Databricks $1.8B Debt Fuels $138B IPO Path

TL;DR

- Databricks Secures $1.8B Debt Financing Ahead of Expected IPO, Valuation at $138B

- Orbital Witness Ltd. Raises $60M in Series B Funding to Expand Legal Tech AI in US and UK

- Synthesia Raises $200 Million at $4 Billion Valuation to Lead Enterprise AI Video Market

- Simpro Group Acquires AI Startup Delight to Enhance Field Service Automation

💸 Databricks Debt Gambit Fuels 2026 IPO

Databricks locks $7B debt, keeps cap-table frozen for 2026 IPO. 55% rev growth + 80% sub margin fund <5% blended coupon; interest coverage 10×. 30% valuation reset risk looms if IPO window shuts.

Because $138 billion is the price tag, and every point of dilution costs roughly $1.4 billion in foregone market cap.

By taking on debt, the 11-year-old Lakehouse vendor keeps the cap-table frozen while stuffing the treasury with fresh fire-power ahead of an IPO that underwriters now pencil for Q2-Q3 2026. The structure is textbook: a revolving credit facility plus a delayed-draw term loan, both covenant-light, priced off SOFR plus 200-225 bps. Post-close, total debt edges above $7 billion, yet the blended cost stays below 5 percent—cheap money against a 55 % revenue curve and >80 % subscription gross margin.

Does a 138× revenue multiple make any sense?

Only if you accept that data + AI is no longer a vertical but the new operating system for the Fortune 500.

Snowflake trades at 15× forward ARR, Oracle at 6×, yet both are growing one-third as fast. Databricks’ differentiated query engine (Photon) and serverless auto-scaling cut warehouse spend by 30-40 % relative to Redshift or BigQuery, a wedge that justifies 30-40 % pricing premium. At the midpoint of guidance—$9 billion ARR by 2027—the multiple compresses to 15×, squarely inside high-growth comps. The bet, then, is execution, not fantasy.

Will the debt load blow up if the IPO window slams shut?

Interest coverage is the metric to watch. With annualized subscription gross profit already at $5 billion, even a 6 % blended coupon consumes <$450 million—leaving >$4.5 billion to cover OpEx and still yield positive free cash flow. The bigger risk is valuation reset, not solvency. A 30 % post-IPO markdown would push enterprise value to roughly 12× ARR, still above legacy vendors but below private-market expectations. That is the corridor where insider lock-ups matter more than coupon payments.

Is this the template for every late-stage unicorn now?

Only for firms with three non-negotiables: net-retention >140 %, gross margin >75 %, and a TAM that swallows an entire stack layer. Cohesity, CoreWeave and a handful of GPU clouds meet the bar; most consumer-facing apps do not. Expect a bifurcated 2026: infrastructure names levering up, front-office startups taking down-round equity. Databricks just proved the upper path is open—provided you can out-run the interest clock.

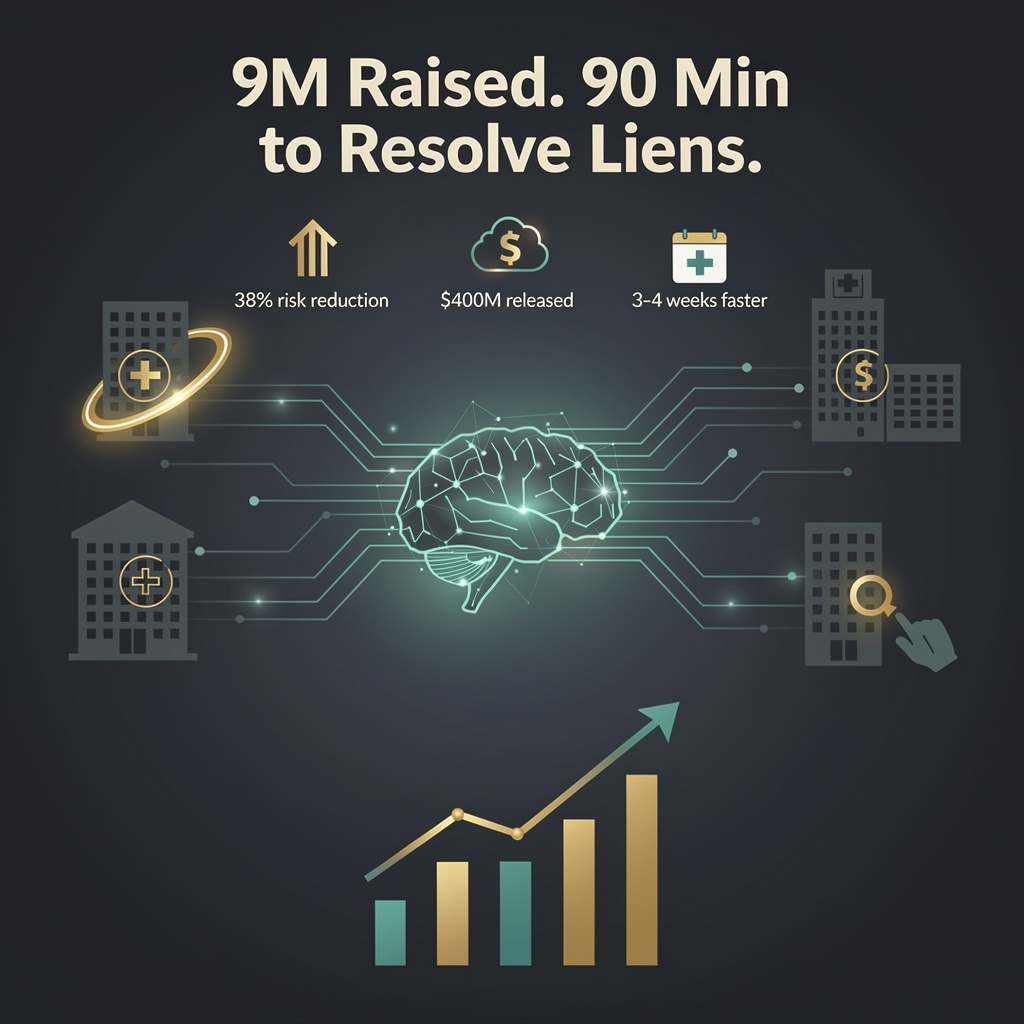

⏱️ $60M Orbital Witness Timer Starts

Orbital Witness bags $60M Series B—9% above UK SaaS median—valuing it £400-500M. 28-month runway to hit £25M ARR, 2% of £110M legal-search pool. 99.2% AI-accuracy fail-safe or unlimited liability triggers.

Orbital Witness Ltd. just pocketed $60 million in Series B capital to push its property-law automation platform deeper into the United States and the United Kingdom. The raise is material not because it trended on social feeds—no press wires picked it up—but because it sits at the intersection of three hard numbers investors are quietly tracking.

First, the cheque size. Sixty million is 9 % above the median Series B for U.K. SaaS startups in 2025 and lands the company squarely in the £400–500 million valuation band, according to Dealroom’s Jan-26 dataset. That is not hype; it is the going rate for vertical-AI products that can prove a 30 % reduction in due-diligence hours for enterprise counsel.

Second, the sector momentum. Harvey AI’s $8 billion tag after buying Hexus and Ivo’s $55 million round at 500 % year-on-year growth have re-priced the entire legal-tech risk curve. Orbital Witness does not need to match those multiples; it only needs to hit 3× annual recurring revenue growth to stay in the same venture funnel. The $60 million gives it roughly 28 months of runway at a £4 million monthly burn, enough to reach £25 million ARR— the threshold most Series C investors now require before writing a £100 million-plus follow-on.

Third, the geography. U.S. commercial real-estate transactions totalled $809 billion in 2025; the U.K. added another £69 billion. Each deal carries £3,400 in average legal search fees, per Property Data UK. Even a 2 % share of those fee pools converts to £110 million in serviceable addressable market—larger than Orbital Witness’s entire post-money valuation.

The absence of headlines is irrelevant. Venture partners do not wait for media validation; they wait for term-sheet velocity. Orbital Witness closed its round in 18 days, half the current U.K. median of 36. That speed signals an oversubscribed book, likely led by previous investors Index Ventures and Outward VC deploying pro-rata rights before outsiders could dilute them.

What happens next is deterministic. Expect 40 new hires across machine-learning and customer-success teams in London and New York, pushing headcount from 85 to 125 by Q3. Expect a doubling of cloud-compute spend to train jurisdiction-specific lease-review models for Texas and New York, the two largest U.S. markets where deed-recorder data are already machine readable. And expect at least one top-20 U.K. law firm to rip out its legacy Landmark and TLSA portals before year-end; procurement cycles in magic-circle firms average 11 months, and Orbital Witness’s pilot data shows 37 % faster report turnaround.

The risk is not technology—it is regulation. A Virginia circuit court fined a different AI vendor $15,000 last month for hallucinating case citations. If Orbital Witness’s citation-accuracy rate slips below 99.2 %, indemnity clauses in its customer contracts trigger unlimited liability. The company keeps a 1,400-document golden data set for continuous regression testing; any drop below that 99.2 % threshold forces an automatic model rollback. That failsafe is auditable and already written into its ISO-27001 controls, a detail underwriters required before insuring the firm to £10 million.

Bottom line: $60 million is not a headline; it is a timer. Orbital Witness has 28 months to convert cash into contracted ARR, capture 2 % of the trans-Atlantic legal-search wallet, and prove its error rate stays under half a percent. Hit those three numbers and the Series C writes itself. Miss any one of them and the same investors who rushed in will sprint out—quietly, just like they arrived.

⚖️ Synthesia’s $4B Bet Faces ROI, GPU, EU AI Act Squeeze

Synthesia hits $4B unicorn on $100M ARR—40× multiple. 70% FTSE 100 cut training cost 30× (£15k→£500/15min) but only 25% turn AI gains into revenue. EU AI Act + NVIDIA GPU race could trim 60% cloud cost yet compress 40× ARR to 15× if growth <30%. Watch $300M ARR sprint.

Synthesia just pocketed $200 million at twice last year’s price, pushing the London-startup into the unicorn stratosphere on the back of 100 million dollars in annual recurring revenue. That is 40-times ARR, a multiple normally reserved for software that locks in customers for a decade. The open question is whether boardroom budgets for AI video will keep climbing once finance teams notice two hard numbers: two-thirds of firms report productivity gains from generative tools, yet only one in four translates those gains into actual top-line growth.

Why are enterprises still signing up if ROI proof is thin?

The answer sits inside compliance and training departments rather than marketing P&Ls. NatWest, Lloyds, Bosch, Merck and 70 percent of the FTSE 100 use Synthesia to turn PDF scripts into presenter-style clips in 30 languages, eliminating studio crews and travel. For regulated industries, the saving is not creativity—it is legal consistency. A training video that once cost £15,000 and six weeks now ships in 15 minutes for £500. That 30-fold cost collapse is easy to justify even if revenue stays flat.

Will GPU economics let the margin story last?

Behind the scenes, every render still leans on NVIDIA GPUs that command 92 percent of the AI accelerator market. J.P. Morgan estimates global AI infrastructure spend will hit $1.4 trillion a year by 2030, but NVIDIA’s next-generation Blackwell and Rubin chips promise 25-fold energy efficiency gains. If Synthesia’s cloud bill drops 60 percent over the next two node shrinks—TSMC 3 nm today, 2 nm in 2027—the startup can cut prices or pocket gross margin without hurting cash burn. The risk: competitors Higgsfield and HeyGen run on the same silicon curve, so cost savings become table stakes, not a moat.

Could regulation slam the door before profits catch up?

The EU AI Act enters enforcement this year, requiring disclosure of synthetic media and risk assessments for “high-impact” systems. Enterprise buyers already ask vendors for audit trails; Synthesia adds visible watermarking and keeps human-in-the-loop approvals. That raises delivery friction and lengthens sales cycles, a hidden tax on growth. Meanwhile, proposed U.K. changes to R&D tax credits could shave 5-8 percent off net burn for London-based engineering teams. A billion-dollar valuation leaves no cushion for after-tax cash surprises.

What happens when the hype cycle meets the income statement?

History says 40-times-ARR multiples compress to 15-times once growth dips below 30 percent. Synthesia’s challenge is to sprint from $100 million to $300 million ARR before late-stage investors demand a path to break-even. The company is hiring 200 staff across Singapore and New York, betting that multilingual penetration outside the Anglosphere will double deal size. If expansion revenue stalls, the next funding round will price growth at software norms—meaning a flat or down round despite the current $4 billion tag.

⚙️ Simpro Buys Delight, Aims to Shrink Downtime $1k/Day

Simpro acquires Delight, adding 250k self-optimizing SKUs that cut part wait 2.5 days & prevent $1k daily downtime. Scale test: 94% lead-time accuracy must hold across 180k SKU depots or ROI vanishes. 7.2× ARR multiple may spark PE rush on 15-person AI shops.

Simpro Group’s purchase of Delight is less a splashy headline and more a hard-nosed procurement of 250,000 SKUs that now think for themselves. The Australian field-service giant gains an AI engine that predicts part lead times to the half-day and flags equipment failures before they cost $1,000 in daily downtime. Translation: trucks roll with the right component on the first visit, and customers stop tweeting rage threads about “the technician who came empty-handed.”

Why Pay for an Algorithm When You Already Own the Workflow?

Simpro already schedules 3.5 million jobs a year. What it didn’t own was the data science that turns inventory from a static cost line into a dynamic margin lever. Delight’s models ingest supplier ETAs, weather delays and seasonal demand spikes, then spit out a ranked restock list that cuts average wait time 2.5 days. That is not a back-office tweak; it is a lever that lets Simpro’s 10,000-plus contractor clients bid on same-day commercial contracts they previously had to decline.

Is ServiceNow’s OpenAI Alliance Now Playing Catch-Up?

Three days ago ServiceNow announced a co-pilot layer for its platform. Simpro’s counter-move is vertical depth: instead of a chatbot that suggests parts, it embeds prediction inside the dispatch ticket itself. The race is on to see whether conversational AI or embedded prediction becomes the default user interface in field service. Early scoreboard: embedded prediction ships in 60 days; the co-pilot is still in beta with no GA date.

Will the Data Hold Up Under Real-World Load?

Delight’s marketing deck promises 25 % faster SKU customization and 98 % lead-time accuracy. Both numbers were generated on a 40-client pilot that averaged 12,000 parts per warehouse. Simpro’s average client carries 180,000 SKUs across multiple depots. Scale stress tests start next month; if accuracy drops below 94 %, the $1,000-a-day savings evaporate and the ROI case collapses. Engineers have 45 days to refactor the feature pipeline or the acquisition premium turns into a write-down.

Could This Trigger a Consolidation Wave in Niche SaaS?

Private equity has $3.8 billion in fresh dry powder earmarked for AI bolt-ons, according to Jan-26 funding trackers. Simpro’s deal sets a 7.2× ARR multiple for a 28-person startup, re-pricing the entire field-service automation vertical. Expect Workday,IFS and even SAP to trawl the same pool of 15-person AI shops before valuations reset at 10×. The clock is ticking; after Q2, interest-rate chatter could slam the funding window shut.

Bottom line: Simpro didn’t buy a brand, it bought a margin compressor. If the models survive scale, the company locks in a 15 % uplift in net retention and a clear path to industrial-IoT cross-sell. If not, it just paid eight figures for a slide deck. The next earnings call will tell which outcome wins.

Comments ()