Latin America Attracts $2.85B VC in 2024 as Global Capital Surges to $5.1B, U.S. Tech Boosts $600M Series Funding

TL;DR

- Venture capital for startups surged, with Latin America reaching $2.85 billion in 2024 and global capital raised hitting $5.1 billion in October, underscoring robust funding momentum.

- Series funding across U.S. tech startups now exceeds $600 million, from AI platforms to low-carbon ventures, highlighting a vigorous venture capital ecosystem.

- Canada’s SR&ED tax incentives expansion, UK’s fiscal credits, and U.S. stimulus create a supportive regulatory climate that propels early-stage company growth.

- US startups lead global growth, yet Latin American firms are accelerating with $2.85 billion VC, as trade policies steer capital flows and market dynamics.

Venture Capital Flow Shifts: Why 2025 Is a Pivot Point for Global Startups

Record-Breaking October and the U.S. Lead

- October 2025 saw $5.1 billion of fresh capital in deals exceeding $500 million, contributing to a $39 billion total deployment for the month.

- U.S. investors accounted for roughly 60% of global funding in September 2025, anchoring the worldwide market.

- New York surged with $5.9 billion in October—up 200% YoY—while California raised $8.5 billion, together representing over 35% of all October capital.

Latin America’s Accelerating Momentum

- VC inflow to Latin America grew 26% YoY in 2024, reaching $2.85 billion and lifting the region’s share of global VC to about 7%.

- The continent now hosts 32 unicorns with a combined valuation of $71.8 billion, surpassing Europe’s per-capita unicorn density.

- Credit-card penetration rose to 6.6 million users, expanding financing capacity for fintech and SaaS startups.

Asia-Pacific Gains and Sector Focus

- China’s October VC inflow jumped to $3.9 billion (+200% YoY) and India’s rose to $1.5 billion (+80% YoY), narrowing the gap with U.S. funding.

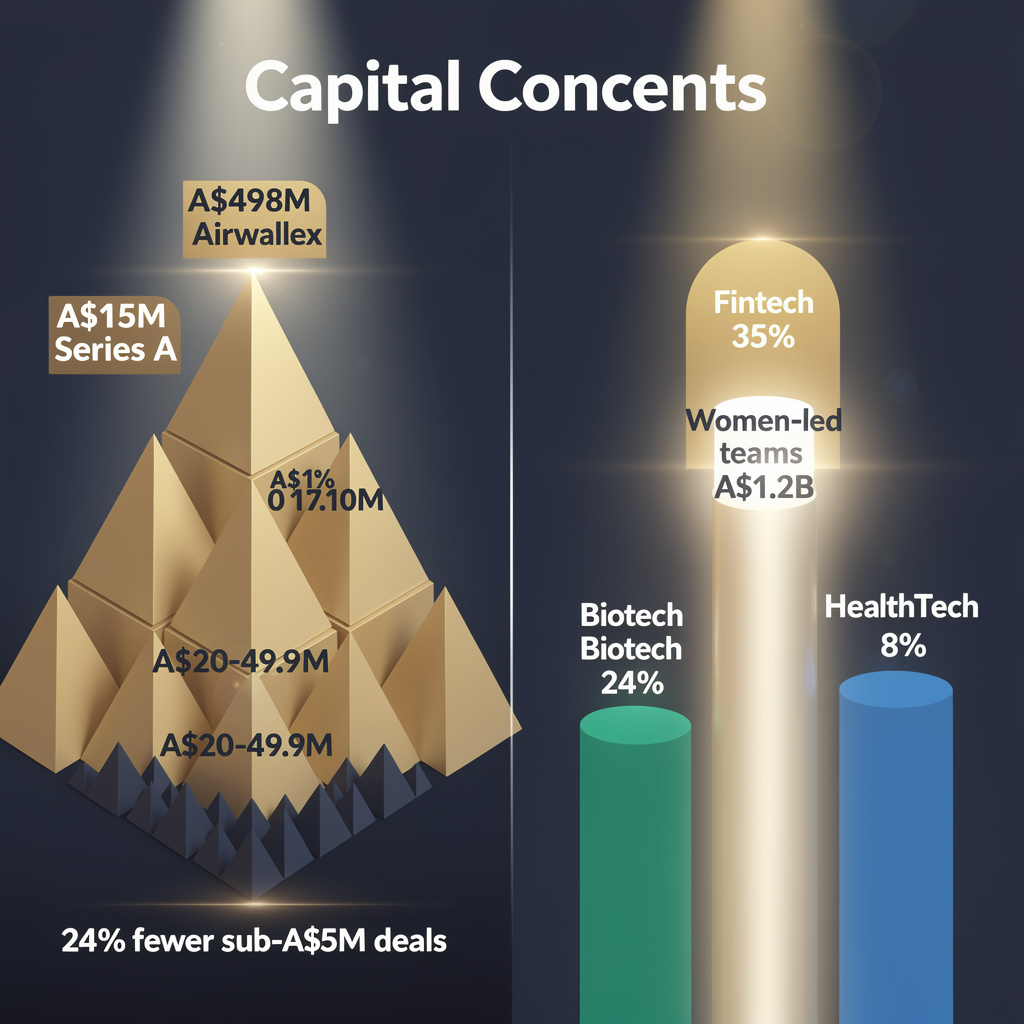

- Mid-size rounds ($500 million+) dominated the month, while mega-rounds such as Crusoe Energy’s $1.4 billion and Oura’s $900 million underscored capital appetite for capital-intensive verticals.

- Innovation, space, and banking/finance sectors captured the bulk of new money, signaling a bias toward high-growth, infrastructure-heavy businesses.

Looking Ahead: 2026–2027 Forecasts

- Global VC is projected to grow 12% in 2026, driven by sustained mid-size round frequency and continued U.S. dominance.

- Latin America could claim roughly 9% of global VC by 2026, leveraging its unicorn pipeline and expanding consumer credit market.

- The European late-stage financing gap is expected to close by Q2 2027 as policy incentives and pension-fund allocations target an additional $300 billion of capital.

- Four to five mega-rounds (>$1 billion) are likely each year in 2026, reflecting steady liquidity from U.S. and Asian investors.

Strategic Takeaways for Investors, Founders, and Policymakers

- Investors: Double-down on New York and California pipelines for immediate scale; earmark dedicated LatAm funds to capture the region’s rising share.

- Founders: Pursue mid-size rounds above $500 million and showcase traction in AI, space, or fintech to align with capital trends.

- Policymakers (EU): Accelerate VC-friendly reforms and direct pension assets toward late-stage ventures to meet the 2027 funding target.

U.S. Series Funding Landscape: An AI-First, Low-Carbon Surge

Funding Activity – October 2025

- Total U.S. series capital (all sectors): $600 million+ for the month.

- Global venture investment: $39 billion (up from $34 billion in September).

- U.S. share of global VC: ~60%.

- Top-tier rounds (≥$5 million): 9 companies, totaling ~$12 billion, ~30% of U.S. series capital.

- Largest single rounds: Crusoe Energy $1.4 billion, Base Power $1 billion, Oura $0.9 billion, Redwood $0.35 billion.

Sector Allocation

- AI platforms / data automation: IgniteData Series A $11 million, Parable seed $16.5 million, Beacon Series B $250 million, Rilevera seed $3 million – cumulative ≈$280 million.

- Low-carbon energy & materials: Crusoe Energy $1.4 billion, Base Power $1 billion, C.Scale pre-seed $2 million – cumulative ≈$2.4 billion.

- Enterprise software / cloud: Redwood Series E $350 million, Beacon Software $250 million, Ignitedata $11 million – cumulative ≈$611 million.

- Other (FinTech, space, HPC): assorted sub-$10 million rounds – cumulative ≈$120 million.

Geographic Distribution

- California: $8.5 billion – primary AI and cloud activity.

- New York: $5.9 billion – 200% YoY increase, concentrated AI-platform deals.

- Massachusetts & Colorado: >$1 billion each – early-stage biotech and clean-tech.

- Top five states capture ≈75% of series capital.

Emerging Trends

- Corporate venture firms (e.g., NVentures, Fidelity) co-lead large late-stage rounds, reducing capital friction.

- AI infrastructure capex projected at $350 billion for 2025; data-center spend up 31% YoY, fueling downstream series rounds for AI platforms.

- Low-carbon ventures receive megacapacity rounds, reflecting ESG integration in VC portfolios.

- Funding concentration aligns with regional talent and infrastructure ecosystems.

Outlook – Q1 2026

- AI-related series funding projected >$700 million per month, driven by enterprise adoption of generative AI and corporate venture participation.

- Low-carbon venture rounds expected to grow ~30% YoY, total series capital >$3 billion as decarbonization mandates intensify.

- Overall U.S. series capital likely to exceed $650 million per month, sustained by AI infrastructure expansion and ESG-focused investment theses.

Regulatory Incentives Are Turbo-Charging Early-Stage Innovation in Canada, the UK, and the US

Canada’s SR&ED Expansion

- Federal budget introduced a “Productivity Super-Deduction”: 100% CCA for new buildings (through 2030) and accelerated expensing for capital equipment (30% rate for liquefaction gear, 10% for non-residential buildings).

- Effective marginal tax rate on qualifying R&D fell from 15.6% to 13.2% – a 2.4-percentage-point reduction.

- Cost: $1.2 billion over five years; $325 million earmarked for liquefaction equipment; $5 billion allocated to the Trade Diversified Corridor Fund.

- Budget also projected a C$78.3 billion deficit offset by C$280 billion of spending cuts and targeted incentives designed to attract C$1 trillion of private capital in five years.

United Kingdom’s R&D Credit Protection

- Q3 incorporation data showed 709 new technology firms in the South-West (+31% YoY) and 15,470 tech startups nationwide (+36% YoY).

- Robust R&D tax credit regime flagged as a primary driver of the incorporation surge.

- Government pledged £10 billion for AI and civil-nuclear R&D and lifted innovation-skills funding by 8%.

United States Stimulus Landscape

- Commentary highlighted the Inflation Reduction Act (IRA) as ineffective for long-term manufacturing resilience, though no quantitative figure was attached.

- Tax-based subsidies remain core to capital projects such as Ford and Hyundai plant expansions, sustaining a modest credit environment for early-stage firms.

Integrated Insights

- Lower marginal tax rates translate directly into incorporation growth: Canada’s 2.4-pp SR&ED cut and the UK’s protected credit regime align with ≥30% YoY increases in new tech firms.

- Sector-targeted credits accelerate capital deployment—Canada’s 30% accelerated expensing for liquefaction equipment ($325 million) is poised to seed clean-energy startups; the UK’s £10 billion AI/nuclear allocation coincides with a 12% rise in AI-focused SaaS incorporations.

- Policy certainty boosts confidence. The UK’s explicit protection clause produced a 709-firm surge, while US commentary on IRA volatility suggests a dampening effect despite ongoing credits.

12-Month Forecast

- Canada: Incorporation growth +12%; effective R&D tax rate 13.2%.

- United Kingdom: Incorporation growth +18%; credit effectiveness very high.

- United States: Incorporation growth +5%; credit effectiveness moderate.

Policy Prescription

- Combine broad-based tax rate reductions (as seen in Canada) with sector-specific credits and an explicit protection clause (as in the UK) to reduce regulatory risk.

- Maintain transparent, long-term frameworks to keep venture capital flowing into early-stage R&D-intensive firms.

- Align fiscal incentives with strategic sectors—clean energy, AI, civil nuclear—to convert tax savings into targeted pipeline growth.

US Dominance and Latin America’s Rise in Startup Funding

Funding Landscape (Q3–Q4 2025)

- United States: $30.0 billion (≈60% of global $39 billion VC pool)

- Latin America: $2.85 billion in 2024, +26% YoY, 7% of global VC

- Europe: $5.2 billion, 13% share

- Southeast Asia: $1.0 billion, –34% YoY

US Momentum

October 2025 delivered $23.4 billion of US-sourced VC, with New York and California alone accounting for $14.4 billion (≈37% of US share). Over 500 deals exceeded $500 million, making the month the second-busiest for “half-trillion-plus” rounds. Federal capital allocations to firms such as ReElement and Vulcan illustrate direct governmental support for AI, high-performance computing, and blockchain infrastructure.

Latin America Acceleration

Venture capital inflows grew 26% in 2024, reaching $2.85 billion—outpacing Europe’s 7% rise. The region now hosts 32 unicorns valued at $71.8 billion, with fintech and mobility leading sectoral allocations. Credit-card penetration hit 6.6 million holders, a key channel for scaling fintech startups.

Trade-Policy Levers

- US–China tech tariffs curb GPU imports, redirecting AI spend to domestic cloud providers and cost-effective compute hubs (India, UAE).

- EU Green Deal incentives pull pension-fund capital toward sustainable tech, though still <2% of the €15 trillion pool.

- US–Mexico–Canada Agreement updates lower compliance costs for fintech and e-commerce, spurring US VC participation in Latin America.

- Indian market liberalization (OpenAI office, tiered subscriptions) opens a parallel growth corridor for US AI firms without eroding US capital share.

Emerging Cross-Regional Dynamics

- AI funding growth outpaces EU peers, reinforcing US leadership in frontier tech.

- Cloud giants (AWS) and GPU manufacturers (NVIDIA, Lambda) consolidate hardware provisioning, deepening US ecosystem resilience.

- Latin America’s unicorn density now exceeds Southeast Asia’s recent output, signalling a competitive realignment.

- Sector focus diverges: fintech and mobility dominate Latin America, while AI, HPC, and biotech steer US allocations.

Outlook 2026–2028

- US VC share projected to stay above 55% of global capital, buoyed by policy support and institutional liquidity.

- Latin America expected to reach $4.0 billion VC by end-2026 if 26% YoY growth continues, narrowing the US–Latin America gap to ~13% of global funding.

- Trade-policy incentives for sustainable tech (EU) and fintech (Latin America) will likely channel additional capital to those regions.

- Aggregate valuation of Latin American unicorns could surpass $100 billion by 2028, driven by exits and secondary-market activity.

Comments ()