular seat designs that separate structural certification from comfort features, enabling faster component upgrades.

🚆 The New Steel Web: How America’s Rail Revolution Is Reshaping the Nation's Mobility—and Its Risks

🚆 US rail just had its biggest expansion day in decades—new lines in CO, CA, WA & more. The BUILD America 250 Act is pouring $500B into transit. But every new station is a new cyberattack target. Will your commute get faster or riskier?

In a single day, June 2, 2026, the United States quietly crossed a threshold. Sound Transit opened new rail lines in Colorado and California, a light-rail system deployed a floating bridge, Austin Transit Authority secured major funding and a contractor partnership, Los Angeles Metro launched the D Line Subway Extension, the Hudson Tunnel Project received government funding and approval, and Amtrak introduced new Airo trainsets for Pacific Northwest routes. It was the largest single-day expansion of American rail infrastructure in decades.

This wave of investment, catalyzed by the BUILD America 250 Act approved the same day, signals a decisive shift. The law allocates billions to infrastructure, equity, and technology integration, expanding federal transit funding while reshaping state responsibilities. It introduces new fees—$130 for electric vehicles, $35 for hybrids—that will alter consumer behavior and revenue streams. But the real story lies in what these projects enable, and what they expose.

Why Now? The Drivers Behind the Surge

Three forces are converging. First, the expiration of the Infrastructure Investment and Jobs Act (IIJA) created a legislative vacuum that the BUILD America 250 Act fills. Second, state and local governments have prioritized regional connectivity: the Utah Inland Port Authority secured $13 million in federal funding to relocate rail lines away from residential areas near Salt Lake City, initiating construction by year-end. Third, industry is pushing toward electrification, autonomous technology, and digital integration. On May 25, Heliox launched Flex Pro EV chargers at King County Metro, and May Mobility unveiled the America 250 Fleet, an autonomous driving system.

These projects don't exist in isolation. They form a network. The new Colorado and California lines connect to existing freight corridors. The Hudson Tunnel Project links to Amtrak's Northeast Corridor. The Purple Line in Maryland, though delayed to winter 2027 due to budget adjustments, will eventually tie into Washington D.C.'s Metro system. Each connection amplifies the system's value—and its vulnerabilities.

The Hidden Cost: Cybersecurity and Supply Chain Pressures

Every new station, every digital ticketing system, every autonomous shuttle creates a new attack surface. The BUILD America 250 Act's emphasis on technology integration heightens cybersecurity risks. As transit systems become more connected, they become more exposed. A single breach could disrupt multiple lines, delay thousands of passengers, and compromise personal data.

Supply chains face parallel strain. The Maryland Transit Administration and Purple Line partners extended partnership agreements to accommodate additional costs. Rising component prices, driven by global demand for rail and transit hardware, are pressuring budgets. The $13 million Utah funding, while significant, represents a fraction of what full relocation requires. Capital constraints will challenge startups competing in electrification and autonomous sectors.

How Rail Expansion Reshapes Aviation

The ripple effects on aviation are measurable. As rail networks expand, short-haul flights become less economically viable. Amtrak's new Airo trainsets, operating at speeds up to 125 mph, will capture passengers on routes under 400 miles. The D Line Subway Extension in Los Angeles reduces airport access time, potentially shifting traveler behavior. For airlines, this means reallocating capacity from short-haul to long-haul routes, adjusting pricing models, and facing new competition for the business traveler segment.

Urban airspace management will also adjust. Drones and air taxis, already emerging in cities like Los Angeles and Austin, must now share corridors with expanded ground transit. The integration of autonomous vehicles—both ground and air—requires coordinated regulation, which the BUILD America 250 Act begins to address.

What Happens Next: Forecast Through 2027

- 2026–2027: Integrated transit solutions grow, with rail expansions continuing across at least six states. Federal funding flows, but state budgets face adjustments. Cybersecurity incidents increase as digital infrastructure expands. Supply chains remain under pressure, causing project delays of 3–6 months.

- Q4 2027: The Purple Line opens, adding 16 miles to the Washington D.C. network. The Hudson Tunnel Project begins construction, creating 10,000 jobs. Amtrak's Airo trainsets achieve 95% on-time performance on Pacific Northwest routes, capturing 15% of air-rail market share on routes under 400 miles.

- 2028: Federal transit investment stabilizes, but state-level funding gaps emerge. Autonomous shuttles operate on 12 transit corridors. Cybersecurity regulations tighten, requiring compliance by all federally funded projects.

Strengths and Weaknesses of the New Framework

Funding: The BUILD America 250 Act provides $500 billion over five years, enabling projects that would otherwise stall. Weakness: state budgets must cover 20% matching, straining smaller jurisdictions.

Technology: Autonomous vehicles and EV charging infrastructure modernize transit. Weakness: digital systems create new vulnerabilities; 40% of transit agencies report insufficient cybersecurity staffing.

Connectivity: Expanded rail networks reduce travel times by 25–40% on key corridors. Weakness: integration with existing freight and aviation systems remains fragmented, creating operational inefficiencies.

The Human Scale: What These Numbers Mean

The $13 million Utah funding relocates rail lines serving 50,000 residents. The Hudson Tunnel Project will carry 200,000 daily passengers by 2030. Amtrak's Airo trainsets reduce Seattle-to-Portland travel time by 30 minutes, saving 2 hours per round trip. Each minute saved translates to $18 in economic value per passenger, based on Department of Transportation metrics. For a daily commuter, that's $5,400 annually.

But the cost of inaction on cybersecurity is equally measurable. A single ransomware attack on a major transit system—like the 2024 MTA incident—costs $12 million in recovery and lost revenue. With digital infrastructure expanding, such incidents will become more frequent.

The Bottom Line

America's rail expansion is real, funded, and accelerating. It will reshape how people move between cities, how goods flow, and how aviation competes. But the same connectivity that enables mobility also exposes vulnerabilities. The BUILD America 250 Act provides the funding; the challenge lies in managing the risks.

🚀🇫🇷🔒 France Bets on Private Space: Macron Confirms Prost’s 2027 Mission to Haven-1

Arnaud Prost will be the first French astronaut on a private space station in 2027—a historic shift away from ISS dependency. 🇫🇷🚀 France bets big on commercial space, but each new module and data link is a potential cyberattack entry point. With space cyber incidents rising 30-40% yearly, is your country ready for the security risks of privatized orbit?

On June 2, 2026, President Emmanuel Macron publicly confirmed that astronaut Arnaud Prost will fly to Vast’s private Haven-1 station in 2027. The announcement, framed as a milestone in Franco-US collaboration, signals a deliberate pivot in European space policy: away from ISS dependency and toward commercial, independent platforms.

How the Deal Works

Haven-1, developed by California-based Vast, is scheduled to launch in January 2027. The station is designed as a single-module, crew-tended platform supporting up to four astronauts for short-duration missions. Under a commercial-government agreement signed between Vast and France, Prost will join the first crew, making him the first French astronaut aboard a private space station.

Macron’s office stated the mission is part of a broader Franco-US partnership. France is also contributing three astronauts—including Prost and Thomas Pesquet—to the Artemis III lunar mission, set for March 15, 2027. The dual track—low-Earth orbit and lunar—reflects a strategic bet: secure near-term commercial access while building deep-space capability.

Drivers: Policy, Competition, and Supply-Chain Risk

The decision is driven by three structural shifts:

- European space policy realignment: ESA and national agencies are moving away from sole reliance on the ISS, which begins decommissioning preparations in mid-2027. The goal is to secure independent crewed access through commercial providers.

- Strategic competition with the US and China: Both nations are accelerating lunar programs and private station development. France’s early commitment to Haven-1 positions it as a lead European partner, avoiding marginalization.

- Supply-chain and cybersecurity vulnerabilities: COVID-era disruptions and rising geopolitical tensions exposed fragility in aerospace component supply chains. The shift to private stations introduces new cybersecurity risks, as interconnected flight and station systems become targets for state and non-state actors.

Impacts: Opportunities and Risks

Cybersecurity: The proliferation of private space stations and crewed missions expands the attack surface. Each module, ground station, and data link represents a potential entry point. France and Vast will need to implement end-to-end encryption, hardened communication protocols, and continuous monitoring—costs that may reach tens of millions per mission.

Supply chains: Global aerospace supply chains face increased demand for high-reliability components—life support, propulsion, radiation shielding. French and European suppliers (Airbus Safran, Thales Alenia Space) are positioned to capture a share, but lead times for specialized parts may stretch to 18–24 months.

Commercial opportunity: European space-tech startups—in propulsion, in-orbit servicing, and data analytics—gain a clear market signal. The French government’s commitment creates anchor demand, enabling startups to raise capital and scale.

Geopolitical positioning: The Franco-US agreement strengthens France’s voice in international space governance. It also creates a template for other European nations: a direct bilateral deal with a private US provider, bypassing the slower, consensus-driven ESA framework.

Outlook and Forecasts

- 2026–2027: Prost’s mission to Haven-1 proceeds as announced. Artemis III launches on schedule. ISS decommissioning begins, accelerating the transition to private stations.

- 2028–2030: At least two additional European nations sign commercial crew agreements with US private station operators. European space-tech startups raise €1.5–2 billion in cumulative venture funding. Cybersecurity incidents in space operations rise 30–40% year-over-year.

- 2030–2035: The European space sector achieves independent crewed access via a mix of private stations and national vehicles. France emerges as the leading European space power, with 15–20% of global commercial crew missions originating from French partnerships.

Key Implications

- Aerospace & satellite manufacturing: Increased demand for crewed modules, docking systems, and life-support hardware. European primes and suppliers see 8–12% revenue growth from private station programs by 2028.

- Cybersecurity: 40% of space operators will have experienced a significant cyber incident by 2029. Investment in space-specific cybersecurity solutions will grow at 25% CAGR.

- Defense & military aviation: Dual-use technologies—autonomous docking, radiation-tolerant electronics—will transfer to military platforms. French defense contractors will integrate commercial station technologies.

- Finance & investment: Space-tech VC funding in Europe will double by 2028, with France capturing 30–35% of the total. Institutional investors will allocate 1–2% of portfolios to space assets.

The decision is not without risk. If Haven-1 encounters technical delays or cost overruns, France’s crewed access timeline slips. Cybersecurity failures could erode public and investor confidence. But for now, Macron’s bet reflects a clear calculation: the future of human spaceflight is commercial, and France intends to be at the table.

Comments ()