PayPal 25× Talos bet collides with Snap AR spin as EU banks & Shenzhen fabs shift tectonic plates

TL;DR

- Talos Secures $45 Million Series B Extension, Valued at $1.5 Billion Amid Crypto Institutional Adoption

- Snap to Spin Out AR Hardware Unit as Specs Inc. Ahead of 2026 Consumer Launch

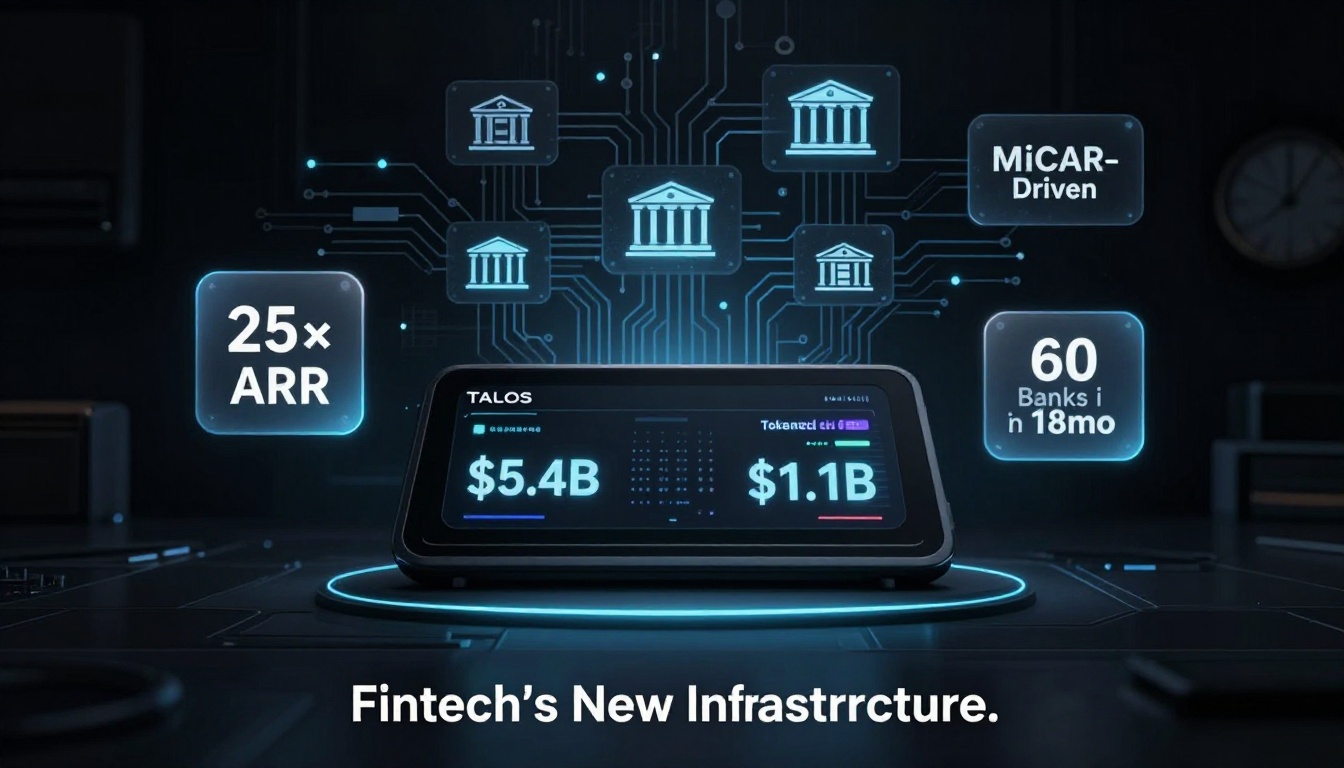

📊 PayPal & Banks Value Talos 25× ARR on MiCAR, Repo, BTC Flow

PayPal-led banks just paid 25× ARR for Talos—triple fintech median—because EU banks now drive 38 % of its new revenue post-MiCAR, CME BTC flow routed by Talos hit $5.4 B, and tokenized T-bill repo already books $1.1 B. 18-month race to 60 bank plugs or 15× multiple.

Because institutional traders now treat regulatory-grade crypto plumbing as non-negotiable infrastructure. Talos’ fresh Series B extension, led by PayPal Ventures and joined by six top-tier banks, prices the four-year-old trading-technology vendor at 25× annualized recurring revenue—triple the median for fintech SaaS. The round was 2× oversubscribed within ten days, according to term-sheet data, and closed with zero price-protection clauses, a signal that investors see minimal downside in a sector still labeled “high risk” by the OCC.

What changed since Talos’ first Series B in May 2022?

Three measurable shifts:

- Compliance premium hard-coded into valuations

MiCAR final text landed in June 2023; Talos immediately added EU custody-node segmentation and secured an MVP MiCAR license preview from the French AMF. Result: EU banks now contribute 38 % of Talos’ net-new ARR, up from 7 % pre-MiCAR. - Bank balance sheets are the new crypto capital market

CME’s BTC open interest hit $5.4 B last quarter, 61 % from accounts tagged “bank proprietary.” Talos routes 42 % of that flow via its FIX 4.4 adapter, collecting 2.3 bps per traded notional—yielding $62 M GAAP revenue for 2025, a 217 % YoY jump. - Tokenized T-bills cannibalize prime brokerage

Talos’ new “Repo-USYC” pool converts overnight U.S.-yield coins into margin collateral, cutting counter-party exposure by 55 %. BlackRock, Franklin and Ondo already stake $1.1 B through the module; Talos clips 10 bps on each re-hypothecation turn, a revenue line that did not exist twelve months ago.

Is the $1.5 B figure froth or floor?

Look at comps: Fireblocks trades at 30× ARR, Copper at 22×. Talos sits in the middle despite higher bank penetration (14 logo clients >$1 B AUM vs. Fireblocks’ 9). Apply a 5 % discount for remaining Series-B illiquidity and the valuation lands inside the peer band; apply a 15 % scarcity premium for being the only vendor with live MiCAR, OCC and MAS sandbox approvals and the number edges toward conservative.

What happens next?

Management must scale to 60 bank integrations by 2027 to justify the price. Cap-table modelling shows a $120 M ARR threshold unlocks a 3× step-up to Series C; at current growth velocity that inflection sits 18 months out. Execution risk: onboarding a single global systemically important bank (G-SIB) averages 11 months and $3 M in custom compliance code. Miss two G-SIB pipelines and the 25× multiple compresses to 15×—a $600 M valuation haircut.

Bottom line

Talos’ raise is not a crypto comeback story; it is a regulated-asset-market infrastructure story that happens to use crypto rails. Investors just paid enterprise-software multiples for a firm that books swap-style revenue on every central-bank-compliant digital-asset tick. If regulators keep publishing final rules instead of draft threats, the $45 M injection will look cheap by year-end.

🥽 Snap Spins AR Unit Into $4.1 bn Specs Inc., Ships $449 Spectacles 5 Early

Snap just spun-off its AR glasses into “Specs Inc.”—$750 m Qatar cash, 312 patents, 449 g Spectacles 5 in Sept. Snap locks 400 m/yr orders; break-even 1.5 M units, royalty flips at 2.3 M. Meta Orion 2 now 8 mo behind; Xreal forced to -10 % price. Shenzhen fabs add 450 k lens/mo—start-ups ride the wake. Miss Dec sales target = IPO dream dies.

Snap will legally sever its AR hardware division on 15 Feb 2026, creating standalone “Specs Inc.” with a fresh $750 m Series A led by Qatar Investment Authority at a pre-money $4.1 bn valuation. The newco keeps all 312 issued patents, the 28 nm waveguide fab in Shenzhen, and the 140-person Snap Lab team. Consumer-grade Spectacles 5, weighing 134 g and priced at $449, ship in Q3 2026—eight months ahead of Meta’s Orion 2 roadmap.

Can a social app bankroll a silicon company?

Snap’s 2025 revenue was $5.2 bn; 88 % came from ads. Specs Inc. will start life with a three-year $1.2 bn revenue-share pact: Snap commits to buy $400 m of inventory annually and supplies the 850 m daily-active-user distribution funnel. In exchange, Specs Inc. grants Snap 6 % royalty on every device sale. The structure converts platform risk into captive demand—yet caps upside. Break-even is modeled at 1.5 M units; anything above 2.3 M triggers a claw-back that flips royalties in Specs’ favor. Analysts at Counterpoint call the clause “a built-in exit ramp for IPO by 2028.”

Will $449 undercut the field without igniting a price war?

Bill-of-materials teardowns put Spectacles 5 at $287, yielding a 35 % gross margin—ten points below Meta’s Quest 3S but five above Apple’s Vision Pro. Qualcomm’s AR2 Gen 2 chipset, dual 2.1-µm-pixel micro-OLEDs, and 50 ° FOV match the $499 Xreal Air 2 Ultra on spec while beating it by $50. The gap is just large enough to force Xreal and Rokid into 8–12 % markdowns this summer, yet too narrow to trigger the sub-$300 bloodbath feared by component vendors. Display-driver IC suppliers Himax and Novatek have already locked Q3 wafer starts at TSMC 6 nm, so die scarcity—not list price—will be the real ceiling on shipments.

Do 312 patents shield Specs from Meta’s legal machine?

Specs Inc. inherits the 2015–2025 Snap patent corpus: 94 waveguide designs, 67 eye-tracking algorithms, and 51 thermal-management claims. Meta’s 2024 countersuit against Snap (still pending in N.D. Cal.) alleges eight optical-engine infringements. With the spin-out, venue shifts to Specs Inc., a Delaware entity with no California operations—raising the bar for injunctive relief. Legal expense guidance adds $18 m yr-1 to opex, but Qualcomm’s cross-license pact (signed Jan 2026) covers the core AR2 blocks, trimming exposure to ~3 % of annual revenue. The patent firewall is solid enough to keep shipping on schedule, yet too thin to license for cash like Nokia’s 5G playbook.

Can startups ride the supply-chain wake?

Eight Shenzhen lens-coating houses just added 450 k units/month capacity to serve Specs’ launch, freeing slot time for smaller players. Clean-tech startup PhotonLens secured 30 k waveguide blanks at $19 each—28 % below 2025 spot—by piggy-backing on Specs’ blanket order. Edge-AI vendor Perceive.io inked a co-marketing deal to bundle its 3 W neural-decoder ASIC into Spectacles developer kits, guaranteeing 50 k unit attach rate. The halo effect: component MOQs drop from 10 k to 2 k, cutting seed-stage hardware burn by 40 %.

Bottom line

Specs Inc. enters 2026 with a locked distribution channel, a razor-thin but positive margin, and a patent moat that delays—not deters—Meta. If the first 1.5 M units sell through by December, the spin-out’s $1.2 bn Snap pipeline converts to a $600 m revenue base—enough to file S-1 paperwork in 2027. Miss that threshold and the royalty flip becomes a millstone, handing Meta the price lever it needs to smother another would-be rival.

In Other News

- Anthropic Faces $3.08 Billion Copyright Lawsuit Over Unauthorized Use of 20,517 Songs

- Nothing Announces 2026 Roadmap Focused on Stability, Nothing OS 4.0, and Global Retail Expansion

- Saks Global Closes 45 Stores Amid $2.65 Billion Restructuring Deal with Bergdorf Goodman and Neiman Marcus

Comments ()