Float Financial Raises $100M CAD, Trump Launches Newborn Accounts, Qiagen Targets $2B Sales

TL;DR

- Float Financial Secures $100M CAD Debt to Expand Credit Products for Canadian SMEs

- Trump Administration Launches 'Trump Accounts' Program with $1,000 Initial Deposit for Newborns, Cap at $5,000 Annual Contributions

- Qiagen Raises 2028 Sales Target to $2B Across Five Growth Pillars, Revises EPS Forecast to $2.38 CER Amid Potential $13B Buyout Interest

📈 Float Financial’s $100M Debt Move and the Future of Canadian SME Lending

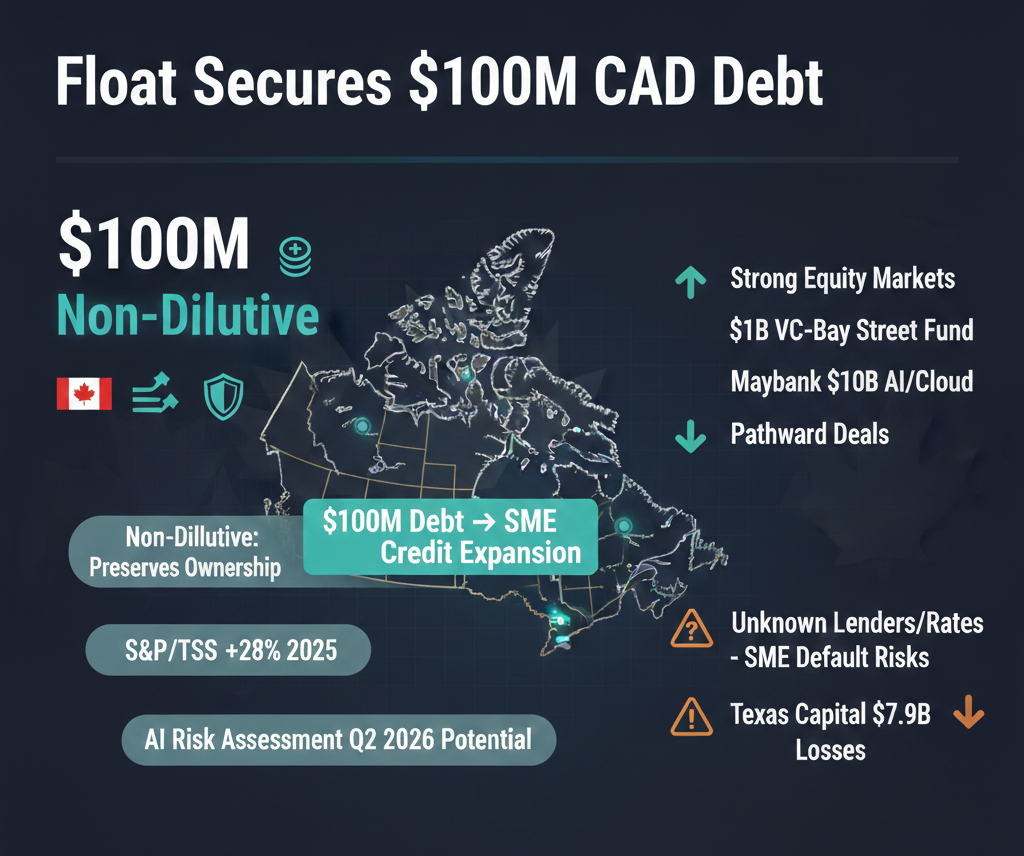

Float Financial raises $100M CAD in debt to scale SME credit products. In a strong S&P/TSX market (+28% in 2025), the move highlights a shift toward non-dilutive financing and tech-driven lending expansion in Canada.

Float Financial secured $100M CAD in debt financing on January 26, 2026, to expand credit offerings for Canadian small and medium-sized enterprises (SMEs). Unlike equity rounds, this non-dilutive capital increases lending capacity without issuing new shares, aligning with risk-averse strategies amid market volatility.

How Strong Equity Markets Are Fueling Fintech Growth

The S&P/TSX rose 28% in 2025—outpacing the S&P 500’s 16%—reflecting strong domestic economic momentum. This environment supports capital deployment, as seen in a newly announced $1B fund to connect Canadian VCs with Bay Street institutions, enhancing fintech scalability.

What Sets Float’s Strategy Apart From Global Peers?

While global fintechs like Juspay rely on equity (e.g., $50M raise), Float’s debt model preserves ownership and reduces investor dilution. This contrasts with equity-heavy trends highlighted in recent earnings, such as SLM Corp’s $1.12 EPS beat, and signals a shift toward capital efficiency.

Where Could Float’s Expansion Lead Technologically?

Maybank’s $10B AI and cloud investment (Jan 22, 2026) and Pathward’s merchant acquiring deals point to automation in credit workflows. Float may integrate AI-driven risk assessment tools by Q2 2026 to improve underwriting speed and accuracy.

What Risks and Gaps Remain Unresolved?

Key unknowns include the identity of lenders, interest rates, and covenants tied to the $100M debt. Canadian SME default rates, regional demand disparities, and regulatory responses to rising non-bank lending are unverified. Texas Capital’s $7.9B in credit loss provisions suggest tightening conditions that could affect SME borrowers.

What’s Next for Canada’s Fintech Ecosystem?

Interactive Brokers’ entry into Canada intensifies competition in digital finance. With Bay Street professional investor numbers declining, fintechs like Float are positioned to fill structural gaps. Continued monitoring of SME credit performance and VC fund deployment will determine long-term impact.

💰 How 'Trump Accounts' Could Reshape Startup Capital by 2045

Trump’s $1,000 newborn accounts may seed the next generation of founders—but funding clashes, legal risks, and childcare gaps threaten impact. Long-term startup capital could shift if accounts survive fiscal and judicial challenges.

The Trump Administration’s launch of 'Trump Accounts'—offering $1,000 at birth and up to $5,000 annually into tax-advantaged savings for children born 2025–2028—introduces a structural shift in early-life capital access. This program targets long-term wealth accumulation, directly influencing future entrepreneurship and venture capital pipelines.

Initial deposits are fully funded by tariff revenues, currently totaling $235 billion since January 2025, though a pending Supreme Court ruling on tariff legality threatens funding continuity. A 10% credit card interest rate cap, intended to finance the program, faces opposition from major financial institutions, including JPMorgan and Citigroup.

Philanthropic commitments—$6.25 billion from the Dells and $75 million from Ray Dalio—are supplemental, not primary, funding sources. These contributions support enrollment drives but do not offset the program’s estimated $300 billion fiscal footprint.

The program coincides with broader fiscal initiatives: $600 billion in corporate dividends, $2,000 rebate checks, and $1,776 military bonuses. This creates direct competition for limited revenue streams, increasing budgetary pressure.

For startups, the long-term effect could be significant. Accounts may mature into seed capital for young founders by 2043–2045, potentially increasing founder diversity and reducing reliance on angel investors or accelerators for initial funding. However, current childcare access gaps—6 million children under 5 lack care—limit immediate family stability, undermining the program’s foundational goal.

States like Hawaiʻi and Kansas are implementing complementary policies, including preschool subsidies and zoning reforms, to improve access. Without parallel investments in early childhood infrastructure, financial incentives alone may fail to stabilize fertility (1.6 in 2024) or broaden economic opportunity.

📊 Qiagen’s $2B 2028 Target Stands Amid Stalled $13B Buyout Speculation

Qiagen holds $2B 2028 sales target and $2.38 EPS forecast. No new buyout updates as of Jan-26-2026. Growth hinges on 15% CAGR and margin expansion. Liquid biopsy and NGS are key. $13B bid remains unverified. Execution risks loom.

Qiagen N.V. maintains its $2.0 billion 2028 sales target and $2.38 CER EPS forecast, unchanged since its Jan-24-2026 guidance. No updates emerged between Jan-19 and Jan-26, 2026, despite persistent speculation of a $13 billion buyout.

The growth plan rests on five pillars: molecular diagnostics, bioinformatics, liquid biopsy, companion diagnostics, and next-generation sequencing (NGS). Revenue must grow at a 15% CAGR from a $1.4B 2025 baseline to meet the 2028 target.

EPS improvement hinges on EBITDA margin expansion to 28% by 2028. Liquid biopsy, growing at a projected 20% CAGR in oncology testing, and NGS adoption at 15% CAGR, are central to the forecast.

The $13 billion buyout figure implies a ~35% premium over an estimated $9.5 billion market cap. No bidders have been confirmed, and no regulatory filings support the valuation. Potential acquirers like Thermo Fisher or Illumina remain unverified.

Execution risk remains high. R&D delays, pricing pressure in diagnostics, or antitrust scrutiny in sequencing markets could derail both organic growth and acquisition prospects.

With no new data in the past week, investors should focus on quarterly revenue trends, margin performance, and any formal M&A disclosures. The absence of movement increases scrutiny on Qiagen’s ability to deliver independently.

In Other News

- FCMB-TLG Private Debt Fund Series 2 Opens in Nigeria with N20 Billion Target for Agriculture, Clean Energy, and Tech Sectors

Comments ()