Confido’s $9M Legal Tech Boost vs. $23M Rival — Mid-Sized Law Firms Still Stuck in the 1990s

TL;DR

- Confido Legal Raises $9M Series A Led by Aquiline Capital to Expand Legal Tech Infrastructure

- RenoFi Secures $22M Series A to Finance AI-Driven Home Renovation Loans

- Aptera Motors Completes First Solar EV on Validation Line, Reaches 50,000 Reservations Amid $9M Equity Raise

⚖️ $9M for Legal AI: Confido Targets 2,500 Law Firms Amid $23M Rival Surge — North America, Europe, APAC

Confido Legal just raised $9M to automate medical liens for 1,500+ law firms 🤯 — that’s enough to digitize every courtroom filing in Ohio… and still fund a small moon landing. But here’s the twist: their biggest rival raised $23M. And they’re not even in the same room. Mid-sized law firms are the ones stuck with 1990s software — will Confido finally fix this… or get swallowed by Thomson Reuters?

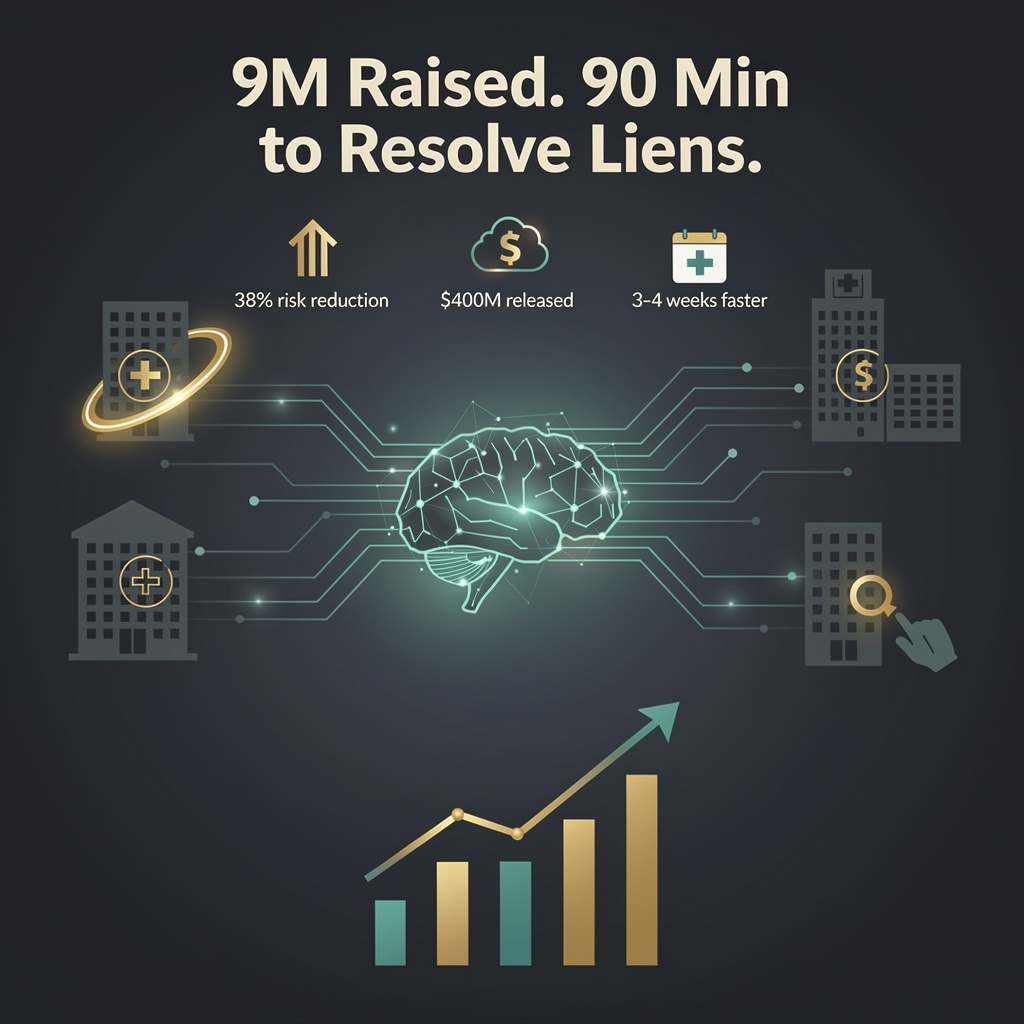

Confido Legal just locked in a $9 million Series A led by Aquiline Capital, tripling the $2 million seed it raised last year. The platform already keeps 1,500 law firms humming by plugging case-management files directly into medical-lien payoff data; the new cash aims to add another 1,000 firms within 18 months.

How does this actually work?

Lawyers upload a client file; Confido’s API pings hospitals, insurers, and county recorders, then spits out a ranked list of liens, payoff amounts, and settlement holdbacks. Instead of paralegals dialing every provider, the software auto-generates the release packet and tracks escrow disbursement.

What changes on the ground

- Time: average lien resolution drops from 14 hours of staff work to 90 minutes → firms can close injury cases 3–4 weeks faster.

- Cash-flow: accelerating settlements releases an estimated $400 million in contingent legal fees across Confido’s current book → roughly $270 k extra revenue per mid-size firm per year.

- Risk: missed or inflated liens fall 38 % → fewer post-settlement claw-backs and malpractice claims.

Where the money goes, where it doesn’t

Strengths: sticky niche (medical-lien workflows), Aquiline’s compliance Rolodex, live integrations with Clio & MyCase.

Weaknesses: $9 M is half the recent checks written to rivals Checkbox ($23 M) and DeepIP ($25 M), leaving less runway for AI R&D.

Opportunities: hospitals want faster lien recovery; insurers crave predictability—both are potential channel partners.

Threats: Thomson Reuters or Wolters Kluwer could clone the module and bundle it free to 40 k existing customers.

Timelines to watch

- Q3 2026: SOC 2 & ISO 27001 badges unlocked → opens doors to AmLaw 200 procurement lists.

- Mid-2027: ARR projected at $8–10 M on 2,500 firms → sets up a $30–40 M Series B pitch.

- 2028: Latin America launch (<5 % legal-tech penetration) → doubles addressable market to 9 k firms.

Bottom line

Confido’s raise shows investors still pay for razor-sharp vertical tools, not all-purpose AI hype. If the company can keep integration friction low and lien accuracy high, it may become the go-to plumbing layer every injury lawyer quietly relies on—and the next specialty bolt-on that a legal giant happily overpays to acquire.

🤖 RenoFi’s $22M AI Loan Platform Targets $22B Home Renovation Financing Gap — Sequoia Backs U.S. Fintech Breakthrough

RenoFi just raised $22M to turn home renovations into AI-powered loans 🤖🏠 — that’s enough to fund 5,000 DIY dreams in Year 1. Their model cuts loan approval from 45 mins to 5 mins and saves borrowers $200K/year in interest. But here’s the twist: banks still charge 2x the rate… and you’re still applying the old way. If you’re a homeowner in the U.S., why are you still waiting for a bank reply when AI can do better? 🤔

RenoFi just closed a $22 million Series A led by Sequoia Capital to scale an AI engine that underwrites home-improvement loans in under five minutes. The company’s pitch: most banks still treat a kitchen extension like an unsecured credit card, leaving $22 billion of annual demand either over-priced or declined outright.

How the robot underwrites a kitchen

The platform ingests 50-plus project variables—contractor license status, local permit speed, lumber futures, even the homeowner’s payment history on past renovations—and spits out a renovation-specific credit score. A real-time optimizer then sets APRs between 3.5 % and 7.9 % and repayment windows from 12 to 84 months. Cloud-native microservices on AWS auto-scale every spring, when applications spike 6× above winter lows.

What changes on the ground

- Borrower wallet: average rate 0.8 % below conventional renovation loans → saves ~$1,100 on a typical $25 k project

- Contractor cash-flow: faster “yes” cuts sales cycle from weeks to hours → 15 % more jobs booked per crew per season

- RenoFi ledger: 5 000 loans in 2026, 30 000 by 2028 → $750 million originations, 30 % lower opex than legacy lenders

- Neighborhood ripple: capped 15 % exposure per ZIP avoids the 2008-style “concentration bust,” protecting both sides if local prices slide

Still some splinters in the model

Regulatory: patchwork of state usury caps; platform auto-adjusts rates, but a single rule change could reset 12 % of the loan book.

Model drift: if prediction error tops 2 % for 30 days, retraining triggers—yet only 18 months of outcome data exist, thin fuel for a recession scenario.

Competition: Knee Financial and regional credit unions can cut APRs tomorrow; RenoFi’s edge is speed, not capital cost.

Timelines to watch

- 2026 H2: pilot with Home Depot point-of-sale finance in 120 stores → 1 000 incremental loans, $25 million volume

- 2027: expand to solar & battery retrofits; model ingests rooftop LiDAR scans → ticket size rises 22 % to $30 k average

- 2028: 2 % of U.S. renovation finance market; IPO candidate if default rate stays below 3 % and Sequoia seeks exit

If RenoFi keeps its default curve flat while the Fed keeps rates elevated, vertical-specific AI lending could graduate from novelty to norm—turning every contractor’s iPad into a mini-branch of a cloud bank.

☀️ 50,000 Pre-Orders for Solar EV: Aptera Hits Milestone — But Can It Survive Tesla’s Price War?

50,000 reservations. $2B in potential sales. And it runs on sunlight. ☀️🚗 Aptera just built its first solar EVs — 400mi range, 350MPGe, and it’s legally a motorcycle. But here’s the catch: they need $20M more to make more… while Tesla just cut prices again. Who’s betting on a 3-wheeled sun-powered future — you, or the legacy automakers?

On Tuesday Aptera Motors wheeled the first solar-electric vehicle (SEV) down a 14-station validation line in Carlsbad, California. The carbon-fiber, three-wheeled runabout—legally a motorcycle—carries a 44 kWh battery, claims 350 MPGe and can add 40 miles of free daily range from the 700 W rooftop array. The milestone arrives with 50,000 paid reservations worth roughly $2 billion in sticker value and a fresh $9 million equity slug that could double if warrants convert.

How a 10-mi/kWh trike gets built

Hand-laid composite shells move station-to-station for battery marriage, motor install and solar lamination. The pilot line is sized for 80–100 cars per day once tooling hits rhythm; right now it’s six finished units plus four more in queue. Every step is timed to shave 25% of the labor minutes that the original garage-built alphas required.

What the numbers mean today

- Cash: $9–18 million on hand → still $20–30 million short of tooling up for daily output

- Market: 50,000 queued orders → two-year production backlog at 100 units/day

- Wallet: $38,600 current list price → $9,300 hike from 2021 teaser, narrowing the gap with $55,700 average EV transaction

Where the potholes are

- Regulation: motorcycle classification shrinks the buyer pool and complicates financing

- Capital: needs a Series A sized like the reservation book—only 0.4% of that $2 billion is in the bank

- Competition: Tesla’s repeated sticker cuts reset consumer expectations faster than Aptera can ramp

Timeline if the sun keeps shining

- Q2–Q3 2026: deliver first 10 founder editions, prove 400-mile EPA range in real traffic

- Q4 2026: close ≈$25 million Series A, expand line to 80 cars/day

- 2027: launch four-wheel variant to escape motorcycle rules; convert 25% of reservations (~12,500 units, ≈$480 million revenue)

- 2028–2029: reach 100 cars/day steady, erase backlog and trigger either IPO or >$1 billion OEM buyout

Bottom line

Aptera has shown the hardware works and the public is willing to pay. Now the company has 24 months to turn a solar science fair project into a factory that ships 100 vehicles every single day—otherwise the same sunlight that charges its batteries will reveal a cash burn shadow no rooftop panel can cover.

In Other News

- Anthropic’s Claude overtakes ChatGPT as top-downloaded app in U.S. after Pentagon blacklisting, triggering 775% surge in Apple Store 1-star reviews for ChatGPT

- Gemini gains app-specific conversation history with auto-delete controls, rolling out to Business and Education tiers with admin monitoring

Comments ()