88% Revenue Spike: Cerebras Challenges Nvidia in US AI Hardware Market

TL;DR

- 88% Revenue Surge: Cerebras Systems Disrupts AI Hardware Market with $95B Valuation. Can Cerebras sustain a $95B valuation through its OpenAI and AWS partnerships, or is the AI hardware bubble bursting?

- $4.5 Billion Series C: DayOne Data Centers Targets APAC-EU Expansion Amid Power Risks. Can DayOne's $4.5B funding overcome the rising public and regulatory backlash against AI data centers?

- 0 DNA Cuts: Epicrispr Pivots to Epigenetic Editing for FSHD in US. Can epigenetic silencing replace traditional CRISPR cutting for safer gene therapy?

🚀 The AI Hardware Pivot: Cerebras Plays the Numbers Game

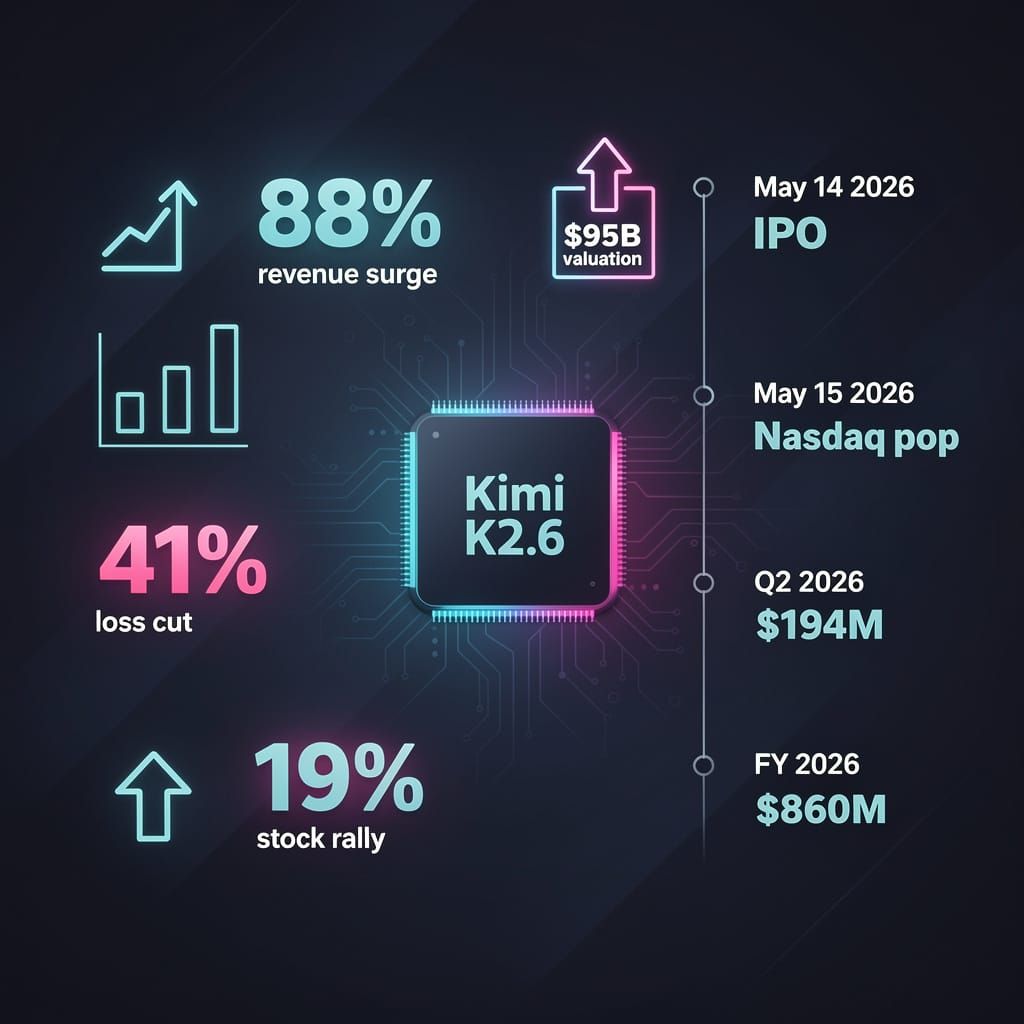

88% revenue growth! 🤯 That's like jumping from a backyard pond to an Olympic pool overnight. Cerebras just slashed losses by 41% while challenging Nvidia's throne. 🚀 Can they actually sustain a $95B valuation or is it just OpenAI hype? Tech investors—are you buying the dip or waiting for the crash?

Cerebras Systems Inc. is attempting to turn a high-burn legacy into a high-margin future. On June 30, 2026, the stock rallied 19.04% to $216.16, signaling a market recovery after a rocky debut. While a Q2 report suggests the AI gold rush is paying dividends, this spike aligns with a broader institutional rebalancing that lifted other tech players like Astera Labs and Rocket Lab.

How do you fix a burn rate?

The strategy is straightforward: replace legacy server dependencies with high-margin AI enterprise spending. The launch of the Kimi K2.6 chip—utilizing a trillions-transistor architecture—demonstrates a technical leap that enables a massive revenue surge. By securing heavyweight partnerships with OpenAI and AWS, Cerebras has shifted from a speculative startup to a disruptive challenger to Nvidia's dominance.

- May 14, 2026: IPO prices at $185 per share, marking a high-impact entry into the AI semiconductor sector.

- May 15, 2026: Nasdaq pop pushes valuation to ~$95B, fueled by $510M in 2025 revenue.

- Q2 2026: Reported $194M in revenue, marking an 88% increase.

- FY 2026 (Projected): Revenue estimated between $855M and $865M, a 69% year-over-year jump.

The Efficiency Equation

It is not just about the top line; the internal plumbing is getting cleaner. By slashing the net loss by 41% to $14M, Cerebras proves that scale can eventually tame the costs of hardware development. This tightening of the belt, combined with the high demand for low-latency inference solutions, results in a dramatic shift in investor confidence.

Revenue: $194M Q2 total → 88% growth driven by AI enterprise demand. Profitability: Net loss reduced to $14M → 41% decrease in capital leakage. Market Sentiment: Nasdaq valuation of $95B → aggressive retail and institutional repositioning.

Despite the rally, the landscape remains brutal. The sector faces supply chain disruptions and heightened cybersecurity risks as AI-optimized services expand. Furthermore, a $95B valuation draws skepticism; analysts warn that this premium depends entirely on OpenAI’s ability to convert compute into revenue. While the 28-percentage-point jump in net profit margin indicates a healthier trajectory, the company operates in a zone where one hardware misstep can erase quarterly gains. For now, the correlation between sovereign AI spending and Cerebras' bottom line is locked in, turning a volatile IPO into a high-performance asset.

💸 The Big Bill: DayOne's $4.5 Billion Power Play

$4.5B raised! 💸 That's roughly $12.3M every single day for a year. DayOne is going all-in on AI infrastructure across APAC and Europe. But with massive CapEx and public pushback on power usage, is this a gold mine or just a very expensive warehouse gamble? 🏢 Tech founders — would you risk the burn for this scale?

DayOne Data Centers Limited just threw a massive party, and the guest list included a $4.5 billion Series C round closed on June 30. Backed by heavy hitters like Coatue, Hillhouse, the Indonesia Investment Authority, and Achi Capital Partners, the cash pile is staggering. But the simultaneous appointment of Chengkang Yan as CFO indicates DayOne isn't just collecting trophies—they are bracing for the brutal cost of scaling AI-ready infrastructure across APAC and Europe.

Why the sudden CFO hire?

Injecting billions into hardware isn't like updating a SaaS subscription; it involves massive capital expenditure (CapEx) and grueling logistical chains. With DayOne already investing $7 billion in Malaysia, the timing of Yan's appointment—following a career at Hillhouse, KKR, and Citi—suggests a causal chain where rapid funding creates immediate "cash pressure." A disciplined financial hand is required to manage burn rates as the company chases hyperscale AI platforms in a volatile market.

The Growth Trajectory

- Q3 2026: Deployment of Series C capital across Singapore, Malaysia, Indonesia, Thailand, Japan, Hong Kong, Finland, and Spain.

- Q4 2026: Scaling of AI-optimized infrastructure to meet surging compute demand from hyperscalers.

- 2027: Projected peak penetration of APAC and EU markets, tracking with accelerated global IT expenditure.

Market Dynamics Financing: Shift toward hybrid models → combining sovereign funds, institutional debt, and SGD green bonds. Competition: High pressure → AirTrunk securing $1.8bn debt for Johor creates a bidding war for regional land/power. Risk: Public backlash → 71% of U.S. voters oppose AI data centers, resulting in state moratoria in Maine and New York.

Despite the funding, DayOne's success hinges on more than just cash. While CBRE forecasts record 2026 leasing activity, the "AI gold rush" is hitting a wall of public resentment. In Malaysia, the boom adds MYR 231.5bn (~11.4% of GDP) and 30,000–40,000 high-skilled jobs, but energy demand could hit 5,000MW, straining grids and clashing with net-zero goals. If DayOne cannot secure sustainable power and navigate the regulatory pushback seen in the U.S., they risk owning very expensive, very empty warehouses. For now, the $4.5 billion runway allows them to gamble on dominating the APAC digital corridor.

🧬 The Soft Touch: Epicrispr’s Pivot to Epigenetic Editing

0 permanent cuts. Epicrispr is ditching the DNA scalpel for a dimmer switch 🧬. This pivot to epigenetic silencing is like switching from a sledgehammer to a volume knob. Will non-disruptive editing finally kill the risk of mutations? FSHD patients—could this be the safer breakthrough?

Epicrispr Biotechnologies just traded the molecular scalpel for a dimmer switch. On June 26, the company installed Amber Salzman as CEO, a move that signals a sharp departure from internal growth plans. The new mandate? Stop trying to rewrite the genetic code and start managing how it is read.

Why stop cutting DNA?

Traditional CRISPR relies on double-strand breaks—permanent cuts that risk off-target mutagenesis. Epicrispr is pivoting to epigenetic editing using a dead-Cas9 (dCas9) framework. Instead of slicing DNA, this system silences or activates specific genes via chromatin regulation. This shift reduces genomic risk while targeting fetal serumless hemoglobin splicing factor defects associated with Facioscapulohumeral Muscular Dystrophy (FSHD).

This isn't a lonely gamble. The field is heating up: VERVE-102 recently achieved a 62% reduction in LDL cholesterol via permanent editing in Phase I, and the VIPR system—a bacteriophage defense—is emerging as a precursor to CRISPR that clamps onto sequences rather than cutting them. These results demonstrate that non-disruptive modulation is a viable alternative to permanent nucleotide swaps.

The Strategic Pivot

- Risk Profile: Permanent DNA cuts → Transient chromatin regulation.

- Regulatory Path: FDA’s "Operation Trial Blazer" → Potential Phase 1 timeline reductions of 6–12 months.

- Mechanism: Genomic alteration → Epigenetic silencing.

What happens next?

Under Salzman, Epicrispr launched a Phase I clinical trial on June 28. The objective is to prove that epigenetic activation improves FSHD symptoms without the unpredictable mutations of first-generation editing. Success now hinges on patient enrollment and biomarker data, arriving just as the FDA is aggressively slashing red tape to counter China's NMPA workforce expansion.

Clinical Timeline

- June 2026: Phase I trial initiation; first human application of this specific epigenetic framework for FSHD.

- 2026–2028: Safety data collection and biomarker alignment to validate transient regulation.

- Post-2028: Potential expansion into broader neuromuscular disorder therapeutics.

Operational Impacts

- Clinical: First-in-human trial for FSHD → validation of dCas9 for muscular dystrophy.

- Financial: Sector shift toward non-GCM pipelines → increased investor confidence despite broader market volatility (e.g., June 2 sell-off).

- Scientific: Shift from DNA repair → specialized epigenome editing, potentially superseding conventional editors within 3 years.

Comments ()