NSW's $6M Startup Pool: Just 0.5% of Australia's February Funding Surge — Public Seed Capital Outgunned by Private Series D Firepower

TL;DR

- NSW government commits $6M to MVP Ventures Program to accelerate early-stage tech startups

- Perplexity raises $250M at $9B valuation as AI-native search platforms dominate venture funding

- Terminus Capital Partners invests in Eventus to boost trade surveillance and global growth

⚡ $6M Public Seed vs. $194M Private Firepower: NSW's High-Stakes Bet on Early-Stage Innovation

$1M+ already deployed in Round 1—just 17% of NSW's $6M MVP Ventures pool. That's enough to fund 10 startups building everything from AI health diagnostics to low-code SaaS tools, yet barely a rounding error against Australia's $193.6M February funding surge. Stark gap between public seed capital and private Series D firepower. Will Round 2 applicants face stiffer competition from startups already courted by VCs, or does state backing give them an edge? — If you're building in Sydney, does grant credibility still open doors?

The New South Wales government has committed $6 million to its MVP Ventures Program, with the first competitive round awarding over $1 million to ten early-stage tech startups. This phased state-backed initiative targets a critical financing gap: the precarious bridge between concept and market-ready product, where many Australian startups falter before attracting private capital.

How the program operates

The $6 million allocation spans three competitive rounds through 2025–26, with up to $3 million distributed across this fiscal year. Round 1 recipients include Babylon Nexus and Walking Tall Health (AI-driven health diagnostics), BIMLOGIQ (construction data analytics), and One-Touch Business Technology Solutions (low-code integration tools). Grants follow transparent scoring criteria, with mandatory post-funding reporting on prototype completion, pilot revenue generation, and follow-on funding secured. The program explicitly ties disbursement to measurable milestones rather than open-ended support.

Immediate impacts across sectors

Capital efficiency: Direct state backing reduces early-stage burn rates, extending runway for pre-revenue firms to reach validation thresholds.

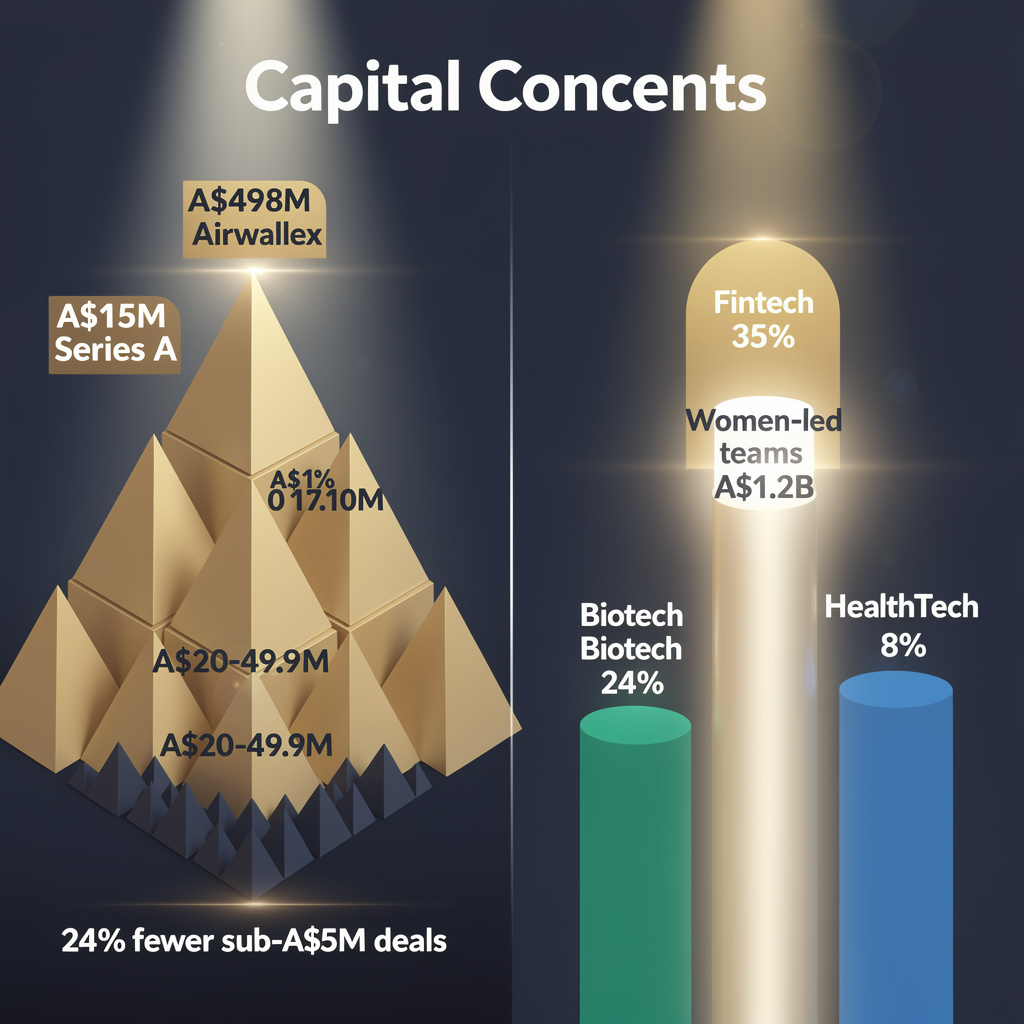

Pipeline development: Functional MVPs enable startups to access downstream private capital—critical when February 2026 data shows $193.6 million raised across ten Australian firms, including a $90 million Series D for Neara at unicorn valuation.

Sector diversification: Healthtech, construction-tech, SaaS, and consumer platforms receive simultaneous support, mitigating concentration risk in any single vertical.

Credibility signaling: Government selection acts as third-party validation, potentially reducing investor due-diligence costs and improving follow-on conversion rates by an estimated 15–20 percent based on comparable seed schemes.

Program strengths and structural limitations

| Strengths | Weaknesses |

|---|---|

| Clear funding caps ensure predictable cash flow for recipients | Small absolute pool risks allocation bias toward grant-experienced applicants |

| Diverse sector coverage reduces ecosystem vulnerability | Competitive rounds may exclude first-time founders lacking proposal expertise |

| Performance-linked disbursement enforces accountability | Limited depth may force premature scaling before market fit |

Opportunities: Leverage abundant private capital pipeline; generate NSW-based unicorn pipeline; attract foreign R&D partnerships through proven validation model.

Threats: Parallel VC programs dilute applicant quality; global credit tightening could reduce downstream funding availability regardless of MVP success.

Timeline and projected outcomes

- Q2–Q3 2026: Round 2 allocates $0.9–$1.0 million to 8–10 startups; application volume rises 30 percent following Round 1 publicity; ≥60 percent of Round 1 recipients achieve functional MVPs within six months.

- Q4 2026–Q1 2027: Round 3 completes fiscal disbursement; early KPI data informs program design adjustments; healthtech concentration increases in response to sector pipeline depth.

- 2027–2030: Cumulative program impact generates >$30 million in follow-on private investment assuming 5-fold leverage ratio; successful healthtech MVPs contribute $15–$20 million in NSW health-sector exports; neighboring states adopt competitive design, creating federated early-stage acceleration framework.

The MVP Ventures Program demonstrates how modest public capital—$6 million against billions in private markets—can reshape startup trajectories by absorbing earliest-stage risk. For NSW, this positions the state as a prototype hub where validated ideas graduate to growth-stage funding. The critical variable remains execution: whether performance metrics translate into measurable commercial outcomes, and whether political continuity sustains the three-round commitment through 2026.

🧨 Perplexity Hits $9B Valuation: AI Search's 90x Revenue Gamble

$9B valuation on <$100M ARR. Perplexity just raised $500M—SoftBank & Bezos doubling down again. That's 90x revenue multiple while burning cash like OpenAI's $14B projected loss. AI search is either the next platform layer or the biggest bubble since WeWork. Your enterprise knowledge budget—safe or getting disrupted? — What's your org still paying Google for?

Perplexity's $500 million December 2025 close—following a $250 million mid-year injection—vaults the AI-native search platform to a $9 billion valuation, underscoring how venture capital is reallocating toward interfaces that displace traditional information retrieval. SoftBank Vision Fund 2 and Jeff Bezos's repeated backing signals more than confidence in one company; it indicates a sector-wide bet that search is becoming the default layer for enterprise and consumer AI adoption.

How capital flows are restructuring search

Perplexity's fundraising arc traces the acceleration: $25.6 million Series A in 2023, $73.6 million Series B with Nvidia and Bezos in early 2024, then a tenfold valuation jump to $3 billion by mid-2024, and triple that again by year-end. This compression—roughly 350x valuation growth in 24 months—mirrors OpenAI's trajectory toward $850 billion and Anthropic's $380 billion Series G. The pattern reveals investor prioritization of full-stack platforms over isolated model providers, with SoftBank deploying across Perplexity, OpenAI, and Anthropic to capture vertical integration advantages.

What the numbers indicate

- Valuation mechanics: Perplexity's annual recurring revenue sits below $100 million, implying a 90x+ forward multiple—comparable to OpenAI's projected $12 billion revenue against its $850 billion tag. This gap demonstrates market pricing of platform potential over present monetization.

- Investor concentration: Three entities—SoftBank Vision Fund 2, Bezos-backed IVP, and Nvidia—appear across multiple cap tables, creating hardware-software convergence incentives that may limit competitive entry.

- Capital efficiency: OpenAI's projected $14 billion 2026 loss illustrates the burn-rate risks accompanying scale-first strategies.

Where the risks accumulate

Revenue validation: Sub-$100 million ARR against $9 billion valuation requires rapid enterprise API and advertising marketplace development to justify multiples.

Market concentration: Repeated co-investment by identical funds across competing platforms raises questions about price discovery and competitive dynamics.

Regulatory exposure: Platform dominance over data pipelines positions AI-native search for antitrust scrutiny as market share consolidates.

Outlook and milestones

- 2026: Expect two additional $200–300 million search-focused rounds; Nvidia-Perplexity hardware integration deals likely to tighten supply-chain dependencies.

- 2027–2028: IPO pipeline activation as ARR thresholds cross $200–300 million; Perplexity positioned for potential NYSE listing following Databricks' 2024 precedent.

- 2029–2031: AI-native search projected to capture 30%+ of enterprise knowledge-retrieval spend; valuation multiples expected to normalize toward 5x measurable revenue, compressing current forward premiums.

The $9 billion figure—roughly equivalent to the market capitalization of a mid-tier regional bank—now attaches to a company with fewer than 200 reported employees and sub-$100 million revenue. This scale of capital deployment enables compute cluster expansion and multimodal integration, yet it simultaneously compresses the timeline for revenue proof points. For founders, the imperative shifts toward monetizable product layers; for investors, cross-stack diversification becomes risk mitigation; for regulators, the emerging interface layer concentration demands attention. The capital is allocated. The revenue must follow.

📊 Terminus Capital Backs Eventus Validus: $400M Fintech Surge Meets AI Trade Surveillance

$400M+ flooded U.S. fintech in 60 days. Terminus Capital just quietly backed Eventus' Validus platform—real‑time surveillance across stocks, bonds, crypto. That's 12‑15 asset managers already locked in, with EU/APAC expansion next. Atlanta‑Austin HQ split = regulatory talent + AI engineers in one bet. The twist? While CoreWeave grabs $2B for raw compute, Eventus is building the decision layer on top. Who actually owns financial risk infrastructure in 2026—Silicon Valley builders or Wall Street incumbents? — What's your city's fintech edge?

Terminus Capital Partners has injected fresh capital into Eventus, an Atlanta-based fintech firm whose Validus platform monitors trades across equities, derivatives, and crypto assets in real time. The undisclosed investment, announced February 2026, signals intensifying investor interest in AI-driven compliance infrastructure as regulatory pressure on multi-asset trading firms reaches new heights.

How Validus captures market opportunity

Validus operates as a cloud-native surveillance engine, deploying machine-learning classifiers to flag anomalous order flow while simulating risk scenarios that integrate price shocks and counterparty exposure. Its modular architecture lets clients adjust detection thresholds without engineering support—a flexibility gap that rivals NICE Actimize and AxiomSL have not fully closed. The platform's pre- and post-trade coverage across traditional and digital assets addresses a structural market need: banks and crypto exchanges currently stitch together fragmented tools, inflating operational cost and latency.

What the investment enables

Product acceleration: Funding targets AI-enhanced anomaly detection in Validus v2.0, leveraging the same GPU-cloud expansion that drove CoreWeave's $2 billion raise in January.

Global expansion: Eventus maintains dual headquarters in Atlanta and Austin, positioning teams near financial talent pools and AI engineering hubs. The capital supports EU and APAC market entry within 12–18 months, targeting MiFID II and MAS compliance requirements.

Acquisition capacity: Terminus Capital's mandate explicitly includes strategic buys—likely data-feed aggregators or niche AI model firms valued $5–15 million that could expand Validus's data lake and revenue base by roughly 30 percent within 18 months.

Competitive positioning

- NICE Actimize: Established AML surveillance but limited multi-asset depth → Validus offers unified pre- and post-trade coverage.

- AxiomSL: Strong regulatory reporting yet primarily post-trade → Validus delivers real-time pattern recognition.

- Market timing: U.S. fintech and AI startups attracted over $400 million across January–February 2026, with cloud-security plays like Upwind Security's $250 million Series B confirming investor appetite for integrated risk platforms.

Revenue trajectory and risks

Current estimates place Eventus at $2–3 million ARR from 12–15 mid-size asset managers. Product enhancements and crypto exchange cross-sell target $5 million ARR within 24 months, with acquisition integration pushing toward $50 million ARR over three years.

| Risk | Mitigation |

|---|---|

| Regulatory shifts requiring product redesign | Flexible rule-engine with former regulator advisory input |

| AI/ML talent scarcity | Austin recruitment pipeline and accelerator partnerships |

| Competitive consolidation | Accelerated acquisition timeline and exclusive data-feed contracts |

| Post-acquisition integration complexity | API-first architecture with dedicated integration team |

Outlook

- 2026–2027: Validus v2.0 deployment; one strategic acquisition closed; three EU enterprise contracts generating $1.5 million incremental ARR.

- 2027–2028: Scale to diversified client base (banks, crypto exchanges, hedge funds); position Validus as market-standard API for surveillance data.

- 2028–2029: Potential exit via strategic sale or IPO targeting $200 million market cap.

The Terminus Capital investment captures a precise inflection point: regulatory complexity, elastic cloud compute, and AI maturity are converging to reshape trade surveillance. Eventus now holds capital and strategic backing to convert Validus from niche tool into cross-border infrastructure—provided execution matches the opportunity its investors have priced in.

In Other News

- Hudson Pacific Properties reports $572M annual loss amid office market collapse, faces $500M debt maturity

- Recursion Pharmaceuticals Reports $74.7M Revenue, Extends Cash Runway to Early 2028 After $500M+ in Partnership Payments

- Plaid Valued at $8 Billion After $575M Funding Round, Partners with Backbase to Expand Financial Data Platform

- Ireland launches 2026-2028 Circular Economy Strategy targeting 12% material reuse by 2030

Comments ()