65 Deaths Linked to Tesla Autopilot: US Regulators Probe Data Manipulation and Safety Gaps

TL;DR

- 15% Market Share Target: JLR Shifts Defender to Hybrid in US Strategy. Will JLR's pivot to hybrid powertrains over pure EVs successfully capture 15% of the US luxury SUV market?

- 65 Deaths: Tesla Autopilot Safety Gap — NHTSA Probes and Data Manipulation in US and EU. Do Tesla's safety claims hold up against real-world telemetry and the rising number of fatal Autopilot collisions?

🚗 Defender’s Pivot: Hybrid Logic Over Pure Electric

15% target market share: JLR's bold pivot to hybrids is a massive bet on reality over hype 🚗 This is equivalent to capturing every single luxury SUV buyer in key US hubs. Infrastructure gaps kill pure EV demand. Profitability or planetary goals? US buyers — would you choose a hybrid Defender over a full EV?

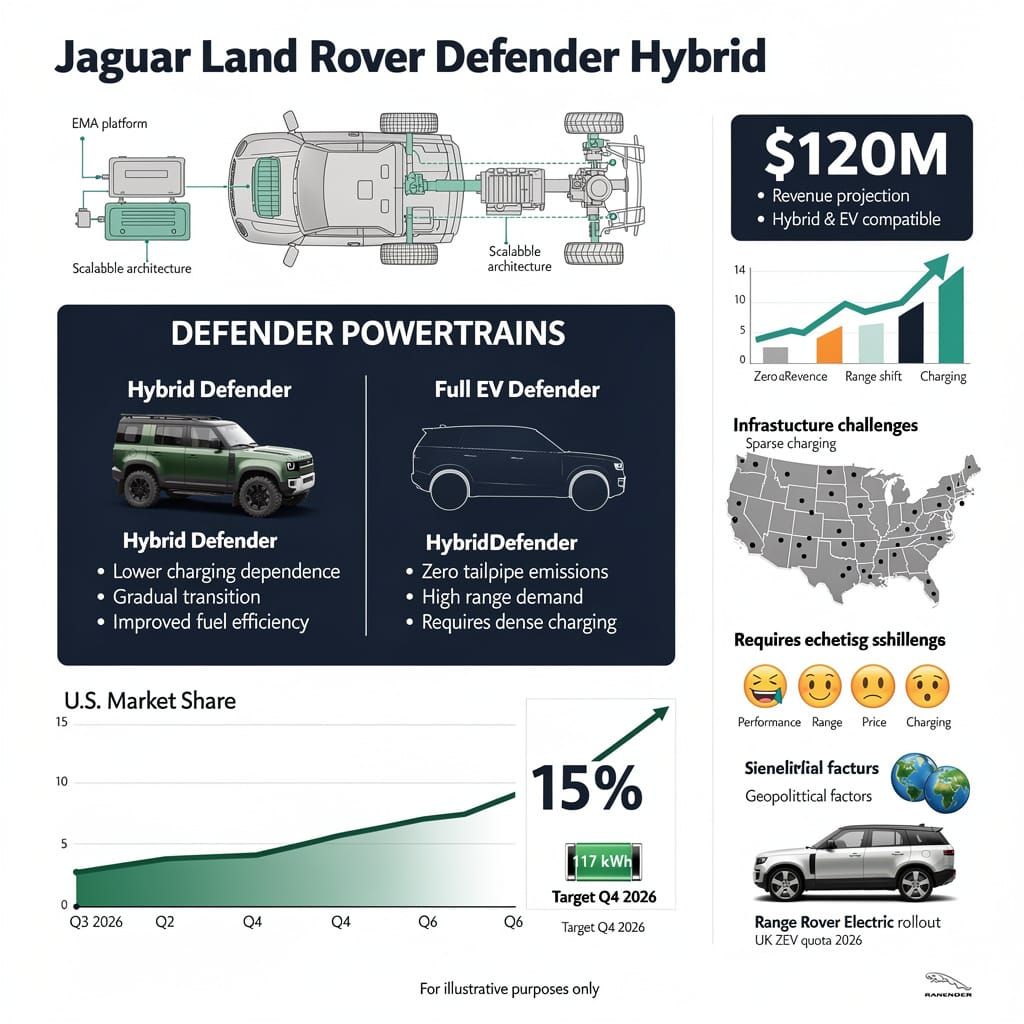

Jaguar Land Rover (JLR) announced on June 23, 2026, a strategic shift in the Defender’s development, prioritizing gas-electric hybrid powertrains over an immediate full battery-electric vehicle (BEV) launch. This decision responds to mixed market readiness and a broader industry trend where competitors, including Honda, have pivoted toward hybrids to maintain profitability amid declining pure EV demand.

How the EMA Platform Enables Flexibility?

The transition leverages the Electrified Modular Architecture (EMA) platform, which supports both Hybrid Electric Vehicle (HEV) and BEV configurations. By reconfiguring the EMA to include full hybrids without plug-in capability, JLR reduces engineering complexity while diversifying its offering. On June 17, JLR introduced the "Baby Defender," utilizing this modularity to balance off-road utility with the practical requirements of the U.S. market.

Infrastructure: Sparse charging grids and reliability concerns $\rightarrow$ heightened range anxiety $\rightarrow$ preference for hybrid reliability. Corporate Strategy: EMA modularity $\rightarrow$ simultaneous HEV/BEV support $\rightarrow$ lowered manufacturing risk vs. pure EV scaling. Market Integration: Stellantis partnership in the US $\rightarrow$ avoidance of import duties $\rightarrow$ projected $120M revenue increase from Defender exports.

What is the Projected Timeline?

- Q3 2026: Launch of the Type 01 electric gran turismo in New York (October), marking a high-end push into the luxury EV segment.

- Q4 2026: Hybrid Defender variants aim for a 15% market share in the US premium car segment.

- 2026–2027: Rollout of the Range Rover Electric (117kWh battery) and stabilization of US market share via Stellantis collaboration.

- 2028: Implementation of UK road pricing for EVs, potentially shifting consumer purchasing behavior.

Consumer Sentiment: High interest in sustainable transport (86,943 used EV sales in UK Q1) clashed with price sensitivity and charging uptime issues. Financial Pressure: Recovery efforts following a 2025 cyberattack and operational disruptions $\rightarrow$ goal of $900M+ US revenue via a revamped brand strategy. Global Context: Geopolitical volatility (Iran oil crisis) drove temporary EV surges, while regulators in the UK softened ZEV quotas from 80% to 50%, reducing the urgency for immediate full electrification.

This shift indicates that luxury automotive adoption relies on practical usability and regional infrastructure rather than raw technological capability. By integrating hybrid options, Land Rover addresses the gap in charging maturity while aggressively targeting the North American luxury SUV market through modular platforms and strategic alliances.

🚨 The Safety Gap in Autonomous Driver Assistance

65 deaths since 2013: staggering human cost of Tesla Autopilot failure. Equivalent to a lethal aviation disaster every few years 🚨. While FSD claims safety, data manipulation and pedal-pressure gaps persist. Is corporate self-certification failing us? Tesla owners — do you trust the FSD safety metrics?

Recent fatal collisions in June 2026 demonstrate a systemic failure in the interface between Tesla’s driver assistance systems and human operators. On June 23, a Tesla Model 3 operated by Michael Butler crashed through a residential home in Katy, Texas, killing 76-year-old Martha Avila. While the vehicle was utilizing Full Self-Driving (FSD), data analyzed by Tesla's Head of AI, Ashok Elluswamy, indicates a manual override occurred via full accelerator pressure, with 98.8% pedal pressure sustained through the 73 MPH impact. This event marks one of over 50 NHTSA investigations into Tesla autopilot incidents, contributing to a total of 65 deaths since 2013.

Data Integrity or Corporate Narrative?

Tesla claims its FSD is 7 times safer than human drivers, but these metrics face escalating scrutiny. An independent study reduced this safety advantage to ~3× after adjusting for methodological flaws. Further volatility emerged on June 17, when Reuters reported that Tesla manipulated safety data submitted to Dutch (RDW) and Swedish regulators, inflating projected life savings to 32,000 people without third-party verification.

Technical vulnerabilities exacerbate these risks. In China, drivers have bypassed cabin monitoring using celebrity figurines to trick liveness-detection AI, enabling unmonitored operation for up to 30 minutes. These gaps in human-machine interaction (HMI) demonstrate a correlation between system over-reliance and high-speed residential incursions.

Industry and Regulatory Impacts:

- Financial: 9.3% drop in US tech stocks on May 30 following FSD safety concerns and robotaxi launch volatility.

- Legal: Lawsuits from victims' families and heightened liability for software developers following data discrepancies.

- Regulatory: NHTSA scrutiny of ~3.2 million vehicles and intensified EU oversight demanding peer-reviewed safety data.

- Market: Waymo’s higher transparency and safety record result in a competitive disadvantage for Tesla's autonomous strategy.

Future Regulatory Trajectory

These failures enable a shift from corporate self-certification to mandatory federal validation. Regulators are now prioritizing hardware-software lockdowns to prevent spoofing and data manipulation.

- Q3 2026: NHTSA mandate for enhanced driver-monitoring systems (DMS) featuring robust liveness detection.

- 2027: Implementation of standardized federal certification for Level 3 autonomy to prevent premature mass deployment.

- 2028: Mandatory black-box telemetry for all AV-enabled fleets to resolve liability and pedal-pressure disputes.

This progression indicates that until autonomy frameworks resolve the gap between executive claims and real-world telemetry, the industry will face prolonged regulatory friction and eroded consumer trust.

Comments ()