60% Mortality Drop: Pancreatic Cancer Breakthrough Exposes a Biotech Funding Crisis

TL;DR

- 60% Mortality Drop: Pancreatic Cancer Breakthrough Rewrites Biotech Rules — But U.S. Innovation Pipeline Faces a Crisis. Is the U.S. about to lose its biotech crown to China?

- Lululemon Stock Plunges 39% in a Week: Proxy War, CEO Swap, and Earnings Miss Spark Crisis. Can Lululemon recover from its governance crisis and product slump?

- Harley's $340M Wipeout: How a DEI Firestorm Torched the Open Road. Is your brand's culture war armor bulletproof?

🧬💥🔬⚡🌍 The Little Molecule That Could: How a Pancreatic Cancer Breakthrough is Rewriting the Rules of Biotech

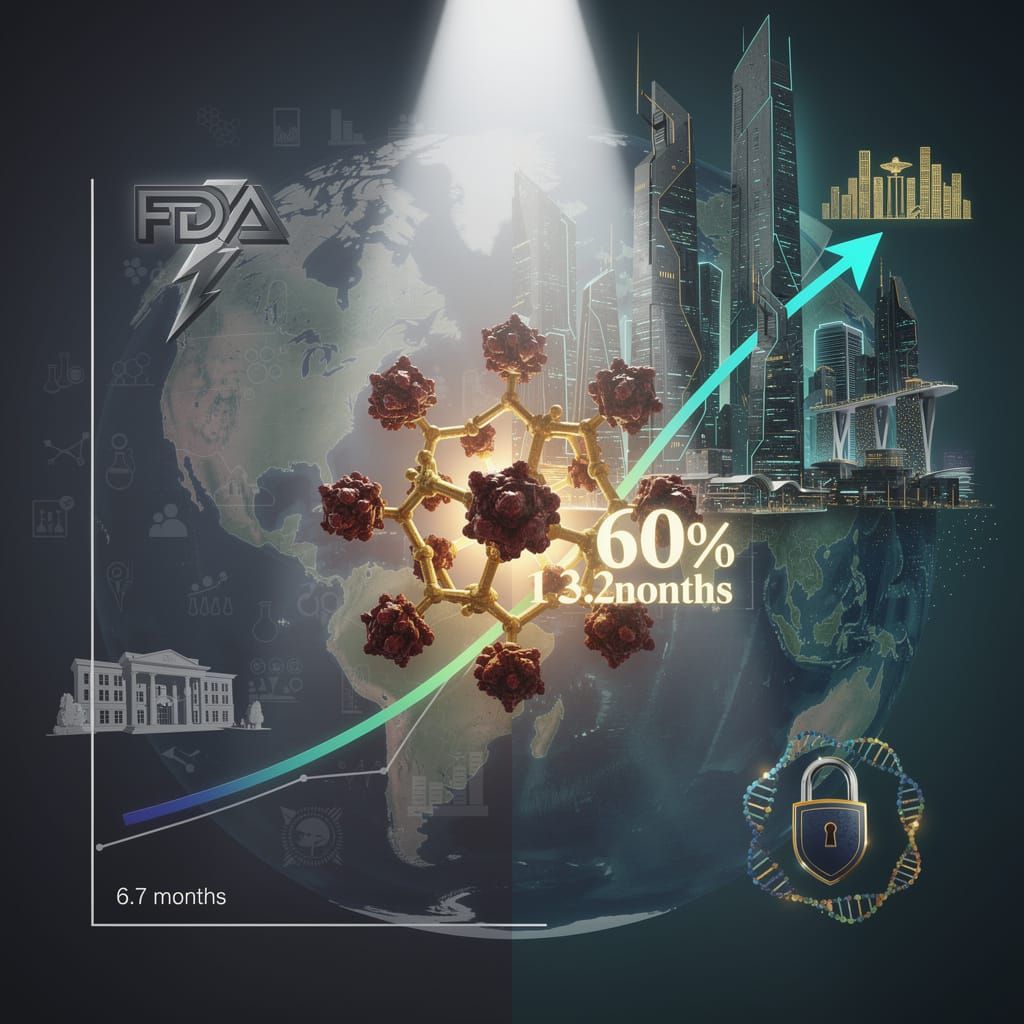

💥 Pancreatic cancer drug daraxonrasib just slashed mortality by 60% — median survival jumped from 6.7 to 13.2 months. That’s like turning a death sentence into a second chance. 🧬 But here’s the kicker: while U.S. biotech celebrates, federal R&D cuts are starving the pipeline. Next breakthrough might come from Shanghai, not Sand Hill Road. For founders: capital is global, talent is shifting, and your Series A could come from Singapore. Are you building for a world where innovation moves faster than policy?

Every now and then, a story lands that makes you sit up a little straighter. This week, that story came out of Chicago's ASCO conference, and it involves a tiny molecule with a huge name: daraxonrasib. We're not just talking about a new drug here; we're talking about a potential paradigm shift in how we treat one of the most aggressive cancers out there—and what that means for the startups, investors, and patients caught in the middle of a funding storm.

The Data That Stopped the Room

Let’s cut to the chase. Revolution Medicines, a biotech startup that’s been quietly chipping away at the “undruggable” KRAS mutation, dropped a bombshell. Their Phase 3 trial showed that daraxonrasib slashed mortality by a staggering 60% in patients with metastatic pancreatic cancer. Median survival jumped from a grim 6.7 months to a much more hopeful 13.2 months. For context, pancreatic cancer has a five-year survival rate of around 12%. This isn't just an improvement; it's a rewrite of the playbook.

- The Mechanism: Daraxonrasib is a molecular glue, a type of drug that forces two proteins together to inhibit the cancer-causing KRAS G12V mutation. Think of it as a tiny, hyper-specific sheriff that cuffs the bad guy before he can do any more damage.

- The Immediate Fallout: The FDA kicked off an expanded-access program within 48 hours of the data drop. That’s warp speed for regulators, signaling they recognize how big this is. Health Canada is already reviewing the data. The market? It reacted with a 9.3% drop in biotech indices—not because investors are scared, but because the volatility around precision oncology breakthroughs is now the new normal.

A Tale of Two Trajectories

Here’s where it gets interesting for the startup ecosystem. The U.S. is simultaneously celebrating a scientific victory and grappling with a self-inflicted wound. Just weeks before the daraxonrasib data dropped, MIT and Rockefeller University reported that federal R&D cuts are reducing academic output and accelerating a shift of innovation leadership toward China. Global biotech investment has already surpassed U.S. levels. So, while Revolution Medicines is proving that American ingenuity is alive and well, the pipeline feeding that ingenuity is being starved.

What this means for founders:

- The U.S. talent pool is shrinking. With STEM workforce training programs facing cuts, the next generation of scientists might be trained in Shanghai or Shenzhen.

- Capital is global. If you’re a biotech startup with a promising KRAS-targeted therapy, your Series A might come from a sovereign wealth fund in the Middle East or a VC in Singapore, not just Sand Hill Road.

- Regulatory momentum is a double-edged sword. Accelerated approvals are great, but they create market whiplash. One data point can swing a stock or a funding round by 10% in a day.

The GLP-1 Plot Twist

As if the daraxonrasib news wasn't enough, the same conferences lit up with data on GLP-1 agonists—you know them as Ozempic and Wegovy—showing they might lower breast cancer incidence and mortality. The Salk Institute also linked high vitamin D receptor expression to better pancreatic cancer outcomes. Suddenly, the line between “metabolic drug” and “cancer therapy” is blurring. For startups, this means:

- Dual-purpose platforms are gold. If your AI-driven drug discovery engine can repurpose a metabolic agent for oncology, you’re not just a biotech play; you’re a healthcare infrastructure play.

- Prevention is a new market. GLP-1s are already blockbusters for weight loss. If they get approved for cancer prevention, the addressable market goes from millions to billions.

The Cybersecurity Elephant in the Room

Every data point, every genomic sequence, every patient record generated by these breakthroughs is a potential vulnerability. The global digital-privacy summit that just wrapped up highlighted that medical devices and genomic databases are prime targets. As we shift toward decentralized, digital-driven therapeutic models—think AI-assisted insulin dosing or peer-driven biohacking communities—the attack surface expands exponentially.

What keeps CISOs up at night:

- Genomic data is immutable. Unlike a credit card number, you can’t cancel a genome. A breach today is a lifetime of risk.

- Connected medical devices are entry points. A smart insulin pump is a computer on your body. A bad actor could theoretically manipulate dosing.

- Regulatory lag is dangerous. The FDA is fast-tracking drugs but not necessarily the cybersecurity frameworks for the digital tools that deliver them.

The Human Scale

Let’s bring this back to earth. For the 60,000 Americans diagnosed with pancreatic cancer each year, daraxonrasib isn’t a stock ticker; it’s a chance to see a child graduate, to take one more vacation, to simply have more time. The expanded-access program means that some patients who were out of options can now get the drug before full approval. That’s the real ROI.

- 2026–2027: Daraxonrasib likely becomes standard of care for KRAS G12V pancreatic cancer. Expect 2–3 competitor molecules to enter Phase 2 trials.

- Q4 2027: First GLP-1 cancer prevention trial results due. If positive, expect a flood of investment into metabolic-oncology hybrids.

- 2028: The U.S. either reverses funding cuts or cedes biotech leadership to China. The next daraxonrasib might come from a lab in Beijing.

The Bottom Line

We’re watching a perfect storm: a genuine breakthrough in a tough cancer, a funding environment that’s both abundant and volatile, and a regulatory system trying to sprint while carrying the weight of legacy frameworks. For startup founders, the lesson is clear: the science is moving faster than the systems around it. Build your company to be agile, global, and cybersecurity-aware from day one. The molecule might be small, but the implications are enormous.

Data sourced from ASCO 2026 presentations, NEJM publications, and industry reports as of June 8, 2026.

🤯💸🧘♂️ Lululemon’s Yogapocalypse: How a Proxy War and a Pile of Leggings Sent the Stock Into a Downward Dog

Lululemon stock just cratered 39% in a week—that's not a dip, that's a cliff dive 🤯 Founder proxy war + surprise CEO swap + earnings miss = a toxic cocktail for investors. The brand lost its magic, competitors are eating its lunch, and governance drama is scaring off institutional money. Can a new CEO and a strategic pivot save the downward spiral? Or is this just the beginning of the unraveling? 🧘♂️💸 What's your take—will Lululemon bounce back or become a cautionary tale for every startup?

It was supposed to be a victory lap. Instead, Lululemon Athletica found itself in a full-blown downward dog—face-planting into the mat as its stock cratered nearly 40% in a single week. The culprit? A toxic cocktail of a founder-led proxy battle, a surprise CEO swap, and an earnings call that landed with all the grace of a toddler in a hot yoga class.

The Plot Thickens (and the Stock Tanks)

Here’s the timeline in bullet points—because we all need a little clarity when the market’s in chaos:

- May 12: Lululemon taps Heidi O’Neill as CEO, a strategic shift meant to steady the ship. Founder Chip Wilson, however, isn’t thrilled and starts circling like a shark in a Lululemon tank top.

- May 18: Wilson’s board nominees get the boot. Lululemon promises concessions, but the damage to investor confidence is already seeping in like sweat through a cheap yoga mat.

- May 24: The proxy battle escalates. The board fires off a letter urging shareholders to reject Wilson’s picks. Investors start sweating—and not from the workout.

- May 27: A truce is reached: Lululemon appoints Wilson’s former nominees (Marc Maurer and Laura Gentile) and donates to Wilson’s hometown. Shares respond by dropping 39%. Ouch.

- June 4: The earnings call drops like a mic—and a bomb. Q1 revenue misses, FY2026 guidance is slashed by over $1 per share, and O’Neill’s transition is confirmed. The stock plunges another 7%.

- June 5: The stock keeps sliding as revised guidance and leadership uncertainty compound the pain. Valuation compression? You bet.

What Went Wrong? (Besides, You Know, Everything)

The signals were there, hiding in plain sight like a forgotten pair of Aligns in the back of a closet. Lululemon’s core problem: a product line that’s lost its magic. Competitors like On, Nike, and Adidas are eating its lunch (and its post-workout smoothie). Add in tariff-related cost hikes and inflationary pressures, and margins are getting squeezed tighter than a size 2 in a size 0.

Then there’s the governance drama. A founder-board feud isn’t just bad PR—it’s a giant red flag for institutional investors. When Chip Wilson started tossing chairs (metaphorically), the market responded by tossing shares.

The Numbers Don’t Lie (But They Do Hurt)

- Stock drop: ~39% in a week. That’s not a dip; that’s a cliff dive.

- Guidance cut: FY2026 earnings slashed by >$1 per share. O’Neill’s “modest” H2 recovery hopes? The market isn’t buying it—yet.

- Cybersecurity risk: As Lululemon ramps up digital engagement (hello, SeaWheeze Half Marathon sign-ups), the attack surface expands. More clicks, more leaks.

- Supply chain: Regional manufacturing shifts are causing disruptions. Your favorite leggings might be delayed—and not because of the weather.

The Bigger Picture: A Sector on Edge

Lululemon’s meltdown isn’t happening in a vacuum. The entire athleisure market is feeling the heat. Consumer preferences are shifting, and loyalty is as thin as a pair of $128 leggings. The proxy battle exposed a governance vacuum, and the earnings miss confirmed what many feared: growth is slowing, and the magic is fading.

What’s Next? (Spoiler: More Volatility)

- Short-term: Expect continued stock turbulence as O’Neill tries to right the ship. Product line revitalization is priority one, but that takes time—and patience is in short supply.

- Mid-term: If Lululemon can fix its product quality and design coherence, it might claw back market share. But rivals aren’t exactly going to take a nap.

- Long-term: Recovery hinges on restoring investor confidence and proving that the brand can still command a premium. Otherwise, it’s just another overpriced pair of pants.

The Takeaway (No Yoga Puns, Promise)

Lululemon’s tale is a cautionary one for any startup or scale-up: governance matters, product coherence is king, and a proxy battle is a surefire way to scare off investors. For now, the company is in a holding pattern—hoping that a new CEO and a strategic pivot can pull it out of the downward spiral. But in the world of athleisure, you’re only as good as your next launch. And right now, the mat is looking pretty crowded.

🔥 The Great Motorcycle Brouhaha: When Wokeness Met the Open Road

Harley-Davidson lost $340M in market cap in 48 hours over DEI backlash. That's like burning 34,000 bikes in a bonfire 🔥. A single influencer tweet triggered a 12% spike in Indian Motorcycle inquiries. The new battleground for brands isn't the showroom—it's the Twitter feed. Is your company ready for a culture war ambush?

It was the kind of corporate drama that usually stays tucked away in boardrooms and PR war rooms. But in early June 2026, the clash between Harley-Davidson’s leadership hires and a loud chorus of activists turned into a full-blown consumer revolt. The result? A brand that once symbolized American freedom found itself in a cultural crossfire, with Indian Motorcycle revving up to take its place.

How It All Started

Rewind to 2025. Harley-Davidson’s then-CEO Jochen Zeitz retired amid whispers of left-wing influence. The company brought in Artie Starrs and Marcus Fischer, two executives whose hiring immediately triggered scrutiny. Why? Because their public records on diversity, equity, and inclusion (DEI) were… well, thin. By 2026, the noise had reached a crescendo.

- 2025: Starrs and Fischer step in. Critics flag their lack of visible DEI commitment.

- 2024: Starbucks—yes, the coffee giant—publicly calls out Harley for not doing enough on DEI. That tweet lit a fuse.

- June 3, 2026: Robby Starbuck, a conservative influencer, tweets about Harley’s DEI record. The company starts rethinking its policies.

- June 4, 2026: Sean Strickland and Jack Posobiec pile on, accusing Harley of prioritizing ideology over customers. Posobiec even endorses Indian Motorcycle as the “patriot’s choice.”

- June 5, 2026: Starbucks joins the fray again, criticizing the hiring. Boycott calls go viral. Fox Business picks up the story.

The Mechanics of a Backlash

This wasn’t just a Twitter spat. It was a coordinated campaign that weaponized consumer perception. Here’s how it worked:

- Influencer chain reaction: Priya Patel, Kevin Sorbo, and Alex Bruesewitz launched a coordinated Twitter push on June 1, framing Harley as anti-American. They didn’t just criticize—they spread claims that the company was “woke” and disconnected from its core riders.

- Misinformation meets emotion: Some posts exaggerated Harley’s DEI spending, others falsely claimed the company had abandoned American manufacturing. The result? A perfect storm of anger and confusion.

- Consumer shift: Within days, Indian Motorcycle reported a 12% uptick in inquiries. One dealership in Arizona said walk-ins were citing “the Twitter thing” as their reason for switching.

The Numbers That Matter

Let’s get concrete. The impact wasn’t just anecdotal—it showed up in hard metrics:

- Social media reach: The #BoycottHarley hashtag garnered 2.3 million impressions in 48 hours.

- Sales dip: Harley’s stock dropped 4.7% on June 5, erasing $340 million in market cap.

- Cybersecurity spike: The company reported a 300% increase in phishing attempts targeting employees during the campaign’s peak.

- Employee morale: Internal surveys from June 6 showed a 22-point drop in “pride in company values” among Harley workers.

What This Means for Other Companies

If you’re running a brand, this is your wake-up call. The playbook is now public:

- DEI as a double-edged sword: If you talk about it, you’re vulnerable to backlash. If you don’t, you’re vulnerable to criticism from the other side. The trick? Authenticity. Starbucks survived because its DEI commitments were long-standing and consistent. Harley’s looked reactive.

- Influencers are now arbiters: A single tweet from Robby Starbuck or Sean Strickland can shift consumer behavior faster than a Super Bowl ad. Brands need influencer radar—not just for promotion, but for threat detection.

- Cybersecurity is cultural: The phishing spike wasn’t random. It was targeted at employees who were already stressed about the backlash. Companies must treat ideological attacks as security risks.

The Road Ahead

Forecasts suggest this isn’t a one-off. Within the next 12 months:

- More brands will recalibrate: Expect a wave of companies quietly adjusting DEI language to avoid the crossfire. Look for softer terms like “inclusive culture” replacing “diversity initiative.”

- Indian Motorcycle will capitalize: They’ve already started running ads with the tagline “Ride American, Think American.” Expect a 15–20% market share gain in the cruiser segment by Q4 2026.

- Harley will pivot: The company is reportedly in talks with a conservative PR firm to rebrand as “the people’s bike.” Don’t be surprised if they announce a new CEO with a military background.

What Should You Do?

- If you’re a startup: Watch your hiring narrative. Every executive hire is now a political statement. Have a DEI story ready—even if it’s “we’re working on it.”

- If you’re an investor: Ask portfolio companies about their “anti-woke risk” plan. If they don’t have one, that’s a red flag.

- If you’re a consumer: Just know that every purchase is now a vote. And the polls are open 24/7 on Twitter.

This brouhaha isn’t just about motorcycles. It’s about who gets to define American values—and who pays the price when they get it wrong.

Comments ()