Victoria VC Splits Same A$2.2B Across 54% More Startups: Pre-Seed Booms, Sub-$5M Deals Collapse

TL;DR

- Victoria, Australia, saw $2.2B in VC funding in 2025, with fintech and biotech leading; median Series A deal size hit $15M

- Ubicquia raises $106M Series D to expand AI-enabled infrastructure solutions globally, now serving 1,000+ cities and utilities

- IQM to Go Public via SPAC Merger, Valued at $1.8B, Targeting $320M in Quantum Funding

📈 Victoria VC: A$2.2B Deployed Across 134 Deals as Fintech-Biotech Duopoly Dominates

A$2.2B in 134 deals—same cash, 54% MORE startups funded. Victoria's VC just got way pickier 💸 Pre‑seed rounds hit A$925K (+24%), but sub‑A$5M deals crashed 24%. The bar for entry? Skyrocketing. Meanwhile women‑only teams grabbed A$1.2B (4× 2024). Is your city's early‑stage pipeline shrinking or are you just not in the room?

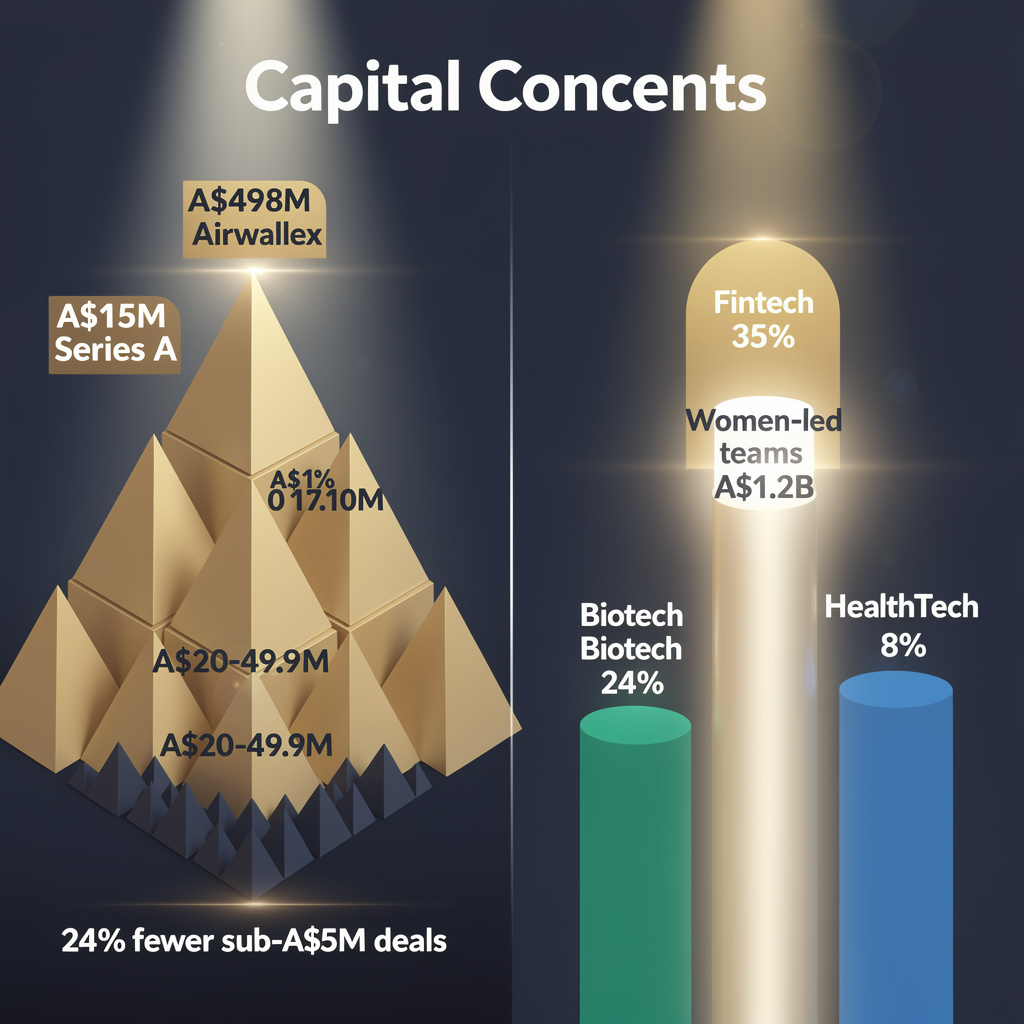

Victoria's venture-capital market delivered a striking split-screen performance in 2025: total funding held steady at A$2.2 billion across 134 deals, yet the underlying mechanics reveal a decisive tilt toward scale over volume. The median Series A round reached A$15 million—roughly double pre-2024 levels—while deals under A$5 million contracted by 24 percent. This compression indicates capital is concentrating in proven growth-stage companies rather than seeding new market entrants.

How capital reshuffled across stages

The deal-size distribution tells the story. Rounds between A$20 million and A$49.9 million jumped from 4 to 17; A$50 million-plus rounds doubled from 3 to 6. Meanwhile, pre-seed and seed medians rose to A$925,000 and A$3.2 million respectively—up 24 percent and 15 percent year-over-year. Early-stage founders secured larger initial checks, but the pipeline beneath them narrowed.

Sector concentration and its trade-offs

Victoria's capital allocation demonstrates pronounced sector clustering:

Fintech: A$759 million (35 percent of total), anchored by Airwallex's A$498 million Series G—equivalent to roughly 2,500 typical pre-seed rounds.

Biotech/MedTech: A$526 million, distributed across multiple late-stage rounds without a disclosed unicorn exit, exposing downstream financing dependencies.

Climate-tech: A$208 million, suggesting sustained but secondary investor interest.

HealthTech: A$165 million, rounding out a top-four cohort commanding 78 percent of all dollars.

This concentration enables ecosystem specialization yet risks over-dependence on two sectors facing distinct regulatory and clinical-trial timelines.

Structural shifts in founder demographics

Women-only founding teams captured A$1.2 billion across 134 deals—a fourfold increase from 2024's negligible total. This surge likely reflects accelerator-driven diversity mandates and government incentive structures rather than organic market evolution. The scale exceeds Australia's total 2023 female-founder VC allocation, indicating Victoria's outsized role in national diversity metrics.

Forward trajectory

- 2026–2027: Median Series A stabilizes at A$15–16 million; sub-A$5 million rounds recover modestly to 70–75 deals if early-stage grant schemes expand.

- 2028: Fintech potentially exceeds A$1 billion annually if AI-native platforms sustain cross-border investor appetite; biotech faces exit pressure with 2–3 anticipated IPOs or strategic sales required to validate late-stage valuations.

- Ongoing risk: Headquarters relocations—exemplified by Airwallex's Hong Kong move—threaten to decouple capital origination from long-term local economic returns.

Victoria's 2025 data validates a market rebound concentrated at the top tier. The challenge ahead lies in preventing early-stage atrophy while managing the geographic mobility of its largest success stories.

⚡ $106M Series D: Ubicquia Accelerates AI Grid Infrastructure Across 1,000+ Municipalities

$106M to wire 1,000+ cities with AI brains. That's ~18TB of monthly grid data—enough to stream Netflix for 4,000 years straight. ⚡ Ubicquia's edge gateways now decide outages in <150ms, faster than you can blink. But here's the tension: every smart meter is a hack target, and utilities still run 1980s SCADA. Midwest towns get the upgrade first—does your city make the cut?

Ubicquia's $106 million Series D, closed February 2026 and led by 67 Capital and Hamilton Lane, signals accelerating institutional conviction in AI-native infrastructure platforms. The company now serves 1,000+ municipalities and utilities across North America, Europe, and emerging markets, processing 15 million+ digital interactions annually—roughly equivalent to the entire population of Chile engaging with its systems each year.

How the platform operates

Ubicquia deploys ARM-based, 5G-enabled edge gateways running TensorRT-optimized AI inference models, feeding a central SaaS analytics layer built on Kubernetes. Core functions include predictive outage detection, demand-response optimization, automated meter reading, and real-time citizen service chatbots. The architecture targets sub-150 millisecond latency for control-loop decisions, meeting NERC CIP-005 grid stability requirements. Current telemetry generates approximately 18 terabytes of raw data monthly, with volumes projected to triple post-Series D rollout.

Operational impacts and risks

- Scale: 15 million+ annual interactions enable network effects for model training across 1,000+ client environments.

- Integration: Legacy SCADA system complexity creates deployment friction comparable to integration bottlenecks observed in high-growth chip-design firms.

- Security: Critical infrastructure exposure aligns with 2026's heightened exploit-intelligence funding environment, demanding zero-trust segmentation.

- Regulatory: Variance between EU GDPR and U.S. NERC standards requires dual-compliance engineering.

Competitive positioning and partnerships

Direct competitors include Runway (generative AI for city services), Temporal (edge execution environments), and World Labs (spatial AI modeling). Indirect pressure emerges from hardware-focused AI chip providers lowering compute costs. Mitigation strategies include threat intelligence integration with LuxnCheck, joint pilots with Utility Global for hydrogen-grid applications, and cross-selling with Temporal for AI-edge orchestration.

Deployment timeline

- 2026–2027: 200 additional cities in U.S. Midwest and EU (Germany, France); 50 new utility contracts targeting $1.2 million average ARR; edge firmware 2.0 release with on-device anomaly detection.

- 2027–2028: APAC pilot entry (South Korea, Singapore) leveraging smart-grid regulatory incentives; data pipeline scaling to ~50 TB/month requiring ~300,000 additional edge units.

- 2029: Target $500 million ARR; "smart-grid as a service" (SGaaS) expansion via utility-backed financing models.

Capital allocation reserves $20 million for edge hardware inventory and $15 million for on-device model compression R&D. Revenue CAGR projects at 45% year-over-year, driven by new contracts and AI demand-response module upsells.

Ubicquia's trajectory illustrates a broader February 2026 pattern: infrastructure-heavy, AI-native platforms attracting institutional capital at scale. Execution hinges on resolving legacy integration complexity and cybersecurity exposure through compliance-first engineering and strategic partnerships. Success positions the company as foundational infrastructure for next-generation urban and utility operations globally.

⚛️ $1.8B IQM Quantum SPAC: Europe's $450M Bet to Challenge US-China Dominance

$1.8B quantum startup IQM just locked $450M+ cash via SPAC—enough to build Europe's answer to IBM & Google. That's $320M earmarked for superconducting chips alone, while China spends $18B public on quantum. 99.9% gate fidelity, 21 systems delivered, yet Europe's still playing catch-up. Will Helsinki-NYSE dual-listing finally unlock sovereign capital to close the gap? 🇫🇮

IQM’s $1.8 billion SPAC merger with Real Asset Acquisition Corp marks Europe’s most consequential quantum-computing debut to date. The Finnish developer of superconducting quantum processors will list on the NYSE by June 2026, contingent on shareholder approval, and aims to raise $320 million to accelerate hardware development. With 21 systems delivered to 13 customers—including four of the world’s top-10 supercomputing centers—and unaudited 2025 revenue exceeding $35 million, IQM enters public markets with demonstrated technical traction and an installed base that rivals earlier-stage American competitors.

How the transaction structures capital

The deal combines $175 million from RAAQ’s trust account, $134 million in PIPE commitments, and $172 million in existing cash to yield over $450 million in post-transaction liquidity. This positions IQM to deploy $200–$250 million immediately toward scaling superconducting qubit production, with reserves earmarked for R&D, intellectual property acquisition, and quantum data-center expansion. The contemplated dual listing in Helsinki would unlock European institutional capital and reinforce EU quantum sovereignty amid a $125 billion projected global market by 2030.

Where risks and competitive pressures concentrate

- Execution: 99.9% gate fidelity, while industry-leading, must advance to 99.95%+ for practical quantum advantage; limited public revenue history heightens scrutiny of cash-burn efficiency.

- Competition: Quantinuum’s $800 million 2025 raise and Pasqal’s targeted €237 million Series round signal intensifying European rivalry; IBM, Google, and Rigetti maintain technical and ecosystem advantages.

- Financing: SPAC completion risks—regulatory delays or shareholder rejection—could defer the June 2026 timeline and compress runway.

What the funding timeline enables

- June 2026: Merger closure, NYSE listing, and optional Helsinki filing; immediate capital deployment toward next-generation processor development.

- 2026–2027: 30–40% year-over-year contract growth anticipated from supercomputing center customers and new enterprise R&D partnerships.

- 2027–2030: Targeted 100+ qubit modules with >99.95% fidelity; projected 15–20% share of global quantum hardware market contingent on sustained execution.

The merger addresses Europe’s structural funding gap against China’s ~$18 billion public quantum investment and fragmented American private markets. Success hinges on converting the $320 million development tranche into measurable technical milestones and expanded commercial adoption before trapped-ion alternatives or better-capitalized competitors consolidate market share.

In Other News

- Penn State launches $7.5M financial operating model transition with 7,500 staff trained, integrating ServiceNow portal and unified finance structure

- Xbox leadership reshuffle: Asha Sharma appointed CEO as Phil Spencer retires and Sarah Bond resigns

- Gilead Sciences to acquire Arcellx for $7.8B, advancing CAR T-cell therapy for multiple myeloma with potential $530M milestone payments

- Loblaw to Invest $2.4B in 2026 on 70 New Stores, 191 Renovations, and $1.2B Automated Distribution Center in Ontario

Comments ()